Shiv Sharma

@shivsharma_5

Followers

7,313

Following

2,012

Media

232

Statuses

2,635

President & GM @Stocktwits @StocktwitsIndia . Former @AWSCloud , @Cisco_Invests , Fidelity International, @RBCCM

Singapore

Joined December 2013

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Adrián Marcelo

• 159802 Tweets

Alvarez

• 130980 Tweets

#FileninSultanları

• 127700 Tweets

ホロライブ

• 85118 Tweets

Vargas

• 77556 Tweets

Vinesh Phogat

• 69967 Tweets

ファミチキ

• 59078 Tweets

湊あくあ卒業

• 56900 Tweets

#NeerajChopra

• 38270 Tweets

YARI FİNALDEYİZ

• 24799 Tweets

Elif

• 18620 Tweets

Yui Susaki

• 16457 Tweets

卒業発表

• 14226 Tweets

こねこ便

• 12901 Tweets

アスクレピオス

• 12050 Tweets

नीरज चोपड़ा

• 10220 Tweets

Last Seen Profiles

$FSLY is by far my most successful investment and wanted to share my take. In summary, sentiment and valuation were at all-time lows leading to the "perfect storm"- super rare to see. Its also shows how rigorous fundamental research + momentum investing can coexist

16

29

247

Here is my portfolio (as of May 1, 2020) in order of size: MSFT, AMZN, AAPL, NOW, FB, BABA, PYPL, NFLX, CRWD, SE, RNG, TWLO, FSLY, SMAR, WORK, ESTC, LVGO, DDOG, PTON. Large cap is usually ~60%.

No options, but long 3x ETFs in my gamble portfolio.

14

20

166

Joined the

@Stocktwits

community three years ago and have been fortunate to learn a ton.

I could not be more bullish on DIY investing & investing education, and am super excited to start working today to help them scale internationally + India!

Stayed tuned for updates!

19

4

111

13F's are out

@whalewisdom

. No big surprises. $FSLY becoming popular. $SMAR is creeping up in popularity (tons of upside @ 12x forward revenue as growth could re-accelerate + room for multiple expansion)

Also, feels like $NVDA and $TSLA are underowned, which could be a catalyst

7

12

106

This is an GINORMOUSLY smart deal for $TWLO. Shows their interest to own the full customer journey, become more strategic to customers, + developer GTM... Building a 360 deg view of the customer AND acting on it is the Holy Grail problem at the moment

4

6

105

Long-time lurker, finally decided to start sharing my investing thoughts and portfolio. Long-term strategy w/ focus on secular trends and valuation. Own best-in-breed names with massive moats AND use VC-approach (i.e. product-driven) to identify high growth small-cap names...

9

18

99

Big reason why $ESTC trades at a discount to other open source software (ie see delta between “currently utilizing” and “using from public cloud vendor”) $MDB $CFLT $GTLB

7

11

99

Definitely true, but these insights would have been a bit more helpful in late 2020 / early 2021 $QQQ $ARKK

An entire generation of entrepreneurs & tech investors built their entire perspectives on valuation during the second half of a 13-year amazing bull market run. The "unlearning" process could be painful, surprising, & unsettling to many. I anticipate denial. Some thoughts:

493

3K

20K

10

6

86

Monthly portfolio review (5/29/20) in order of size:

$MSFT, $AMZN, $NOW, $PYPL, $FB, $SE, $FSLY, $CRWD, $NFLX, $WORK, $LVGO, $RNG, $TWLO, $PD, $SQ, $BYND

Here is my portfolio (as of May 1, 2020) in order of size: MSFT, AMZN, AAPL, NOW, FB, BABA, PYPL, NFLX, CRWD, SE, RNG, TWLO, FSLY, SMAR, WORK, ESTC, LVGO, DDOG, PTON. Large cap is usually ~60%.

No options, but long 3x ETFs in my gamble portfolio.

14

20

166

5

5

67

Paytm and Zomato get all the love, but the Freshworks IPO is a legit milestone for Indian startups. Great example of India leveraging its own IT talent to scale their own business rather than for clients … First of many more Indian SaaS IPOs on the way

2

9

71

I get $LMND is a disruptor to a massive, broken insurance market, but the unit economics are horrible. Not used to seeing 30%+ churn and 20% gross margins. LTV/CAC is ~0.6x today vs insurance industry of 2x...40x 2021 Revenue is nuts, I think it gets cut in half around lockup

12

15

68

Excited to share my first editorial on the state of investing education in India, and how “Social Finance” and influencers can help!

@StocktwitsIndia

@Stocktwits

5

10

66

Thoughtful product take on $TDOC $LVGO deal. Summary is nothing new, but does raise interesting points that I had not considered on product gaps and potential responses by other industry participants ... I sold at announcement but may add back later

6

7

63

I think $ROKU has a huge 2021 as 1) ad spend comes back, 2) ad budgets are reset and allocation to OTT increases, 3) Roku’s ad stack improves

Every single Roku conf call:

"Nahh, we're not going back to the linear TV world."

0

1

25

5

4

64

Wow... big but not un-expected... $SE will no longer be the only Southeast Asia pure play in US markets.

Wouldn’t be surprised if they use

@tokopedia

as a platform for further M&A consolidation in the region

BREAKING: Billionaires Richard Li and Peter Thiel's blank-check firm is considering a potential merger with Indonesian e-commerce giant Tokopedia, sources say

1

10

26

2

4

64

Ark Invest is quietly building a disruptive biz. Only firm I know that explains decisions and content is solid

@ARKInvest

Honestly think my portfolio will struggle to outperformform $OGIG + $ARKW for extended periods...considering buying these and calling it a day

The August

#mARKetUpdate

webinar is now available! Please note that due to a conflict in scheduling, the event was pre-recorded earlier this morning. We hope you enjoy the recording and we will see you back LIVE for our September episode!

2

11

52

4

10

63

With so much noise on tech valuations, wanted to go academic (which i dislike lol) and share my take on "whats priced in" $ABNB's valuation. Remember, revenue multiples are short form for DCF's

In summary, it's "priced to perfection", but not stupid crazy ... (1/3)

3

8

60

Does anyone know why $OKTA has historically (until recently) traded at a premium to $CRWD 's forward revenue multiple?

CRWD is growing twice as fast. Both have massive TAMs with optionality and limited competition...

7

2

60

#PayTmIPO

prospectus is a must-read for anyone interested in India. Few thoughts and graphics below:

- 333M accounts (50M MTUs)

- 21M merchants

- Product reminds me of $SQ

- LONG runway (e.g. 3% India owns equities; 4% have credit cards), but Monthly Transacting Users are flat

3

8

61

A must read on $WORK

@stewart

. Rare seeing such forthcoming CEO interviews

Takeaways: 1) Shows top-down maniacal product obsession you won’t see in diversified vendors, 2) best-in-breed may have LT edge over bundles, 3) API connectors btw apps are a must

1

4

55

Just recorded my first podcast! Check out below to hear my thoughts on global tech stocks, social finance, communities, the creator economy, and why I'm uber bullish on

@Stocktwits

&

@StocktwitsIndia

!

This weeks pod with

@shivsharma_5

is live!

Covering all things social finance and tech investing.

The future of investing, the communities behind it, and opportunities for Indian retail investors.

Transcript & Audio:

1

1

9

3

9

55

Of $ZM's new products, I'm most excited about OnZoom. Unlocks a massive TAM for a consumer/B2C use case popularized during Covid. It could be a YouTube alternative for influencers/SMBs to run their biz and grow their audience (ie Shopify for ecommerce)

Introducing OnZoom - Zoom's new immersive experience and event marketplace. 🎉 Head to to explore all that it has to offer!

6

28

90

4

4

54

According to Goldman Sachs, 71% of all option trades in October were on $TSLA and $AMZN 🤯

1

4

53

Looks like $SE 's new country launch playbook is on track in Brazil $MELI

They start with Free Fire (high margins) to offset loss-making e-commerce. In Brazil, e-comm ASPs are a fraction of MELI's. This playbook has worked across ASEAN and Taiwan so far. Data from

@GoldmanSachs

1

8

52

I keep promising myself to avoid, but $BABA is looking super cheap again - 23x NTM earnings & 19x NTM EBITDA

Unless there is some significant unknown regulatory issue, this is probably the best value you'll find. With AliCloud, feels almost like $AMZN / AWS in the early days

9

3

46

As much as i love $NET for its TAM and optionality in cyber-security, lot of good news is priced in and risk/reward is not great. NTM Revenue Multiple has grown from 10x in March to 44x right now

$NET may spend 2021 digesting its gains and growing into its multiple

3

2

47

This why you have to own cybsecurity. US media and government completely downplays extent of China security risk.

Look at 13Fs and funds holdings, security is underowned (versus SaaS) by institutions bc its a complex landscape and tough architecturally $ZS $NET $CRWD

Former Google CEO Eric Schmidt says there's 'no question' Huawei routed data to Beijing

10

67

130

3

4

45

I get why pure growth investors don’t like this deal, but I like at first glance. More obvious synergies here than most deals I’ve seen - cross-sell into each other’s customer base and bundling. Also complementary as $TDOC handles dr appts and $LVGO monitors between appt care

Creating a new standard for how healthcare is delivered, accessed and experienced around the world. We're merging with

@Livongo

and bringing chronic condition management to the full spectrum of health needs being addressed through

#virtualcare

. Read more:

5

22

76

4

9

47

While it’s easy to make a case that $ZM is not expensive (see below), still think you’ll see a big sell off when Covid ends as 1) $ZM growth rates normalize, and 2) $ flows into covid-hit sectors ... in long run, I think growth story holds up but with scary volatility

5

2

47

Take a look at $FUTU ‘s numbers below 🤯

Futu is an HK-based brokerage and social community that gives “emerging affluent Chinese” access to global equities. Average user age is 36 and 40% of base works in tech... thanks

@JonahLupton

for calling out

3

2

47

Crazy that $SHOP $ZM $SNOW will likely pass $CRM in market cap in 2021 or 2022 ... At this rate (even if growth and multiples normalize), software is going to be a big chunk of major indices in the near future

2

4

46

Finally back home after 2 months in Delhi for family reasons and 21 day hotel quarantine in Singapore

#covidsucks

4

1

43

With huge gains in $FSLY and $LVGO, the biggest contributor has been multiple expansion (see below). It’s hard to find such high quality companies at these discounts, but possible. Can’t expect this level of outperformance buying SaaS at 30-40x forward rev

6

0

43

Well said on $CRWD. No one would know current trends in cyber security than

@SpeakerPelosi

... I’ve always felt security threats have been kept relatively quiet by govt and media

Nancy Pelosi buys $CRWD stock. Not gonna take that as bearish.

If I was a gambling man, knowing her sleaze propensity, she probably saw a draft of some large govt. RFP only they could win. $CRWD.

23

37

247

2

3

42

Decent take by BofA. $LVGO CEO said they’d eventually compete w $TDOC so had to merge or compete. Why wouldn’t $LVGO double down and grow TAM by adding diseases? ... Either way, VC investors still holding will make a killing here w the cash portion of proceeds

3

5

43

In their Paytm initiating coverage report, Goldman Sachs forgot to include

@StocktwitsIndia

in the fintech competitive landscape :)

0

1

40

Good $TDOC $LVGO summary here. But I question if Covid has permanently accelerated telemedicine like video conf. Video conf is used for biz/social where healthcare is sensitive and personal...i think younger demographics more likely to adapt than elders

10

2

41

India's top 10 stocks are going to look much different real soon. Shifting from old economy + financials to digital-first will also lead to Nifty index valuations looking vastly different ... Goldman Sachs sees ~150 tech IPO worthy companies

#PayTmIPO

#NykaaIPO

#policybazaar

0

4

38

$FTCH is another big win for Fintwit while most institutional investors I know have avoided ...

@howardlindzon

@JonahLupton

@OphirGottlieb

and many others have been all over it. Like $FSLY, common denominator is low revenue multiple + accelerating growth

Absolute explosion from wave 4, technical and fundamental monster $FTCH

3

1

25

4

3

38

Super pumped to work closely with my friend & mentor

@howardlindzon

on taking

@Stocktwits

@StocktwitsIndia

to the next level.

Hit me up if you want to chat strategy, partnerships, product, community, content and social…

Over

@stocktwits

we are quadrupling down on crypto, India, and my fave thing media/education like our 'Trends With Friends' brand.

Integrations we have rolling out for AI and our own data will be live soon.

meet

@shivsharma_5

who is running biz dev and growth as our President

11

6

46

7

4

38

I’m not buying $SNOW here, but the math Puru is prob looking at is $65B enterprise value / $1.1B of next year rev = 60x ... if they CRUSH estimates like $ZM $SHOP, maybe the multiple is really 40-45x? That’s not as bad as you think for a company earlier in lifecycle w TAM ahead

$SNOW revenue estimates for FY ending -

Jan '21 ---> $574m (+117%YOY)

Jan '22 ---> $1.1b (+90.2%YOY)

Jan '23 ---> $1.8b (+68.9%YOY)

This might explain its 'insane' valuation.

I have a starter position.

31

29

267

9

1

36

Excited to be a host in the All About Money 2021 Conference with

@_groww

@rachana_ranade

@vivbajaj

@PrateekLearnapp

@Abhishekkar_

and many more!

4

5

36

It’s likely volatile for now, but I like $AGC / Grab long-term. It’s the super-app of SEA. Here’s a few slides

~14x forward rev is expensive for consumer tech. Key is 1) ARPU growth from Fintech upsell, 2) B2B oppty w/ merchants, 3) obvious SEA growth tailwind (like $SE)

2

4

36

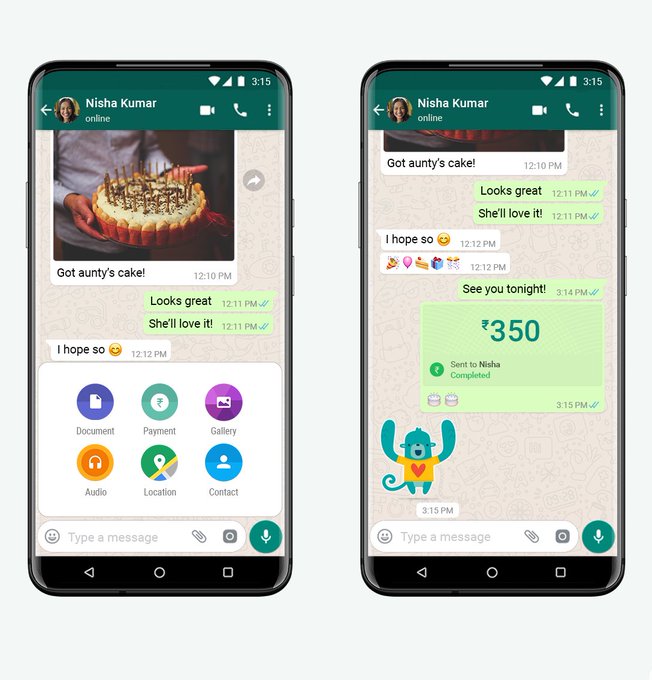

I will say $FB

@WhatsApp

did a pretty slick job integrating P2P payments. Given WhatsApp is the default OS in India, this will be pretty successful... $SQ $PYPL are fortunate WhatsApp isn’t as popular in the US

Starting today, people across India will be able to send money through WhatsApp 💸 This secure payments experience makes transferring money just as easy as sending a message.

776

2K

9K

5

3

36

Nice summary of the $ROKU opportunity. Secular shift to CTV from linear TV driving ad resiliency and growth while other internet ad businesses facing demand volatility

2

4

37

7) Today, FSLY trades at 32x forward revenue (up from Covid-low of 4x). Valuation is super tough to digest on the surface. Market is optimistic about its Compute

@Edge

product, which is in currently in beta, and institutions currently buying. I'll trim, but its prob going higher

8

3

36

Likely why BNPL stocks been struggling ... survey results are not surprising though $SQ $AFRM $MQ $PYPL

2

6

33

Nice update here if you like $ROKU

2

3

33

I really think Covid will create a new generation of DIY investors who made a ton of $ owning obvious beneficiaries $PTON, $ZM, $WORK, $TSLA, $QQQ

5

3

35

Super excited and honored to speak at

@iitbombay

… If you are a college student, please be sure to register for their Virtual Stock Market Competition📈

@StocktwitsIndia

E-Cell IIT Bombay presents speaker session from

@shivsharma_5

, VP International at Stocktwits.

Register for Virtual Stock Market competition to attend the session. VSM will be held on 1st, 2nd and 3rd October. Link to register:

@StocktwitsIndia

1

6

27

4

8

34

Own/love $SE. Another eg of why valuation matters as much as technicals (e.g. $LVGO, $FSLY). Its a ~100% grower that recently traded as low as 3x forward revenue! As investors understood the SE Asia story, revenue multiple expanded to 10x forward rev...should have loaded up more

Here's why I love gaps: $SE gapped 35% on 2/27/19 on 1,016% above avg. volume and never looked back. From the gap day close it has ran 325% in 472 days or 15.7 months. The average TML runs on average for 18-22 months. Remarkable. Doesn't have the earnings but a good one to study.

3

4

36

2

1

34

Helpful link for IPO lockup expiry dates. $JFROG $SNOW $AMWL $U expiration coming this week. $FUBO next month

3

2

33

$SQ Cash App ARPU is $30 compared to $PYPL Venmo’s $13

Honestly, I expected an even greater delta given Cash App’s product portfolio is much farther ahead

3

3

34

IMO - Valuation is why $FUBO IPO has done so well. ~50%+ grower with a $2.6B market cap, sports gambling growth upside, and M&A optionality.

$ROKU and $DKNG are the lazy comps here who trades at 20x and 23x forward revenue, respectively... FYI, lock-up is coming up soon

6

2

32

Interesting take on potential for “sell the news” on WFH, and rotation to longer sales cycle names. Channel checks citing improved demand for HCM... explains why $WDAY has become a popular hedge fund name

Focus on employee experience also + for $MDLA

5

6

32

These $SE numbers are 🤯! Reminds me of the Amazon model as the gaming segment profitability funds e-commerce growth

Tons of runway and optionality still left. Southeast Asia (or ASEAN) combined is almost the size of India with higher GDP per capita

$SE Q3 earnings call recap:

(STOP ASKING ME IF I SLEPT THROUGH MY ALARM, DO U HAVE NO FAITH IN ME i'm slow at typing 😂😂😂😂)

17

5

237

1

0

31

Super proud of our team! Pretty certain that we were one of India’s fastest growing social media brands in 2021! 🚀📈

@pratspective_

@iYashUpadhyaya

@AdityaM31264398

Boss: We should hit 200k IG followers by Dec 2021.

Me (admin😎) right now:

0

3

53

3

3

30

$SMAR had a sneaky good user conference last week. Laid out vision of being a simple “low-code, no-code” platform that brings in data from SaaS apps to automate workflows

Think of them as a customizable layer above all SaaS apps. Enormous # of use cases. Super early days here...

3

5

31

Nice take by

@Beth_Kindig

on $ZM. I agree with the thesis, but for me its 1) ZM Phone + other product optionality, and 2) the valuation thats attractive (24x forward revenue - from high of 60x)... Also, remember they have 30% EBITDA margins and could soon be valued on EV/FCF

Shares of $ZM are cheaper now than they were before the pandemic.

In my new Forbes article, I analyze why the company is set up for sustained success that is not dependent on Covid-19.

36

58

516

2

1

32

Wow

@lillianmli

is my new go-to for China Tech. Thread below is her $BABA bear case that’s under discussed while many funds been buying the dip citing valuation

Also below, there’s a good read on why China IT/SaaS spend has lagged. Similar dynamics to India and Southeast Asia

1) Let's talk about my reaction to

@packyM

's Alibaba longform. (Oh yeah, Substack deserves its own reaction genre).

While I enjoy Packy work, I think this piece missed local context (similar to a lot of English writing on Chinese tech rn).

21

77

554

1

0

32

$MSFT Azure results were super impressive - growing 47% @ $20B runrate. They are mostly large enterprise w long, complex sales cycles. AWS has high mix of digital biz who adopted early and expanded usage over time... Seems like MSFT gaining share in sticky enterprise customers

Cloud Giants Update 👀MONSTER businesses

AWS: $46.4B run rate growing 29% YoY

Azure: ~$20B-$25B run rate (exact rev $ not disclosed, this is estimate), but 47% YoY growth

Google Cloud: $13.8B run rate growing 45% YoY

*Google Cloud includes GSuite as well as GCP

5

24

142

1

1

32

5 year weekly chart of my favorite large cap software company $NOW (over $CRM)

Revenue multiple has always been expensive. Meanwhile, FCF has accelerated with operating leverage. And, mgmt keeps expanding its TAM without drastic acquisitions

4

3

30

$GOOGL earnings beat was obvious going into the Q. I expected ad spend coming back from SMBs and most impacted sectors

But, surprising how management attributed growth to digital shift and declined to comment on sectors like travel... Feels like a nice setup for rest of 2021

2

1

31

Another data point that shows security is still an IT priority. Likely won’t change anytime soon. $ZS $NET $CRWD

0

4

29

Love $SE, but it'll be much harder for them to scale e-ecommerce operations in India than it was Brazil ... Garena and gaming side is a different story and already doing well

7

0

29

Super interesting that $WORK is just now starting “solution selling”. This is enterprise sales 101 that most (CRM, NOW, SAP) have mastered. Shows how early Slack GTM is and theyve gotten this far on brand value

This will also unlock deeper workflows + use cases in Sales, IT, etc

1

2

30

Great listen on the state of the semiconductor industry ... Best explanation I’ve seen on why the industry could be shifting from being highly cyclical to secular growth. Also, a derivative play on AI/ML usage $NVDA $AMD

Fun interview with

@koyfman

for

@KoyfinCharts

"Investing Wizards" series.

via

@YouTube

Also put it on my channel for posterity.

13

22

184

3

3

29

You're about to see non-Indians googling "how to buy Indian stocks"

According to Bank of America, “India will see $300 billion to $400 billion of market-cap creation in the internet ecosystem in the next five years”

5

3

30

Doing work on $DOCU after the 30% pullback. Core product (most of revenue) is easy to replicate. But, the brand is a now verb with tons of runway ahead. Long term optionality with CLM, embedding into workflows, and smart contracts via blockchain ... I’ll prob pass for now tho

4

2

30

$NOW is often forgotten for smaller (more expensive) names, but its one of my highest conviction holdings. They’re quietly executing, entering new buying centers outside of IT, and are now strategically relevant in the enterprise.. for short term, Partner channel checks are +

3

2

29

I bet most don’t realize that $ZM has over double the Free Cash Flow margin than Salesforce

SaaS businesses are often more profitable than people imagine on a FCF basis (SBC is a huge driver between difference in GAAP Op Margin and FCF Margin). And it's not just the mature companies who spit off FCF. Some more recent IPOs have strong FCF margins too! $ZM $CRWD $ZI $DDOG

13

34

190

1

2

28

My style is to stick with the best-in-breed and I thought I’ve had a solid year, but this chart below of top Russell YTD performers is insane. $NVAX (+2,330%), $CODX (+1,570%), $NLS (+1,100%)

3

2

29

The crazy market reaction to $NET news (that Fintwit already knew) shows there’s still imperfections and opportunity to find “relative” value ... feels like w so many SaaS names, investors been overly focused on rule of 40 + multiples over product roadmap and optionality

The market sure in love with $NET today in realizing they are a $ZS competitor. Some of us have known this was coming since... uh (checks notes).... February.

Let’s refresh on a few past tidbits.... /1

10

19

188

2

0

26

Nice reminder here of $NCNO, which is in the 2021 sweet spot of fintech + SaaS

It was loved on Fintwit around the IPO. Now that it’s past the lockup, looks like it’s bottoming.

Commented on $NCNO $U $CRWD - The Best Cloud SaaS Stocks In A Correction: Stocks We Plan To Buy On Dips.

0

2

11

1

1

28

Good read by

@HedgeyeTech

... Can’t treat all SaaS the same. Will be interesting to see which sustain their multiples and reach next phase like $NOW, $TEAM. Some will need m&a; some have TAMs + product/mkt-fit to support organically

Important to constantly challenge yourself by taking the other side of your thesis - it's the best way to know where you might be wrong. We put out the slide below on Monday post our 5th installment of the HT3 Monthly Data Call... $MDLA $WORK $SMAR $TWLO $NET

4

5

72

1

2

28

Nice charts and data by

@MeritechCapital

on $CRM and SaaS during the financial crisis

ARR growth dropped from 52% to 20%, altho margins held up better ... Pricing in lower estimates (if you believe in this scenario) is why multiples can overshoot to the downside

1

4

27

Bold comments on $TSLA by

@chamath

. Wish I was more technically skilled to have an informed opinion

If he and

@CathieDWood

get this right (with retail), they’ll be in this generation’s Warren Buffet club. Also, imagine the uproar against Wall Street who missed this for clients

4

1

28

Favorite hedge funds with a similar approach and portfolios include Whalerock Capital, Tiger Global, Coatue Management. My goal is to provide ordinary investors with confidence to allocate a % of portfolio to tech-enabled secular growth winners!

1

0

28

Funny how you don’t hear much about previously recent IPOs anymore like $API... ~50% off highs and valuation far more attractive

6

1

27

Another thoughtful listen and amazing how much high-end content is available. Think you’ll see many new concentrated, VC-style growth funds succeed in this cycle

Also, amazing that Fintwit caught most of these names with 1/1000th of the work, 13Fs, and technicals 🤣 $SQ $SE

Weekend reading secured - for at least 78 minutes!

Here you can find the transcript of my talk with

@DennisHong17

&

@HaydenCapital

.

Some of my learnings are collected in special quotes you can find in the text.

2

17

131

0

2

27

Partially why so many institutions avoided $TWLO despite the biz momentum. I've owned for years, but have been trimming the past few months... its also why mgmt has been so focused on validating/growing TAM and moving up the software stack (i.e. Flex)

4

1

27

Guess the metaverse barely existed last quarter... Thanks, Zuck $FB 🤪

2

0

28

As Covid fears slow, I continue to like names that have structurally benefitted, but saw core parts of biz negatively impacted.

Eg SQ Cash App has benefitted, but core payments volume down. $ROKU audience and usage up, but ad demand been tough

Interesting piece out by $SQ.

"On March 1, 8% of U.S. Square sellers were effectively cashless; 54 days later, on April 23, the number of cashless businesses had skyrocketed to 31%."

5

87

380

1

0

25

Pretty crazy how every single analyst on CNBC is recommending cyclical recovery stocks... Meanwhile, $ZM $PTON $TDOC are all well off-highs, charts looks like potentially bottoming, and at relatively decent multiples

0

0

25

Nice summary of channel checks. Nice confirmation of what most know and not many surprises.

$DT > $DDOG is not surprising since audience was large enterprise IT buyers

2

3

27

Nice to see India’s SaaS ecosystem getting media attention. I hope some of these consider IPOs in India over the US

1

3

27

While this earnings is great for $SHOP, the results show how broken the sell-side estimates system is. Low estimates optically inflate revenue multiples and spook investors... meanwhile, buy-side investors who did the work knew the estimates were too low and were happy owning

Shopify with a BLOWOUT quarter. Do people still think their "multiple" is too high? 😀 $SHOP

- $714M rev (+97% YoY) vs $518M consensus

- $196M subscription rev (+28%)

- $518M merchant solutions rev (+148%)

- $30.1B GMV (+119%)

- New stores created (+71%)

- 53% GM

- 8% FCF Margin

15

53

481

3

0

27

$OKTA is one of my other favorite SaaS names that I’m watching. Never owned it but always wanted to. Still expensive but ~30% off highs is not a terrible entry

1

0

25

More data points and rationale on why I wait for IPO lockup’s ... $SNOW $U $JFROG $PLTR $ABNB

Traditionally, IPO lockup window has been a great time to buy names you believe in for long run. Pre-C19 in Jan we ran an analysis w/600%+ return investing in top enterprise names (25%+ growth at IPO) from '12-'16 at lockup. You don't have to be in at IPO.

#golong

6

6

115

1

1

27

This partnership shows why $ZM can’t be relied on for telemedicine at scale. In fact, I’d argue $TWLO is better positioned bc vertical-specific vendors can us their APIs

3

1

27

The supply constraints highlighted by $PTON highlight $NLS competitive advantage in manufacturing capacity at the moment ... rare to see for those who focus on digital businesses

5

0

27

Amazing how underweight China still is in the MSCI... If this changes, would be a massive catalyst for Chinese equities if this were to even slightly change

5

2

26

While most try to correlate $ZM ‘s revenue multiple with rev growth of SaaS peers, don’t forget the super efficient GTM model. It reflects in its EBIT / operating margins:

- ZM (now): 41%

- ZM (normalized): 30%

Large cap peers:

- ADBE: 45%

- CRM: 20%

- NOW: 25%

- MSFT: 41%

1

2

27

Acquiring $PINS is an expensive way to steal AWS customers and migrate cloud usage

“MSFT has been pursuing an acquisition strategy aimed at amassing a portfolio of active online communities that run on top of its cloud platform”

6

3

27

Not surprising to see security and infrastructure software as so sticky. Long buying cycle up front, but huge pain to rip out $CRWD $SNOW $MDB

The LTV/CAC ratio measures the relationship between the lifetime value of a customer and the cost of acquiring that customer. For example, the value of $CRWD's customers is 8.2x more than the cost of acquiring them. Here's how some top

#SaaS

stocks compare.

$PLTR $SNOW $NET

9

110

559

2

2

25

One of the favorite companies that I own. Only digital public pure play on ASEAN, which collectively is almost as large as India with higher GDP/Capita... for anyone interested, check out this Google / Temasek report for details

$SE quarterly results -

Adj. revenue +57.9%YOY

-> Garena rev. +30.3%YOY

QAUs 402.1m (+48%YOY)

Paying users 35.7m (+72.5%YOY)

-> Shopee rev. +110.5%YOY

GMV+74.3%YOY

Adj. rev. as % GMV = 5.1% (4.2% in Q1 '19)

Adj. mkt place rev as % of GMV = 3.8%

I've increased my position.

13

15

277

1

2

25

Nice read here on $U by

@LoupVentures

. I'm not buying here as it will be choppy (as any IPO), and I dont think we've hit the inflection point of AR/VR or "gaming as a social network"...But, this could easily be a less flashy winner from this IPO cohort

0

5

26

This trend is only getting started. Once you’ve experienced this, who would go back to city life. Bali is on my list

Barbados is considering letting foreigners move there for a year and work remotely.

18

73

215

6

2

26