Brandon Carl

@brandonjcarl

Followers

4,895

Following

528

Media

378

Statuses

2,602

Markets, Macro, AI, Tech. Head of AI + Strategy at @SmarshInc . Previously CPO/Head of AI Research @dreasoning , Global Macro @nomura . All opinions my own.

Nashville, TN

Joined March 2009

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Trans

• 367097 Tweets

#EndBadGovernaceInNigeria

• 334801 Tweets

Imane Khelif

• 318837 Tweets

無課金おじさん

• 268856 Tweets

Japão

• 160493 Tweets

#IStandWithAngelaCarini

• 147942 Tweets

Kano

• 134756 Tweets

Félix

• 133470 Tweets

The IOC

• 120737 Tweets

トランスジェンダー

• 83375 Tweets

Italiana

• 75363 Tweets

Evan Gershkovich

• 74166 Tweets

#OurRockStarMarkDay

• 73081 Tweets

#마크생일_200만큼_축하해

• 70044 Tweets

Paul Whelan

• 65661 Tweets

HIKAKIN

• 58397 Tweets

Gabi

• 57635 Tweets

Algeria

• 56573 Tweets

ヒカキン

• 54208 Tweets

女子ボクシング

• 54034 Tweets

mark lee

• 50881 Tweets

South Park

• 46760 Tweets

Alcaraz

• 44038 Tweets

TZUYU

• 37919 Tweets

The Wall Song

• 35756 Tweets

ana cristina

• 19475 Tweets

ボイスサンプル

• 17261 Tweets

Argelia

• 15121 Tweets

Busenaz

• 14015 Tweets

ウルフアロン

• 13352 Tweets

NO ONE LEAV1NG

• 12794 Tweets

女子バレー

• 11849 Tweets

Pinned Tweet

2023 Investment Recap

What Worked

• OSCR (+167%)

• TALK (+186%)

• COIN (60% on structure, 400% on spot)

• Grayscale Convergence (350%)

• TLT (12%)

• Municipal CEFs (18%)

• Bank Preferreds (73%)

• Gen AI (this got stupid)

• PINS (78%)

What Didn't

• AGNC Preferred vs

5

0

13

@DavidSacks

@elonmusk

That’s not right David. You can test the error with a binomial distribution. This is the Law of Large Numbers.

Twitter samples 9,000 per quarter or 36,000 per year.

At 5% sampled mean the standard error is sqrt(5% x 95%/36K) = 0.36%.

Twitter is right.

133

72

4K

One of the most illuminating papers you can read on The Great Depression is Martha Olney's

"Avoiding Default: The Role of Credit in the Consumption Collapse of 1930"

By putting yourself in the shoes of then-consumers, things start to make sense...

1/5

15

145

814

A few very interesting add-ons reading through the investor deck for JPM/FRC.

This deal appears to be a *fascinating* feat of financial engineering.

1/5

10

66

265

The game theory around First Republic, the FDIC, the banks and the White House is a bit crazy.

When you walk through it, today's announcements from the FDIC and the US Government make sense and may be an attempt to get the banks to recapitalize FRC.

1/12

5

46

221

When you look at the Fed's H8 data for Small, Domestically Chartered Banks, you can see exactly what happened...

First, the run on deposits: $250 billion over two weeks.

1/5

6

31

181

@rscotteisenberg

@DavidSacks

@elonmusk

The standard error describes the margin of error for a sampled mean.

Population size isn’t part of the computation. The size of the sample is.

A multiple of your standard error gives you the confidence interval.

The Law of Large Numbers is why it converges. Hope that helps.

5

4

167

So many people on Twitter are confusing coupons with convexity right now.

Yes - there’s an asymmetry to 20 years falling by 20 bps vs rising. But the majority of this is due to coupon, not convexity.

Moreover - if you want to do proper bond math you need to account for:

•

8

25

159

Let's take a quick look through First Republic, and how they're navigating.

To begin, uninsured deposits fell hard (by nearly $100 billion), but are now stabilizing after banks added $30 billion.

Why? Only $19.8bb is now uninsured and the flight risk is now much lower.

1/10

8

30

160

But consumption decreased a lot.

The small print matters. And Prisoner's Dilemmas can have major impacts.

By 1938 the terms of default had largely changed and we prevented a similar situation.

Worth a read.

7

8

141

The math on this is wildly incorrect. I would encourage you to correct and retract this

@mikealfred

.

If you look at the increase in the actual debt maturing the payment goes up by 22% versus 100%.

If you look at the interest payments versus Federal Tax Receipts (total, not just

Roughly half of all Treasuries outstanding today will mature by the end of 2025.

The current average interest rate on federal debt is 2.6%.

The current prevailing interest rate is over 5%.

If nothing changes, the US government will be forced to refinance this debt at roughly

117

339

2K

10

12

141

@maxjanderson

Interesting analysis but you don’t need Net Liquidity. You’re largely just looking at FRB Reserves Balances.

Assets - RRP - TGA

= (Liabilities - RRP - TGA) + Capital

= Reserves + Currency + Other + Capital

Reserve changes is how policy is designed to work.

CC:

@dampedspring

2

10

117

People tightened their belts on consumption in order to not lose their equity in key items.

This began a spiral: decreased consumption led to economic slowdown led to layoffs led to decreased consumption.

Default rates on cars increased, but not remarkably.

4/5

2

12

116

How Microstrategy funds for so cheap…

1. Buyer buys the converts

2. Sells long-dated high strike calls against it

3. Receives small coupon

Because vol is so high buyer covers all of credit risk.

Pure arbitrage at the expense of retail traders.

Hat tip

@macrogliblyglo1

6

12

101

In the late 1920s people had taken out a large number of loans for autos, appliances and pianos.

These loans were typically 12 to 24 months in duration, with 10 to 40% down payments, and remarkably high interest rates.

Debt was new.

2/5

1

6

98

This is one of my favorite charts to look at.

Deposits, Stocks + Bonds held as a % of Disposable Income vs the 10Y inverted Treasury Average Yield. Data is through Q2: recently would be 4.50+.

You can immediately see a few key things:

(

@concodanomics

inspired by your 🧵s)

1/6

5

17

84

The issue was the structure of debt.

Contracts typically did not allow for you to sell your durable good to pay off the loan.

Moreover, if your durable good was repossessed, you often lost the surplus.

1

5

83

This is actually the system working the way it's supposed to against exogenous shocks.

I expect there will be earnings hits this quarter but that the sales may also help with capitalization ratios.

5/5

8

2

74

People that are laser focused on JOLTS misunderstand the economic situation. There are structural (vs business cycle) factors at play. Let me outline the specifics of why and what to do.

1. The Labor Force has returned to pre-pandemic levels.

5

19

71

@alexstanczyk

@joerogan

@PeterZeihan

Alex - much of what he is saying is correct. These are fundamental economic principles.

The technology is awesome - but he’s right that fixed supply does not support growing economies.

I may write more on this, but if you fast-forward the following economic equation it highlights inherent issues with Bitcoin as *the* universal currency

Money Supply x Velocity of Money = Real GDP x Prices

This is typically expressed as MV = PY

@michaeljburry

@balajis

1/5

2

0

8

29

3

67

@CloudsGalore

@DavidSacks

@elonmusk

That’s only true if the entire population turns over each day which is not the case. There will absolutely be correlation.

There will be some attenuation, but each day is not it’s own analysis. That would assume daily population independence.

3

0

54

The moment we've all been waiting for. M2 YoY is now negative.

Pretty rare occurrence and exactly what you'd expect given the Fed's position.

3

11

56

Good journalism by

@ericwallerstein

.

If this is a speculative attack (which it appears to be) - it's reprehensible. No nice way to put it.

Back-to-back records for put options on PacWest. 125k contracts traded Monday, 190k on Tuesday with time to spare.

$PACW

@WSJmarkets

:

12

21

129

13

14

54

Fathers be good to your daughters.

As the father of an 8 year old girl this has my attention more than ever.

Thanks

@donnelly_brent

for first tipping me off to this.

13

6

52

By far, my favorite question at any point in the investment cycle is this:

“How much has to go right to justify this valuation?”

Or more mathematically:

“What percent of plausible future states would justify this valuation?”

8

8

53

This isn't a prediction. But there's so much fear-mongering on Twitter that I wanted to walk through solutions.

None of this is easy, but it's not impossible. You've got to concurrently keep your culture in place and staff motivated.

I wish the leadership team the best.

10/10

6

3

51

Altogether, when you:

- Lower capital costs

- Provide positive NIM

- Lower risk

... you can get unusual gains. Details are here:

5/5

3

4

47

@DavidSacks

As you know - the securities can be worth less than the deposits in a rising rate environment.

So the product you’re describing would still have risk of a run.

1

0

47

Feat 2: Re-orienting the creditor stack.

Uninsured deposits being made whole while the FDIC is taking losses.

Technically you'd go: insured deposits, FDIC, uninsured deposits.

Instead we are going: insured deposits, uninsured deposits, FDIC.

Aligns with previous deals.

3/5

1

2

45

There are a few things that are easy to overlook in these sorts of analyses. The thread below is well-intended but misses the mark.

1. The tech sector is now much more mature and diversified than it was in the late 90s.

You need an inferred multiplier:

P/E Observed =

P/E for

2000 peak vs now:

Tech sector traded at 2x its profit share vs 1.25x now.

SPX was at a 25x forward P/E vs 20x now.

Translation:

S&P 500 would need to reach 6250 to price-in same level of irrational exuberance as 1999-esque - per Soc Gen

103

122

521

2

4

44

This is exactly the sort of mechanism by which Fed policy is supposed to work (among others).

Debt rollover takes time. Asset reallocation takes time.

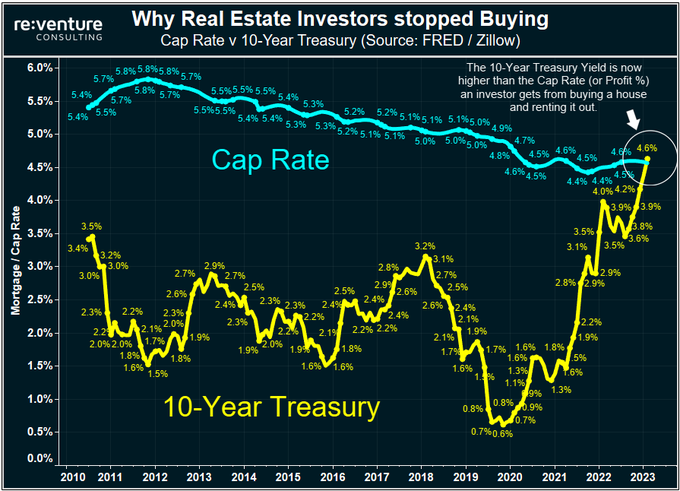

Here's an ominous indicator for the Housing Market.

The 10-year government bond now yields a higher return than the Cap Rate, or profit from operating a rental property.

No wonder real estate investor demand is collapsing. More profitable to buy bonds.

81

430

2K

2

5

38

4. Why aren’t these workers returning? We can see that disabled individuals increased during COVID by 3 million, which more than explains the shortage.

Remember that such individuals often need caretaking (which also helps explain the need for healthcare workers).

4

8

42

@BillAckman

@federalreserve

Bill - you were actively pushing for large hikes in Q3.

Were you expecting a different outcome than what's transpired? Honest question.

is a fiction. Rates are going up a lot soon. The sooner the Fed quells inflation, the better for longer-term bonds and long-term financial assets like equities. Don’t be misled by short-term, technically driven market movements. Stocks of high quality businesses with long-term

9

38

624

7

3

39

@Mattfox68569363

Fabozzi's Fixed Income is the canonical work.

However there's a 6 part series by Antii Ilmanen many years back that I found to be the best work.

2

2

38

There are three possible responses to this:

1. Sufficiently drop aggregate demand / GDP so that the workers aren’t needed.

2. Public programs to rehabilitate the disabled.

3. CapEx investment and automation.

There’s too much focus on

#1

. Shrinking an economy is bad policy.

8

5

38

$880 billion of potential fraud from pandemic relief programs.

This is the size of 2008 bailout but entirely fraudulent.

It’s no wonder prices of Rolexes, Lambos and Airbnb properties went to the moon.

3

11

36

As the bond market rallied, this enabled them to begin selling off some of their securities portfolio: $168 billion.

There were also circa $70 billion in loans sold, ostensibly in private transactions.

3/5

3

4

36

For full sake of clarity.

1. If the stock rallies like crazy they have a free call spread.

2. If it stays put and Microstrategy doesn't default they're paid both principal and call premium for massive ROI.

3. If they default they recoup most if not all losses via calls sold.

1

2

33

Feat 3: Lots of wins

- FDIC paid $10.6B by JPM

- JPM recognizes gains of $2.6B

- JPM 20% IRR and $500mm net income accretion

- Tangible book value accretive

- Capital ratios intact

- Everybody gets deposits back

4/5

1

3

36

Feat 1: "Transforming" high risk, high funding to low risk, low funding.

The FDIC loss-share reduces risk-weighting on covered loans to 25% - *far* lower than typical for these assets.

The FDIC is also providing fixed-term financing of $50 billion.

2/5

1

2

35

Sigh, major factual error.

The specific coffee series that was removed was last published in 1988. It’s still in the CPI, just not with a specific can size.

Again: be careful when people start with the narrative and use data to back it. Details matter.

Why is the

@BLS_gov

removing the price of coffee from the inflation report?

Coffee is an important part of America prices, almost as important as gas prices (we already exclude gas) and we are removing it from the CPI INFLATION REPORT!

H/t

@DonMiami3

50

104

376

3

2

36

Many people are talking past each other on SVB.

Why? The situation is complicated - and both the Points and Counterpoints can be true at once. I’ve compiled many I’ve heard below.

What’s important is to resolve this in a manner that mitigates financial and technology contagion.

3

11

35

To accommodate this drop, they increased borrowings (likely FHLB, Discount Window, BTFP) by $297 billion.

2/5

1

1

34

An important lesson I saw on Wall Street.

Markets teach humility. Everybody is wrong, a lot. Those who realize this, are willing to change their mind, and adapt: survive. Those who do not, do not.

Very few career paths force this kind of adaptation.

0

4

33

Great article by

@FedGuy12

.

This aligns with the point I've been making. IOER and massive excess reserves stunted the transmission mechanism of hikes similar to the way that Reg Q stunted Burns' hikes.

For hikes to impact, Powell needs to increase QT instead of more hikes.

2

5

31

With the runs slowing, borrowings have now fallen back by $125 billion.

4/5

2

1

31

To put the potential China bailout into context.

$280 billion is 4 times the record ETF inflow of last year.

It is about 9x the largest net investment inflow via the Stock Connect program.

As a percent of total market capitalization it’s much higher yet.

Breaking News: Bloomberg has learned Chinese officials are considering a market rescue package in the order of $280B. Markets responding nicely initially.

Details to follow. Stand by.

49

180

751

2

6

31

There are two questions it’s important for you to answer

@balajis

:

In your Bitcoin maximalist world:

1. How do you prevent debt-deflation cycles?

2. How do you propose to address trade imbalances with a fixed currency?

VOTE FOR BITCOIN

The post below by

@MacroScope17

is excellent. Let me extend his point one step further: the real election is BTC vs USD, the primaries have already started across the world, and every ballot counts. So make sure to vote early and often. Here's why this is more

212

702

3K

14

2

29

All views my own – I'm just trying to piece together why the series of news articles emerged that did.

12/12

9

0

30

As far back as I can remember I have been able to see macro trends clearly. However - most of that time I have been a terrible portfolio manager.

In the last few years I've changed markedly. My wife asked me lessons learned – which I thought I'd share here. I'm not sure why

2

4

27

Post-mortem on First Republic:

- JPMorgan acquires/assumes all deposits

- Doesn't assume preferred/unsecured notes

- Loss-sharing w/FDIC (details below)

- Est. FDIC loss of $13 billion

- One-time gains of $2.6 billion for JPM

1/7

1

6

26

The reason that this can work is because most of the assets on First Republic's balance sheet are likely money good. This is in huge contrast to the 2008 Global Financial Crisis.

Most assets will revert to par over time.

9/10

There is a lot of misunderstanding about how bonds and mortgage securities work.

I put together this diagram so that people understand:

bank "mark-to-market" losses on their Held to Maturity Portfolios will self-correct, even if rates stay high.

1/10

1

2

9

2

6

26

Liabilities: the bank is heavily funded by the Fed, FHLB and big banks.

To put it in content: $135.9 billion of $215.0 billion (63%) of liabilities come from government- and GSIB-related activities.

This will compress NIM, but it will be sticky + reduce liquidity risk.

3/10

2

6

26

3. We can see this in the Labor Force Participation Rate. This has dropped by about 0.75% of 164.5 million, or about 1.25 million workers.

1

4

27

@RaoulGMI

You’re missing the fact that they did very little interest rate hedging, which is uncommon for a bank portfolio.

6

0

27

@LTCM_ETF

Coupon being the recurring payment that the bond pays out,

In bond markets carry is calculated as the difference between short-term borrowing costs on a security vs the cash paid out via coupons.

Since short rates are higher than long-dated yields that is negative right now.

0

1

24

@taobanker

This comes from the Taylor series decomposition.

Duration is the first order approximation of the change in price versus the change in yield. First order linear approximations are by definition symmetric.

The convexity term is the second order part, which is asymmetric.

1

1

25

Finally - we can also normalize by assets to look at the composition.

You can see that:

1. Deposits have trended lower over time

2. Stocks are near secular highs

3. Bonds are near secular lows

6/6

1

3

25

To begin: Wedbush had estimated that First Republic's tangible book value if marked fully to market would be negative $73/share.

If correct, the $13.5 billion capital hole is what creates an issue for any prospective buyer.

2/12

1

1

26

Short note on how the First Republic Bank “rescue” works. There is a ton of confusion out there: my goal is to help quell panic.

As of Dec 31, 2022 the bank had $4.23 billion of cash and cash equivalents.

This makes sense: as a bank your deposits are pretty “sticky”.

1

3

25

2. And yet, in spite of Fed hikes, job openings are near cyclical highs. Demand for workers outstrips supply.

1

4

25

“What’s going on nationwide is every one of these banks has either frozen their loan-to-deposit ratio or, more likely, is very intent on shrinking it”

Former Dallas Fed President Robert Kaplan

0

8

25

The market is up 11% since this call.

Tech outperformed to the upside with AI being the major driver.

Short-term, the easy money has been made on this. Long-term the thesis holds. I'm largely in uncorrelated bets that should trend higher over time.

On the complete opposite side of MS: I’ll bet we print at least 4500 SPX sometime this year.

Tech will outperform to the upside.

1

0

5

6

0

23

@rleshner

This is patently false.

Study history. DeFi does not work.

The reason is human nature: greed creates leverage and fear creates contagion.

There must be an uneconomic buyer of last resort. The longer it takes to relearn this lesson, the more painful.

7

1

22

@parthiv645

@DavidSacks

@elonmusk

We know as sample sizes goes up the margin of error goes down.

In stats the population size isn’t relevant in the margin of error.

If you have a new method or reason to overturn stat theory, please do post.

3

1

22

In March, a bank consortium deposited $30 billion in uninsured deposits (this is key) for an initial term of 120 days.

This mitigates liquidity issues for First Republic. As of April 21, 2023, they had $45.1 billion of cash/equivalents + unused available borrowing capacity

3/12

1

1

22

Impressive results out of JPM

Consumer/Community Banking Net Income +80% YoY

Importantly, look at Loan Loss Reserves: they increased, but decelerating

This tells you that JPM had room within their earnings to increase them by even more, and chose not to

@BickerinBrattle

👏

1

4

20

On Wall Street this is known as “picking up nickels in front of a steamroller.”

Option Selling helps me generate $1000s per week in cash flow

My sweet spot for selling options is Delta 0.15 to 0.25

Let's talk about the benefits of selling options with a delta of 0.15 to 0.25

👇👇👇

37

59

455

5

0

22

4 step plan to fix the economy:

1. Fed to start leading + stop reacting to data

2. Launch Supply Chain Lending Facility w/ 0% interest rates to mitigate capacity issues

3. Drain excess cash in a targeted manner (tax hikes on very wealthy)

4. Fix issues w/ OER/CPI + housing

3

5

22

The net effect is that you recapitalize some of the $13.5 billion – wait out the losses on the assets (which eventually will be made good), and try to profit from upside on the warrants.

Which certainly sounds better than losing up to $30 billion.

11/12

1

0

21

From Dick’s Sporting Goods earnings.

”Profitability was short…due in large part to…inventory shrink (theft)”

5

3

18

This is a bank doing banking things.

They were hit because of VC deposit flight, which they replaced with brokered deposits (smart) and began sale of certain assets (smart).

Banks by their nature are prone to speculative attacks. Don't put people out of business to make a buck.

1

3

21

This is where it gets interesting.

If at the end of 120 days the banks chose not to roll over their deposits, First Republic would pledge assets to the FHLB and Fed to tap additional borrowing.

The collateralization is a key fact.

4/12

1

1

20

In May I'd indicated PacWest was under speculative attack and w/time they'd find a path forward.

Today marked their merger with Banc of California. All deposits honored, all liabilities honored, and preferreds honored. Common diluted - which is the way the system should work.

Good journalism by

@ericwallerstein

.

If this is a speculative attack (which it appears to be) - it's reprehensible. No nice way to put it.

13

14

54

1

1

19

This looks to be a pre-written essay by Russian Media celebrating a successful military outcome in Ukraine restoring the unity of Russia, Ukraine and Belarusia. Sources at the end of the thread.

"Russia's military operation in Ukraine has ushered in a new era." 1/5

1

5

19

It's been nearly 15 months since I expressed this view.

I am now beginning to see *early* signs of necessary conditions for a recession.

I'll share a contrarian view

Predictions of a near-term major recession will be wrong. Companies leaning into growth will be rewarded.

• Consumer, corporate + bank balance sheets are strong

• Consumer + corporate debt servicing is low

• Corporate balance sheets are strong

1

0

2

5

0

20

The recent banking situation is going to have broader impacts than most realize.

I’ll outline 4 key changes below and how this will drag on growth.

In a different thread I’ll highlight why this should translate into the Fed being done.

No pictures: this is dense.

1/6

2

7

20

It’s very hard to understand how this 30%+ return was not insider trading.

“On March 17, Representative Nicole Malliotakis, Republican of New York, bought shares of New York Community Bancorp after private discussions with New York State bank regulators.”

From NYT and WSJ

1

6

19

In this thread, I'll make a case for why the Fed should be done hiking, covering:

1. Importance of transmission mechanisms

2. A surprise reason Arthur Burns failed

3. The shift from fractional banking

4. How the bank runs unclogged policy

5. The danger of hiking more

1/14

1

2

19

So the government leaks that they are currently unwilling to intervene on First Republic as a clear signal to the banks.

As the banks you now have two options: see who blinks first, or act.

8/12

1

2

18

When the economy is slowing so fast that FedEx can’t forecast, the Fed isn’t creating stability.

This is just getting dumb.

The Fed’s number one job is stability. Price stability is one part of a larger stability equation.

To overtly try to drive equities lower creates instability. Companies cannot plan with instability.

If the market gives the Fed what they’re asking for history will not be kind.

6

2

9

2

7

17

What’s happening in housing right now reminds me a lot of oil in 2007.

At the time people thought that oil was under supplied and that the replacement cost meant we wouldn’t go below $80.

Three things they missed:

1. Investors had bought up a ton of the inventory

2. Those

4

0

18

So if you're the FDIC you threaten to downgrade the scoring condition so as to limit borrowing from the Fed/FHLB.

Now in the event of receivership: the banks lose up to $30 billion because they are unsecured.

The FDIC gets away rather unscathed.

6/12

1

0

18

If you wait and the government blinks, then you may get your deposits back or a better funding deal on asset purchases.

If they don't blink, you're back to losing up to $30 billion.

And in either case, you've upset the hand that feeds you IOER.

9/12

1

1

18

If I were in Powell's seat, this is what I would convey:

"We are seeing broadly that banks plan to tighten their lending conditions. This does a good bit of work for us and places rates further into restrictive territory than they were in April.

As such, at the current time we

2

3

17

Tell me you don’t understand math without telling me you don’t understand math.

Let’s break it down:

$3mm/BTC x 21mm BTC = $63 trillion

This is:

- 2x the total amount of Treasuries

- or 3x the total M2 money supply.

Let’s assume for the moment this is a currency. The

If you’re willing to sell your Bitcoin for less than $3,000,000 per BTC, you don’t actually understand Bitcoin yet.

219

110

1K

3

4

17

This is both chart crime and a crime of understanding.

Chart crime: you have to normalize by Nominal GDP, Bank Assets or Money Supply. The number will still show an increase but much more metered.

Understanding crime: the BTFP created a major funding arbitrage where banks

The GFC bailout looks like just a blip on the radar vs what the Fed is doing today to support the banks with liquidity via loans/facilities.

And we wonder why the market is up.

This chart blew me away.

75

488

2K

2

2

17

This is terrible analysis, misinformation viewed 200K times.

Deposits fell from $375mm to $343mm QoQ or 8.5%, not 30%. YoY analyses conflates shifts to MM funds.

The stock rallied because CET1 ratios are strong.

Charles Schwab lost 30% of their deposits.

Stock rallies.

All the proof we need that the banking crisis is over.

113

112

1K

3

3

17

In the event of receivership (not expressing a view), the Fed and FHLB can (to my knowledge) seize the collateral against the loans.

This leaves fewer assets for the FDIC to sell – which would translate through into the FDIC carrying more losses.

5/12

1

0

17

WaFd one of the first regional banks to report w/loan originations -55%+ YoY ($1bb vs $2.2bb)

“Net loans outstanding grew…due to funding of…loans previously originated” but “the Company has intentionally slowed new loan production given the uncertain…environment”

The recent banking situation is going to have broader impacts than most realize.

I’ll outline 4 key changes below and how this will drag on growth.

In a different thread I’ll highlight why this should translate into the Fed being done.

No pictures: this is dense.

1/6

2

7

20

1

5

16

Generative AI will prove to be one of the most deflationary forces of our lifetime.

Governments will spend against it in order to balance the social impacts.

3

1

16

I get a very different valuation metric for S&P than

@RayDalio

has outlined here.

He indicates a similar methodology to my own but with very different results.

This measure calculates the earnings growth rate that is required to produce equity returns in excess of bond

Having been through many bubbles over my 50+ years of investing, about 10 years ago I described what in my mind makes a bubble, and I use that to identify them in markets—all markets, not just stocks.

Read what my bubble gauge says about the current

48

231

1K

4

0

16

@PoliticalIndepe

@FedGuy12

@Siddharta9

That’s actually incorrect versus accounting standards

@PoliticalIndepe

3

0

15

@Regenarian

@DavidSacks

@elonmusk

You’re misunderstanding.

5% is the sample mean.

= # of reviewed accounts deemed to be a bot / # of reviewed accounts

You’re calculating the proportion sampled (samples / population). We don’t need that for any of the math we’re discussing.

1

0

15

One key thing Volcker taught us.

When you need to break the back of inflation you have to maintain high rates farther into a slowdown than is normal and comfortable.

It’s the opposite of the Fed’s most recent guidance and begs the question as to political maneuvering.

3

0

16

While shopping for a new family car I pulled up some data that we know - but powerful to see.

Cars went from depreciating to appreciating to deprecating again.

During the appreciation phase it’s common for people to start to believe that the vehicle will keep going up and thus

2

2

16