Kevin Chen

@jiafengkevinc

Followers

4,013

Following

1,774

Media

275

Statuses

2,008

Postdoc @SIEPR '24 | Assistant Professor @StanfordEcon '25 | PhD @HarvardHBS '24 | AB/SM @Harvard '19 | Econometrics, causal inference, and stats

Joined July 2019

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

#TGS2024

• 170748 Tweets

Tigers

• 103271 Tweets

Miami

• 79815 Tweets

Knicks

• 67573 Tweets

Towns

• 64649 Tweets

Minnesota

• 63816 Tweets

#SmackDown

• 53662 Tweets

Randle

• 48205 Tweets

Wolves

• 34983 Tweets

Rudy

• 34560 Tweets

Royals

• 27266 Tweets

Hart

• 22474 Tweets

#DesafioXX

• 21379 Tweets

भगत सिंह

• 21148 Tweets

Asharamji Bapu Case

• 18228 Tweets

日本破壊クソメガネ

• 16671 Tweets

Equality Exploited

• 15666 Tweets

Cam Ward

• 15401 Tweets

Celtics

• 11244 Tweets

how it started // how it's going

Recently accepted by

#QJE

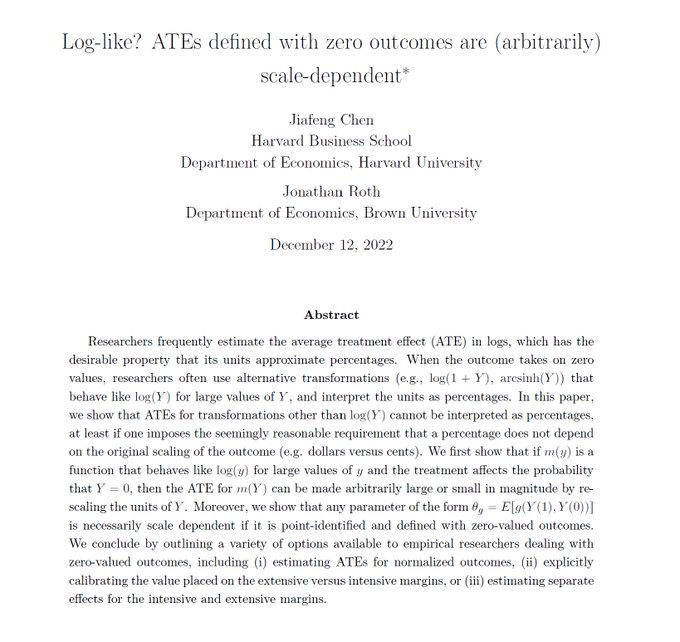

, “Logs with Zeros? Some Problems and Solutions,” by Chen (

@jiafengkevinc

) and Roth (

@jondr44

):

4

195

723

12

63

1K

We've all encountered this problem: "I want to take logs, but my data have zeros => ???"

Commonly (myself included), people use an ad hoc transformation m(.) (e.g. m(x) = arcsinh(x)) that approximates log, and interprets the resulting effect as a %

🧵of paper with

@jondr44

1/n

Twitter is fun because we can promote the work of friends and people we admire!

Today I want to call your attention to a brand new paper by

@jondr44

and

@jiafengkevinc

, available at:

What is the gist?

Check the abstract!

6

78

387

8

154

785

I'm very excited to join

@StanfordEcon

as an assistant professor in 2025, after a year

@SIEPR

. I'm stressed out about moving my 🐱 across the continent, but otherwise beyond thrilled for what's to come!

(also, definitely welcome all advice re: bay area)

46

10

495

Seems like today is a good day to talk about why the bootstrap works

Here's my intuition---

5

34

397

only an economist would call the sample mean "OLS coefficient on a constant"

7

9

370

@KhoaVuUmn

🥴: "Hello, I am

(G'WG)^-1 G'WΩWG (G'WG)^-1.

I want to find the W that makes me as small as possible, but, look at me, I'm a mess"

3

12

318

👀🤩

Synthetic control can be interpreted as an online learning algorithm. Even without assumptions on outcomes, results from online learning imply that synth predictions perform almost as well as those made by the best weighted match.

@jiafengkevinc

1

60

246

4

14

238

as a professional econometrician, i think the WHO's notation choices are amateurish compared to mine

8

7

223

the people who always nod in interviews are my personal heroes

5

6

220

New short paper documenting an easy recipe for incorporating machine learning into linear IV to boost instrument strength *essentially for free*:

Joint work with Daniel Chen and

@econ_greg

#EconTwitter

#CausalTwitter

2

47

212

Excited to share a new working paper taking a closer look at causal inference in school choice settings, where students are matched to schools via algorithms. The paper derives the identified causal estimands under heterogeneous treatment effects (1/n)

2

33

172

because otherwise no one can write a paper, obviously

Seriously though, why should audits be less likely for taxpayers earning $399,999 than those earning $400,000?

6

0

13

1

6

159

Thanks

@jondr44

! A thread on this short paper 🧵

(no econometric toys are harmed in the writing of this paper)

Very cool new paper by

@jiafengchen42

that gives a justification for synthetic control methods

He shows that when treatment timing is random and you have many time periods, SC has close to optimal regret when an adversary chooses the potential outcomes

1

25

129

3

28

157

what is often missing in the statistical software debate is that the labor market value of python and r is positive

Grad students planning to go non-academic

Learn Python and R.

That is all.

Thank you for coming to my TedTalk.

12

31

388

4

8

152

I want to open a discussion about this post by Gelman (

@StatModeling

) and various aspects of RDD inference. Gelman criticizes a paper that shows a close-election victory effect of 2-10 years on "days alive after election" (thread 1/n)

#EconTwitter

1

29

151

I too drop 15 new results in "The Tortured Job Market Paper: The Appendix"

Taylor Swift drops 15 new songs on double album, 'The Tortured Poets Department: The Anthology'

25

43

168

2

8

151

New paper on statistical inference with data from (batched) adaptive experiments with Isaiah Andrews [1/n]

1

21

143

Most regression estimators in the presence of heterogeneity

0

7

128

your daily “regress two independent I(1) against each other” tweet

1

8

126

foolish: use this to instrument trade flows

wise: use this to instrument new trade papers

1

3

114

Since the Twitter exploit must be worth more than $118,000 to a profit-maximizing attacker, the fact that the realized profit is only $118,000 illustrates that the criminal market is not efficient. In this essay I will

That bitcoin scam racked up at least $118,000 in just three hours =>

7

51

105

2

10

105

i'll have to speak to my therapist about this

Here is one:

If X has the same distribution as X', Y as Y', and Z as Z', do we have 𝔼[X+Y+Z]=𝔼[X'+Y'+Z']?

31

134

783

3

5

101

I'm thrilled to announce that I'll be offering difference-in-difference offsets, where I promise to not write DID papers for a price

For a higher price I'll start working on projects like "Why TWFE is More Robust Than You Think" and "Why Constant Treatment Effect is Innocuous"

8

8

102

(while I have your attention, here's a PSA to use weak IV robust procedures)

0

11

100

Live footage of conda dependency conflicts

King cobra bites python. Python constricts cobra. Cobra gets crushed to death. Python dies from the cobra’s venom. 🤯

5K

23K

274K

1

6

88

Excited to share a new preprint with

@DRitzwoller

on semiparametric estimation (read, *machine learning* estimation) of long-term treatment effects, such as those identified by a latent unconfoundedness or a surrogacy assumption (1/n)

1

19

84

i sense a market for this

can someone make the “X as seen by Y” of

{statisticians, biostatisticians, econometricians, polmeth, machine learning}

0

1

19

3

14

79

i'm also on the job market this year 😬

website @ [(n+1)/n]

2

9

71

views about real analysis Did kinda cut the discipline in half

9

4

67

*crosses out “partial identification in causal inference” from research interests because that job is, um, automated*

Our new working paper: tell the computer what you know (and don't know!) about a causal question w/ discrete data → automatically get most precise possible answer (bounds, or a point estimate). Joint w/

@guilhermejd1

@nsfinkelstein

@dean_c_knox

Shpitser.🧵

8

125

533

2

2

68

so the good news is that github copilot does work in stata, the bad news is that it gives you R code

1

1

69

my duck confit came out so well I feel compelled to show it off

1

0

64

T̶a̶y̶l̶o̶r̶'̶s̶ ̶t̶h̶e̶o̶r̶e̶m̶ Mean-value theorem (Taylor's version)

2

0

64

possibly really dumb question: does IV "work" if the instrument Z is confounded with treatment W?

i.e. DAG is Z -> W -> Y, W <- V -> Y, Z <- U -> W,

In PO notation,

Z = Z(U, e1)

W = W(Z, U, V, e2)

Y = Y(W, V, e3)

and (e1, e2, e3, U, V) are jointly independent

10

14

64

Been learning DAGs lately and wanted to be more fluent in translating between DAGs and POs

I think this is a reasonably short proof of the front-door formula/napkin problem that uses only potential outcomes..?

(it can conceivably fit on a big napkin?)

2

2

62

i wonder if anyone has explained the sample variance as

1. regress data on a constant, take residuals

2. regress the squared residuals on a constant

3

0

57

Another way of saying this is that we can't have all three: (a) an average effect, (b) scale-invariance, and (c) point identification. In practice, then, we must decide which two properties we want. [5/n]

1

5

54

that's just econometrics

0

7

57

in short: no alternative transformation can define away the log(0) problem, but sensible alternatives do exist!

[n/n]

3

1

52

your daily macroeconomics tweet

the small angle approximation solves the dynamics of the pendulum by approximating sin(x) = x. How good an approximation is this? This shows the true dynamics (blue) and the approximation (white) for various initial angles

14

156

781

0

5

51

i've got my synthetic wisconsin ready to go

BREAKING: Wisconsin Supreme Court strikes down Gov. Tony Evers' order to stay home in a 4-3 decision.

2K

6K

25K

2

0

47

intro statistics rarely emphasizes the difference between an estimand and an estimator (usually it's fairly clear, e.g. sample mean estimates the mean), but the difference becomes super pronounced and subtle in causal inference

1

9

48

gonna be that guy in the seminar with

@economeager

but in meme form

[this is actually

@jondr44

's example and i just memeified it]

2

1

43

live view of the behavior of the implicit estimand of TWFE under treatment effect heterogeneity

@KhoaVuUmn

1

1

40

Well, a percent is invariant to units, and so a basic requirement is that differences in m(.) should be invariant to scaling.

It turns out the opposite is true: For any m(.) that approximates log, but is defined at 0, one can choose the scaling to get anything one wants 😬[2/n]

2

2

40

Super excited to be presenting this paper at the NBER SI Labor Studies Methods session tomorrow morning!

Thanks

@jondr44

! A thread on this short paper 🧵

(no econometric toys are harmed in the writing of this paper)

3

28

157

2

5

37

If you're at CODE

@MIT

, I'll be presenting some work (joint with Isaiah Andrews) at 11:15am ET today, come check it out!

2

2

38

meanwhile in econometrics, most of what I do is writing P in different fonts

Defining notation for a theory paper is halfway between making up a language and choosing an opening in chess. Small early choices affect what moves are available later.

4

17

382

1

0

37

A buddy and I passed a bunch of SEC 10-K filings through a big pre-trained neural network and examined its brain---because why not, university compute is free and we can't mine BTC anyway

Turns out the network understands which companies are close to which

#EconTwitter

⬇️⬇️⬇️

How can transformer models help us understand economic and financial information?

New workshop paper with

@jiafengchen42

develops an industry classification index from text with greater informativeness about financial metrics than existing text/expert-based classifications [1/2]

1

7

37

2

6

36

𝙉𝙤𝙬 𝙞𝙣 𝙥𝙤𝙨𝙩𝙚𝙧 𝙛𝙤𝙧𝙢

meme form coming soon...

(since this is just linear IV under the hood, it's compatible with AMIP!)

New short paper documenting an easy recipe for incorporating machine learning into linear IV to boost instrument strength *essentially for free*:

Joint work with Daniel Chen and

@econ_greg

#EconTwitter

#CausalTwitter

2

47

212

1

3

35

@otis_reid

A lot of times fancy estimators are actually just comparisons of the correct set of means

3

0

36

i can't believe no one brought up radon-nikodym derivative yet

5

0

34

for some particular reason the harvard-mit econometrics seminar seems to have 13x attendance today

4

1

33

@ben_golub

i'd argue the Rao-Blackwell theorem is better-known, based on me knowing Rao-Blackwell but not knowing the Blackwell information ordering 😂

1

1

32

Sir, this is a landscaping company

71,000,000 Legal Votes. The most EVER for a sitting President!

342K

95K

722K

0

0

33

i think that's what "large-T asymptotics" means

I am reviewing a paper and came across the word “eternal validity,” which is a typo…but its a brilliant typo. Why us economists only talk about internal and external validity? Why not eternal validity???? 😏

#EconTwitter

#AcademicChatter

23

26

476

2

2

31

it's also a good time to finally open yellow van der vaart and build some more intuition why bootstrap can fail---

0

1

32

@AnthonyLeeZhang

seems like most results in real analysis can be understood without real analysis

0

0

32

@ben_golub

@CaltechEconThry

Proof I first saw from

@stat110

's stat 210:

WLOG, assume f(X), g(X) mean zero.

Observe that

E[f(X) g(X)] + E[f(Y) g(Y) ]= E[(f(X) - f(Y)) (g(X) - g(Y))] for X, Y independent and Y ~ X

Conclude by noting that (f(x) - f(y))(g(x) - g(y)) ≥ 0 a.e.

0

0

32

this is why the pscore-as-dimension-reduction thing is a bit of mental gymnastics and word sorcery---estimating the pscore is a high-dimensional problem!

2

3

31

TIL from

@conlon_chris

that one could be using a slower BLAS on Apple silicon, here's a fix that's worked for me, so far, from our thread

@jiafengkevinc

@paulgp

Compare to this -- the point is not that that NumPy is 180x faster than R. The point is that my NumPy setup is using the correct BLAS and my R setup is not:

3

0

8

0

8

31

P̶e̶n̶a̶l̶i̶z̶e̶d̶ ̶r̶e̶g̶r̶e̶s̶s̶i̶o̶n̶ ̶e̶s̶t̶i̶m̶a̶t̶o̶r̶s̶ The Tortured Predictors Department

#TSTTPD

0

2

27

just realized supreme court rulings and the QJE have the same (i think?) typeface

2

0

26

"i have discovered a truly marvelous proof of the results in the main text, which this online appendix has too few pages to contain"

📢 **REStud Page Limit**

With effect from 1st July 2022, a page limit policy applies to all submissions. Papers should be under 45 pages. Online appendices should not exceed 30 pages. A “grace period” is in place until 15th August 2022. For more details:

2

42

272

1

0

27

@jondr44

@ShengwuLi

the easy mnemonic is that Jensen's inequality is always in the direction where you don't want it to be

0

1

26

Happy to share my new NBER working paper with Ed Glaeser and

@davidmwessel

. We find that the Opportunity Zone program, as a part of the 2017 Tax Cuts and Jobs Act, has not (so far) generated a response in residential housing prices. Link: .

#econtwitter

1

1

27

Now, I can't possibly pass on an opportunity to promote some recent work on Twitter, to Twitter, by quote-tweeting

@TwitterEng

(joint work with

@DRitzwoller

)

We built a causal estimation framework on the idea of statistical 'surrogacy' (Athey et al 2016) - when we can’t wait to observe long-run outcomes, we create a model based on intermediate data.

2

23

254

1

5

26

Suppose (Xn, Yn) converges in distribution to (X, Y), and (Yn, Zn) converges in distribution to (Y', Z). (This implies Y' ~ Y). Suppose Xn is independent of Zn given Yn.

T/F: (Xn, Yn, Zn) converges in distribution to some (X'', Y'', Z'')?

4

0

24

I will be presenting this paper on inference post adaptive experiments this Thursday (11:30 am ET) at the International Seminar on Selective Inference.

Come check it out!

1

1

24