Francisco Roch

@francisco_roch

Followers

1,818

Following

825

Media

125

Statuses

876

PhD in Economics, University of Chicago. Lic en Economía, UCEMA.

Joined October 2011

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Olympics

• 3863746 Tweets

Venezuela

• 1138221 Tweets

Bitcoin

• 473774 Tweets

Christianity

• 465499 Tweets

Islam

• 428271 Tweets

Last Supper

• 377452 Tweets

Hezbollah

• 287496 Tweets

Majdal Shams

• 135008 Tweets

Sanchez

• 113000 Tweets

The Villages

• 106110 Tweets

Greece

• 89520 Tweets

لبنان

• 84467 Tweets

Nadal

• 83689 Tweets

Druze

• 82261 Tweets

Lebanon

• 75814 Tweets

مجدل شمس

• 69626 Tweets

金メダル

• 61070 Tweets

Jazz

• 48833 Tweets

C Spire

• 44289 Tweets

Alcaraz

• 40528 Tweets

Medina

• 33404 Tweets

YO SIGO A DENISSE PORQUE

• 31172 Tweets

Antoine Dupont

• 22802 Tweets

Gary Gensler

• 19526 Tweets

Maresca

• 16920 Tweets

Giannis

• 16628 Tweets

#アイドルへモーニングコール

• 16035 Tweets

Suns

• 14046 Tweets

Shai

• 12447 Tweets

Economists have less credibility than sports commentators 😬

18

118

552

Always a privilege to attend a talk by Tom Sargent!

“It is very hard to read, it is only in words” and “You should only read it after you are 5 years older than I am”, about the General Theory by Keynes.

8

9

198

Argentina 1 - Brasil 0 … and just received a R&R at Econometrica. What a wonderful evening! 🥳

8

1

170

First person to ever call me “Dr Roch”. This photo magnet from my thesis defense has brightened up every fridge I had since 2012. So privileged to have taken your class, been your TA and had you as one of my advisors.

1

2

145

Happy to share the news that my paper with

@fqroldan

on state contingent debt (link to the paper below) has been accepted for publication at the JPE Macro! 🥳🥳

11

7

99

Happy to see that my paper with

@fqroldan

on state-contingent debt in JPE Macroeconomics has been published online

@ChicagoJournals

@JPolEcon

5

12

96

After a long journey, our paper on fiscal rules is out at the AEJ: Macro!

The October 2022 issue of AEJ: Macroeconomics (14, 4) is now available online at .

1

5

23

11

3

97

Thrilled to join the editorial team of the IMF Economic Review as Associate Editor. Submit your papers!

4

2

96

Celebrating with Suman Basu,

@EmineBo88305436

,

@GitaGopinath

the submission of our paper on “Integrated Monetary and Financial Policies for Small Open Economies” (missing in the pic our coauthor

@dfilizunsal

). Link to the paper below.

1

2

92

De vuelta después de 563 días. Sensación de primer día de colegio

0

0

83

Just presented my paper on Sovereign CoCos and Debt Forgiveness (joint with Hatchondo, Martinez and Onder) at

@lacealames2023

. Link to the paper below

2

6

82

Just released. Our new IMF working paper on Uncertainty Premia, Sovereign Default Risk, and State-Contingent Debt. Joint with

@fqroldan

Check it out!

4

7

78

Just released. Our new IMF working paper on Sovereign Cocos. Joint with Juan Carlos Hatchondo, Leonardo Martinez and Kursat Onder.

2

13

76

Are interest rates and flexible exchange rates enough to manage a turn in the global financial cycle?

@GitaGopinath

tackles this question in her Feldstein Lecture, based on our research on optimal monetary and financial policies. (1/2)

2

16

74

Long journey with a great ending! Maybe we should ask what levels of spreads countries should target, instead of asking what levels of public debt they should aim for.

Forthcoming in AEJ: Macroeconomics: "Fiscal Rules and the Sovereign Default Premium" by Juan Carlos Hatchondo, Leonardo Martinez, and Francisco Roch.

0

6

33

0

3

61

The new Research Handbook of Financial Markets is out!

In Chapter 17, Leonardo Martinez,

@fqroldan

,

@jzettelmeyer

and I survey the literature on sovereign debt. Check it out!

Three years of effort. Many timely, insightful chapters by truly excellent authors. The Research Handbook of Financial Markets is just published.

Now sharing the joy, will write separately to introduce the volume.

10

33

693

0

10

60

Este paper muestra que el riesgo pais cae significativamente ante anuncios de ajustes fiscales, especialmente en periodos de riesgo pais elevado o cuando se da con un programa con el FMI. Esta caida es clave para suavizar el efecto contractivo del ajuste.

0

10

57

Our paper “Numerical fiscal rules for economic unions: The role of sovereign spreads” is now available online. With Juan Carlos Hatchondo and Leonardo Martinez, we show that a spread limit is a more robust fiscal anchor than a debt limit.

1

1

49

After a great experience in Mexico and

@CEMLA

, happy to go back to DC and the IMF, where I’ll be joining the Research department.

3

0

50

My paper “The adjustment to commodity price shocks” has just been published

0

5

44

Just presented my paper on Sovereign CoCos and Debt Forgiveness (joint with JC Hatchondo, Leo Martinez and Kursat Onder) at the

@SEDmeeting

#SED2023

0

2

41

Caliendo y Parro muestran que seria beneficioso para Uruguay abandonar el Mercosur y firmar un TLC con EEUU

La posición arg. es deshonrosa y desopilante. Deberían dejarnos solos. El AEC debe bajar y el Mercosur debe firmar TLC con UE, Canadá, Corea del Sur, etc. Es la vía más segura y rápida para bajar la pobreza. El presidente que no se anime no es un estadista; es un oportunista.

0

8

37

1

5

38

Just released. Our new IMF working paper on Numerical Fiscal Rules for Economic Unions. Joint with Juan Carlos Hatchondo and Leonardo Martinez.

1

9

38

No se pierdan el blog que escribimos con

@fqroldan

sobre bonos atados al PBI

Bonos atados al PBI: ¿Por qué tan caros? ¿Por qué tan pocos? | Por

@fqroldan

y

@francisco_roch

0

4

42

0

6

40

Juan Carlos Hatchondo presenting our paper on Constrained Efficient Borrowing with Sovereign Default Risk (also joint with Leo Martinez) at the

@SEDmeeting

#SED2023

0

2

39

Visiting the Econ department and feeling nostalgic (and a bit old!) looking at the pictures of the entering classes. I’ll start with mine, 2006. Great friends and economists!

@EulerEquation

@IgnacioMunyo

4

0

39

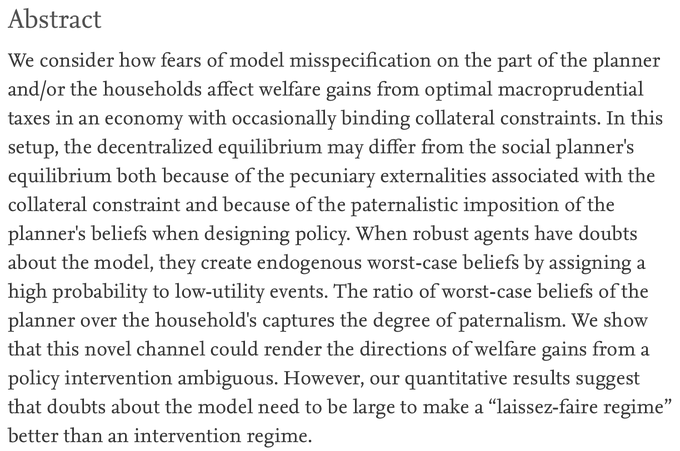

Check out the revised version of our paper on Robust Optimal Macroprudential Policy

Cambian los efectos de los controles de capitales cuando se aplican a un modelo incorrecto?Encontramos que mientras que el error de especificación no sea muy grande, estas políticas son socialmente beneficiosas.

Por Federico Bennett, Giselle Montamat y

@francisco_roch

1

5

21

1

3

37

Great news indeed! Very happy to be part of this fantastic editorial team led by Andrei Levchenko and Prachi Mishra!

Great to see the IMF Economic Review increasing its impact factor (IF) from 2.5 in 2021 to 4.3 in 2022!

The 5-year IF is now at 3.9.

More information on the journal here:

@francisco_roch

@IMFNews

0

7

60

0

2

36

New blog post on

@LSEforBusiness

. With

@fqroldan

we discuss why GDP-linked bonds have been used so scarcely and severely underpriced. Check it out!

1

8

35

Happy to have contributed to this recently released policy paper

2

2

33

Very interesting and timely panel on inflation with

@cristinarellano

, Silvana Tenreyro and

@IvanWerning

, including some discussion on Argentina and dollarization.

#IEAWC2023

0

1

32

Check out our new working paper (joint with Juan Carlos Hatchondo and Leonardo Martinez)

0

3

30

Para informar un poco sobre el FCL del FMI:

The qualification criteria are the core of the FCL and serve to show the IMF’s confidence in the qualifying member country’s policies and ability to take corrective measures when needed.

2

9

30

In two recently published papers (links below) we study precisely common fiscal rules for a Union of heterogenous economies. We show that a common limit on sovereign spreads can generate welfare gains across economies in the Union. A common debt limit does not!

1/6. Christian Lindner is right to insist on common fiscal rules. But he misunderstands the implications. Common fiscal rules do not imply identical desirable paths. Countries are different in many ways, all of them relevant.

3

70

220

1

4

29

En esta entrada de FE pueden leer sobre lo que voy a hablar mañana

El BCRA brindará un seminario de economía a cargo de

@francisco_roch

, de

@CEMLA

Jueves 9/8 a las 15.30 hs. Reconquista 250 CABA.

#SeminarioBCRA

0

7

16

0

5

27

Check out our new WP on the optimal use of central bank tools, joint with Suman Basu, Emine Boz,

@GitaGopinath

and

@dfilizunsal

Just put out some new research on policy making in emerging markets and developing economies faced with global financial shocks, dominant currency pricing, and currency mismatch on balance sheets. The paper is here: . A blog is here:

3

28

137

1

4

28

Check out our recently published paper! We extend a model of occasionally binding constraints à la

@JavierBianchi7

to allow for model uncertainty

by applying the robustness framework of

@UncertainLars

and Sargent.

New: "Robust optimal macroprudential policy" by Federico Bennet(

@frbennett13

), Giselle Montamat and Francisco Roch(

@francisco_roch

). How is macroprudential policy affected by fears of model misspecification?

1/2

2

13

50

0

4

27

Just released. Our new IMF working paper on Robust Macroprudential Policy. Check it out!

0

3

26

Happy to share my F&D article on the value of fiscal policy commitment. Check it out!

2

3

24

El crack de

@fqroldan

presentando nuestro trabajo sobre state-contingent debt

Antes de cada presentación hay que recordar el consejo de Sargent:

Just be yourself. But don't speak too fast

3

0

62

1

0

23

Sargent la semana pasada en UTDT contaba que solo haber aprendido IS-LM "it's a handicap"

Aprendés IS-LM y te vas con las sensación de que sabés macroeconomía. Movés curvitas de un lado para el otro, sube la tasa de interés, baja tal cosa, pim pum pam y listo. Lo cierto es que no, no sabés mucha economía moviendo las curvitas del IS LM. Es más complejo.

25

14

287

1

1

24

Completely agree! However, in two papers with Hatchondo and Martinez we argue that it may be hard to implement a fiscal rule anchored on a common debt level for a union of heterogenous economies. The spread level is a more appropriate anchor.

A monetary union needs a good fiscal union and fiscal rules are an important piece of that.

6

9

97

3

0

24

Preparing a discussion on state-contingent debt instruments for a workshop organized by the UNCTAD and the ECLAC on Innovative Financing Instruments. Will rely heavily on my work with

@fqroldan

. You can access a non-technical piece in this LSE blog post

1

5

23

Los espero el lunes 22 a las 12:30pm en

@UCEMA_edu

donde presentaré el trabajo “Constrained efficient borrowing with sovereign default risk” (coautores: Juan Carlos Hatchondo y Leonardo Martinez)

0

3

21

Taylor: “...while interest rate rules work well to keep inflation low in a low-inflation regime, getting inflation down from high levels to low levels is a transition issue which raises other concerns.” “the role of quantitative instruments such as the monetary base is crucial.”

2

3

21

Comparto mi nota en Foco Económico sobre reglas fiscales

2

9

21

Visit to my alma matter! Always great to see the advisor and former professors!

0

0

19

After almost 6 months of enjoying this view, time to go back to DC!

1

0

18

Glad to have participated in this great conference! I discussed a ver interesting paper by

@TimTkehoe

and coauthors on the role of shocks to the risk-free rate on default incentives. We need to think more about the relationship between external shocks and haircuts!

Finalizando un muy enriquecedor XXIV Workshop in international economics and finance organizado por

@EconomiaDiTella

en el Banco Central del Uruguay. Contento de reencontrarme con amigos.

@GerardoLicandro

@andyneumeyer

@TimTkehoe

@francisco_roch

y muchos otros más.

2

2

60

0

3

17

In this paper we develop a tractable model that characterizes the optimal joint use of these policies (monetary policy, foreing exchange intervention, capital controls and macroprudential regulation). (2/2)

1

4

16

Me senté a tomar un café en Bogotá y me sugiere seguir la libertad para una vida llena de significado 💪

3

0

17

No se lo pierdan! Espero que haya streaming

@UCEMA_edu

"Inflation Targeting in High Inflation Emerging Economies".

Muy buena esta conferencia de John Taylor (si, el de la regla) en el CEMA el próximo jueves 29/11 18:30.

(Lástima que a esa hora ya no habrá transporte público por el G20)

1

7

50

0

2

17

Mi primer documento de trabajo en RedNIE

En respuesta a la pandemia de COVID-19, la mayoría de las economías han implementado programas de estímulo fiscal que llevaron la deuda pública a sus niveles históricos más altos. Estos desarrollos puesto las estrategias de desapalancamiento al frente de los debates políticos.

1

0

4

0

0

16

Today

@fqroldan

and Jeromin will be presenting our chapter on Sovereign Debt (also joint with Leonardo Martinez). Check out the conference program and follow live on YouTube.

The Research Handbook of Financial Markets Conference

November 1-2, 2021

Online conference organized by

@BilkentEconDept

and

@cepr_org

For conference program, registration and more information:

0

3

25

0

0

15

Check out our piece with

@fqroldan

on GDP-linked bonds featured in the latest edition of the IMF Research Perspectives

🆕 Download the latest IMF Research Perspectives newsletter: "Solving for the Recovery." Our Spring/Summer 2021 issue offers insights on how we can solve the puzzle of building back better.

0

4

20

1

1

15

Fantastic new issue of the IMF Research Perspectives! Glad to have contributed with an article featuring our paper on Sovereign CoCos and Debt Forgiveness. Check it out!

1

2

15

Correct link to our

@voxeu

column. Joint with Sakai Ando, Giovanni Dell'Ariccia,

@pogourinchas

,

@guido_lorenzoni

and Adrian Peralta. Check it out!

This

@voxeu

column estimates jointly issued

#euroarea

debt of 15% GDP could be issued without fiscal transfers

•

A free lunch! the “convenience yield” on a euro area safe asset

•

@pogourinchas

@IMFNews

1

2

10

0

11

14

En este capitulo del Regional Economic Outlook complementan el analisis y muestran que el efecto en el riesgo pais es todavia mas significativo si el ajuste se hace por via del gasto que impuestos.

Este paper muestra que el riesgo pais cae significativamente ante anuncios de ajustes fiscales, especialmente en periodos de riesgo pais elevado o cuando se da con un programa con el FMI. Esta caida es clave para suavizar el efecto contractivo del ajuste.

0

10

57

0

1

14

Great conference program that can be attended virtually as well! My coauthor Leo Martinez will be presenting our paper Constrained Efficient Borrowing with Sovereign Default Risk (also joint with JC Hatchondo). Check it out!

Coming up Tuesday, 27 June: First Colombian Conference on Fiscal Policy at

@EconomiaUAndes

:

Mark Aguiar, Juan Jose Ospino,

@c2granda

, Guillermo Vuletin, Leonardo Martínez,

@paures12

,

@TimTkehoe

.

0

12

45

1

2

14

Siempre orgulloso de ser graduado de UCEMA, 2da en el ranking RePEc en Arg

@carod2015

@alerodri1976

@CemaCalixto

2

7

13

4 prerequisites for successfully adopting inflation targeting, according to the IMF:

1) Institutional independence. The central bank must have full legal autonomy, and be free from fiscal and/or political pressures that could create conflicts with the inflation objective.

1

2

12

"the more dynamic, uncertain and ambiguous is the economic environment that you seek to model, the more you are going to have to roll up your sleeves, and learn and use some math."

La economía se formaliza con matemática. Es una herramienta para poner los supuestos sobre la mesa y que todo sea transparente. Si querés charla y prosa, elegí otra ciencia social.

37

78

560

1

0

11

“El régimen de metas de inflación puede ser perfectamente razonable una vez que la inflación haya convergido a niveles bajos y que el BCRA tenga mayor credibilidad ... en la transición hay que establecer un ancla mucho más sólida para las expectativas”

1

1

12

Joint work with

@haralduhlig

ICYMI in a BFI Working Paper,

@UChi_Economics

'

@HaraldUhlig

and Francisco Roch examined "The Dynamics of Sovereign Debt Crises and Bailouts"

0

0

2

0

1

11

En su libro, Vegh muestra que se requiere mucha más credibilidad en un plan de estabilización bajo esquema IT que con ancla cambiaria o de agregados. Igualmente en los tres es clave bajar el déficit fiscal.

En un IT lo clave es que la inflación termine estando en el rango que dice el BC. Sino, no funciona, guste o no. Es claro que Arg. no está en esa situación. La inflación se bajará más rápido con un ancla fuerte (y que la maneje el BCRA) y fácil de entender para la gente.

4

3

11

1

1

11

Seems like a good moment to recall this piece I wrote about the value of commitment for the success of fiscal consolidation plans

Happy to share my F&D article on the value of fiscal policy commitment. Check it out!

2

3

24

0

1

12

Great luncheon address! Check it out in the link below. The lecture starts at minute 40. Don’t miss it!

Just gave the AEA Joint luncheon address on “New Foundations for Macro Policy” Great to see old friends, including brilliant women

@Susan_Athey

, President of AEA, &

@skalemliozcan

.

21

54

1K

0

0

10

Hoy tenemos a

@DavidKohn_16

hablándonos sobre Financial Frictions and Export Dynamics in Large Devaluations. No se lo pierdan!

Today's

#Webinar

: Financial Frictions and Export Dynamics in Large Devaluations by

@DavidKohn_16

Oct 3, 12:00 EDT

0

3

4

0

0

10

Reforzando lo de Mauro.

FCL no tiene conditionality. El PLL tiene “focused conditionality”:

“under one- to two-year PLL arrangements, prior actions, structural benchmarks, and quantitative performance criteria will only be used when they are critical for a program’s success”

1

1

9