Garrett Arms

@ArmsGarrett

Followers

4K

Following

23K

Statuses

1K

Investing. Any opinions my own.

Tennessee, USA

Joined January 2022

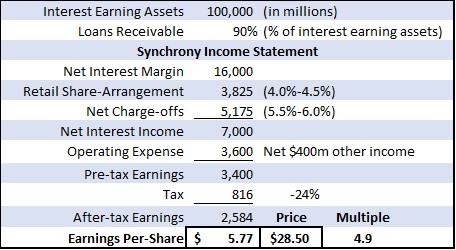

$SYF Quick pitch: bank that trades at 1.25x tangible book, has de minimis deposit flight risk, & targets (earns) a 28% return on tangible equity. While perennially discounted in relation to business quality, SYF is now exceptionally cheap (less than 5x earnings).

16

9

115

@21stCentValue @boujee_banker Issue shares at 2x TBV, increase book, deploy proceeds accretively, reprice to 2x new, higher book, repeat cycle. A veritable (Micro)Strategy in the making.

0

0

7

@tobygadd18 @CasinoCapital Flat (excluding 8 percent divvy) but still printing money—maybe the very reason to own.

0

0

0

$NBN ballpark. Still printing. Noninterest income $6m for 12.31 Q, but still ramping 7(a)biz--current SBA approval runrate +25% over latest Q. EPS ~$2.70 for Q & will be >$12 this yr (& >than napkin). Could buy for sub-3x 2-yr fwd 18months ago--not too shabby.

Long Northeast Bank $NBN. $300m market cap specialty bank w/mgmt that plays way above their pay grade. Tangible book value is $38. Price is roughly the same. 3-year avg ROE is 24%. 1/n

1

1

23

Fully aware that $NEWT is a 'shitco', but the bank just printed a 50% ROE for the year..

$NEWT is a compelling long at $13. Newtek Bank is the largest player in the SBA lending market. At today’s price, it trades at a market cap of $340M & <7x what the company has guided to earn this year ($1.95). 1/n

5

3

32

@SSGY12356 Likely several in this space. IMO, the real kneecapping will be in those still priced as a secular growth story (maybe BMI).

1

0

1

New gross margin still slightly above pre-covid (+120bps), but Used margin now lower (-300bps). Think market’s positive reaction relates to stabilization of New GMs, so partial overhang lift. P&S still a real driver of GP $'s. I would be willing to make the bet against share shift & that distribution model doesn't change. EV requiring inherently lower maint. expenditures & autonomy still major variables, though

1

0

2

The year is 2030. The S&P is at 36,000. Your carefully curated portfolio of value stocks is 20% lower.

2

0

13

@MaldenDriveCap @JerryCap Underperforming the S&P made Ryan Israel a ‘billionaire’. Pretty sweet gig if you ask me.

1

0

1

Never understood why people use the implied value of these Warburg preferred investments as a realistic mark for equity value of the underlying, how they remotely create any floor value, etc. Extrapolating the conversion value to an equity figure always seemed like a sleight of hand to me.

1

0

4

@blondesnmoney @irbezek Be curious to know NOI the mall generated & how in line that is w/ the co's mid-point 15% cap rate estimated NAV guide—seem to be guarding figure closely. JLL would probably tell you. Def one of their lowest quality malls in terms of sales per sq foot, etc.

0

0

5

Correct. The comment that ‘loan book would have to be like 7x larger than it is right now, while keeping expense flat, to make it even remotely attractive’ was all you needed to see to know this guy doesn’t understand the business. Didn’t even realize the company has two other noninteresting earning divisions that support that expense base, but rushed over to retweet a victory lap about “putting the down the NEWT bulls again”. Gotta love that. The point is not to fixate on the unguaranteed balance of the SBA loan in isolation, ignore the servicing income from the entire loan, and claim they don’t make any money holding the remaining paper over time. The takeaway is that when you combine the gain on sale, all of the servicing income, and a 10% coupon on the unguaranteed portion, after adjusting for credit losses the returns on equity in this business are just higher than most all lending on a risk-adjusted basis. Separately, the company does provision upfront—the whole point of CECL is to run an expected loss model instead of booking those charge offs when incurred, so there is no long-tail burn. For context, the company maintains a 7.8% allowance against unguaranteed 7(A), compared to the 8% cumulative charge off rate it underwrites to (which includes ALL losses on loan), as mentioned above. Moreover, the 35% of the portfolio that’s over 3-4 years old is through the stress of the default curve, so charge off rates on older loans are much lower. And there is no seasoning issue. It originates, services, and sells SBA 7(A) in the same way it did before the bank merger. Fee income is the model, so naturally, if you strip out all of the noninterest earning revenue and allocate the entire expense base against net interest income, the company would appear unprofitable. But that would tell you basically nothing. The worry with these companies is always that the gain-on-sale economics are inappropriately front-loaded (which is a legitimate concern as it has ongoing servicing responsibilities and risks related to the asset)—it’s a reason to keep a close eye folks like NBN who are growing this business by +50% with no real history in the space. It’s much less of a worry for a company that has been in the business for 15 years and is going at 15%. With NEWT, you can just build a static model with zero growth in SBA originations and the servicing pool and see that the company would still be highly profitable.

0

0

3