Explore trending content on Musk Viewer

McDonald

• 1240083 Tweets

EP7 U STEAL MY HEART

• 439787 Tweets

#الهلال_العين

• 280836 Tweets

日本シリーズ

• 153463 Tweets

سالم

• 130736 Tweets

Neymar

• 83612 Tweets

علي العين

• 77028 Tweets

Liz Cheney

• 75994 Tweets

نيمار

• 39674 Tweets

ناصر

• 35850 Tweets

البليهي

• 32652 Tweets

curitiba

• 27544 Tweets

Paul Di'Anno

• 24989 Tweets

Iron Maiden

• 23155 Tweets

كوليبالي

• 22703 Tweets

#الاهلي_الريان

• 22344 Tweets

زعيم اسيا

• 22277 Tweets

AFIP

• 20846 Tweets

جيسوس

• 20696 Tweets

Chris Kaba

• 19709 Tweets

juanjo

• 16771 Tweets

Al Hilal

• 14552 Tweets

سفيان رحيمي

• 13307 Tweets

Daniel Penny

• 12287 Tweets

سافيتش

• 11833 Tweets

olivia rodrigo

• 11514 Tweets

فهد العتيبي

• 11048 Tweets

الشوط الاول

• 10542 Tweets

🍓ChatGPT o-1 can successfully do finance theory 😲

5

17

136

#EconTwitter

New paper with

@YuehuaTang

:

"Can ChatGPT Forecast Stock Price Movements?"

Using news headlines, we explore

#ChatGPT

's potential in predicting stock market returns.[1/7]

7

26

107

📖 My new book is out soon!

Everything you wanted to know about AI and stock markets.

The Predictive Edge: Generative AI and ChatGPT in Financial Forecasting

14

25

102

My book is out!

Generative AI and ChatGPT in Financial Forecasting

5

18

96

@ThatAkhilRao

At 14 observations you may just want to look at them with a lot of detail to see if they fit whatever theory you have in mind

2

0

69

🏆Very happy to win the best paper award!

Paper link:

1

1

67

We finally added transaction costs to the paper, and comparison with other models (including ChatGPT-4)

Homework, cover letters... stock forecasts?

University of Florida professor

@alejandroll10

says ChatGPT *might* just be a top stock picker... someday.

He breaks down his fascinating research paper on what could be the future of trading:

4

15

40

4

9

62

🏆Very happy to win the Blackrock best paper award with

@YuehuaTang

!

@UF

3rd prize in two weeks!

Can ChatGPT Forecast Stock Price Movements? Return Predictability and Large Language Models

Paper link:

4

5

64

My second post is out!

Human-Level Referee Reports Using Claude, Not ChatGPT

How to obtain harsh, helpful referee reports to improve your research; and why large context windows enable a comprehensive understanding of texts.

Link ⬇️

6

13

58

Paper with

@NickRoussanov

challenging the core of arbitrage pricing theory and questioning the trade-off between systematic risk & expected returns.

Do Common Factors Really Explain the Cross-Section of Stock Returns? Not really!

#EconTwitter

#fintwit

Higher risk yields higher returns, says an old investing maxim. Research from

@alejandroll10

and

@Wharton

’s

@NickRossanov

challenges this notion, using AI to help eliminate risk that is not compensated with extra returns. Read about the model here: .

1

0

14

1

8

53

Paper with

@YuehuaTang

on the news!

Can ChatGPT Forecast Stock Price Movements? Return Predictability and Large Language Models

#ChatGPT

#fintwit

Can ChatGPT be used to predict stock moves?

University of Florida professor

@alejandroll10

is studying that question by using the AI to parse through news headlines and if they are good or bad for a stock:

5

6

29

0

11

55

Such a nice asset pricing conference to present at!

1

4

54

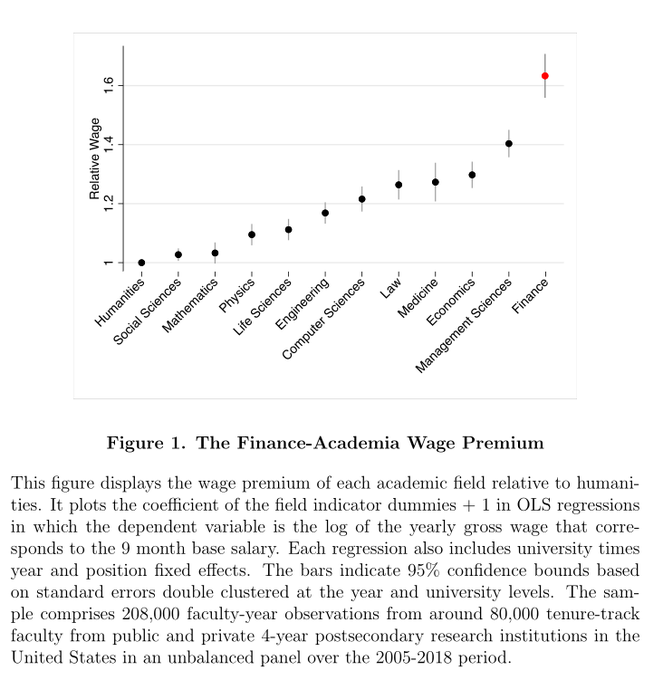

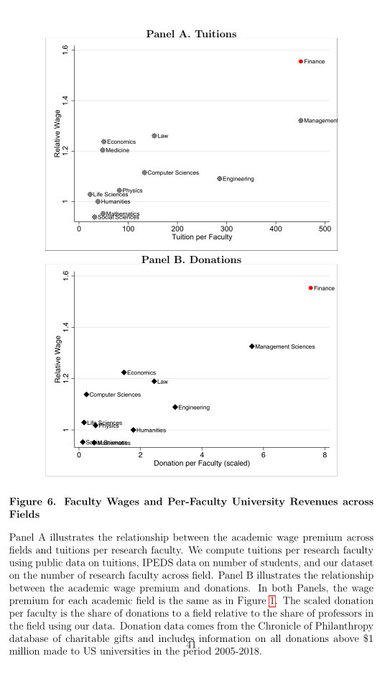

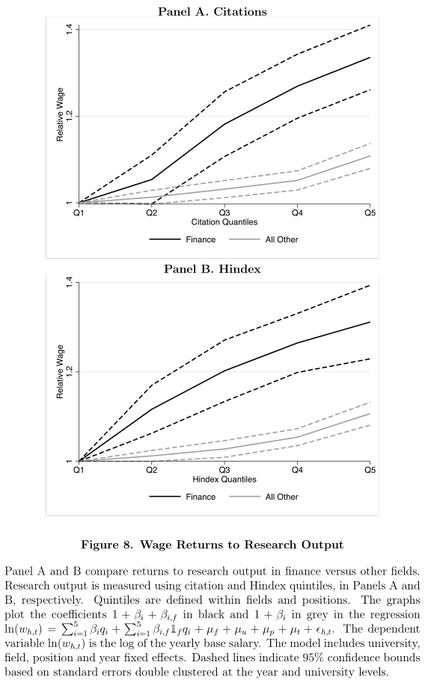

Finance professors get paid more because our students earn more income, with a high possibility of exceptional income and happily pay higher tuition and donate more! 💲💵💹

Why do finance professors get paid more? Clerier, Vallee, and Vasilenko provide some fascinating charts.

5

31

207

0

3

51

@realGeorgeHotz

@BillAckman

big opportunity here, invest in

@AMD

and make them open source drivers = Nvidia market cap

0

0

43

📢We're hiring an Assistant or Associate Professor in Finance focusing on Fintech/ML!

📚Come join our department at the University of Florida!

@UF

@UFWarrington

🎓Top Market Salaries and No State Tax!

☀️Best weather all year!

I am on the committee this year.

Link ⬇️

2

6

42

ML in finance academia is not using the latest developments. Two causes:

1. It takes time to adapt the newest techniques into working papers. You need to write it down and adapt it to an interesting academic setting

2. Referees are skeptical of exotic methods

@jarismen

@alejandroll10

I think my suspicion is that the ML stuff that academia is doing is miles away from what's being done in industry

2

0

3

5

2

42

Fantastic location for a conference! ⛰️🏞️🚠🚵♂️🧗

Alpine Finance Summit

2

1

40

@GaryMarcus

Vital: coding in python, translating code from python to R, converting between latex writings to presentations and vice versa, solving equations (via Wolfram), rephrasing thoughts

0

0

41

The best reason to use Python over R for statistics is that ChatGPT can run python code in its sandbox.

Pandas has a horrible syntax but who cares if you don't have to write it explicitly anymore.

0

0

40

🏆 Thrilled that our paper, "What If Option Closing Prices Were Trustworthy? A Machine Learning Approach," won the Best Paper in Derivatives Award!

Link:

Thread 🧵

🔍 Options lack a robust mechanism for closing prices. How can we solve this? (1/N)

3

4

37

@EconTalker

No, it's one of the best econ podcasts available. The historical archive contains more than enough econ. Much easier for people interested in econ to find it with the current name. It also helps incentive you to do some econ episodes which I love.

1

0

36

How good is ChatGPT at predicting returns and is it profitable to implement them?

I elaborate on the paper's detail, ChatGPT and finance

New EP of ROIS Podcast with special guest, Financial Professor from the University of Florida, Professor

@alejandroll10

!

Releasing on May 15th, Monday @ 8AM EST.

#GenerativeAI

#StockMarket

#ChatGPT

#AI

#Prediction

#Finance

@RoisInvestments

0

11

13

3

12

36

I really look forward to the 6th Future of Financial Information Conference, taking place on 27-28 May 2024 at Stockholm Business School. And you should too! 🌟

As session chair, I am thrilled to see two wonderful papers in my session:

What Drives Trading in Financial Markets?

0

1

35

Being a finance professor is the best job in the world by far

In finance:

- Good pay

- Good job market atm* (8/8 strong academic placements among our PhD students this year, though we are good and this year was unusually good even for us)

- Good outside options

* past performance is no guarantee of future returns etc

7

4

91

4

3

31

For anyone asking for a live version of the paper 😅

It's pretty cool to see academic ideas implemented this quickly!

We gave ChatGPT $50k of our money to see if it can beat hedgefunds

1500 people joined and now another $1 million+ is copying ChatGPT via Autopilot

So lets have some fun here

No clue how it'll do, but will be fun to do it with everyone

More details on "The ChatGPT Challenge"👇

135

185

1K

1

6

30

@AISafetyMemes

This can happen right now by googling the same information... I'm unsure how much extra risk LLMs add.

4

1

31

Does this count as 2.5 papers at NBER? 😂

0

1

30

You'll never have as much free time as you do now.

1

0

29

Happy to see it online!

#RFS

#Forthcoming

: Man versus Machine Learning: The Term Structure of Earnings Expectations and Conditional Biases

Jules H van Binsbergen

@Wharton

Xiao Han

@BayesBSchool

Alejandro Lopez-Lira

@alejandroll10

@UF

1

5

11

2

2

29

Our research has just been featured in the latest episode of

@excessreturnpod

I always enjoy talking about the foundations of asset pricing!

Does peer-reviewed theory help predict the

cross-section of stock returns?

with

@achenfinance

@TomZ_Econ

Those of us who use factors have been taught that they need a risk-based or behavioral explanation.

We have been taught to avoid data mining.

But what if both are wrong?

We are joined by

@achenfinance

and

@alejandroll10

whose new paper suggests exactly that.

4

13

51

0

4

27

💻💹Webinar on how to use ChatGPT in finance research!

Register:

🚨 Webinar alert 🚨

150+ registered participants within a few hours of the initial announcement can hardly be wrong - you will not want to miss the upcoming Future of Financial Information -

@FutFinInfo

#webinar

either!

Date: 21st June at 4pm CET (10am New York time)

1/🧵

1

2

10

2

9

28

@kareem_carr

R seems useless outside of academia no? I love R but I don't think students will keep using it at work

14

0

28

@cameron_pfiffer

@ChristophMolnar

book explains well why it is both statistics and machine learning depending on what you care about

3

2

25

Teaching and Research with ChatGPT Newsletter 🤖

I'll post about using ChatGPT in finance, research, and teaching.

How to use ChatGPT in class to teach coding. 🧑🏫

How (not) to generate research ideas using LLMs. 🧑💻

How (not) to use ChatGPT when writing. 🔖

Link ⬇️

1

6

25

💹New results in the space of open source financial LLMs:

💻We added Llama 2 to our Financial Natural Language Understanding and Prediction Evaluation Benchmark (

#FLARE

) Leaderboard

👨💻

#FinMA

looking well and we're currently improving it!

@JiminH_AI

0

3

24

My book will be produced as an audiobook!🎵

Generative AI and ChatGPT in Financial Forecasting

1

1

25

It's crazy the number of opportunities

#ChatGPT

opens in financial economics research. If you have an idea that needs text analysis or ChatGPT but don't know how to implement it let me know and we can collaborate!

#EconTwitter

2

1

25

When will finance journals jump in on this?

Econometrica seems to be experimenting with brief author responses to referee reports, prior to editor decisions. Seems cool!

14

45

359

0

0

23

Best slides on discussion of our paper at NBER 😂

0

0

22

⏯️New podcast recording with

@JeremyDSchwartz

in Behind the Markets!

We had a wonderful talk about the role of artificial intelligence in finance, including ChatGPT, factor models, and the state of asset pricing.

Podcast:

Live from

@Wharton

we have

@alejandroll10

talking his research on using Chat GPT for stock selection strategies and state of finance and general asset pricing research.

Plus we’re scooping CNBC this week with latest Siegel thoughts live from a cruise

0

6

26

4

6

22

My first collaboration with CS researchers! New open source model trained on financial tasks! With instructions and model weights available

📷 Excited to introduce PIXIU - the first open-source financial instruction dataset, benchmark, and fine-tuned LLMs! This is a big step forward for

#FinancialAI

. Check out our

#arXiv

paper () and GitHub repo ()!

#AI

#NLP

#FinTech

1

3

11

1

1

22

1/📣I recently had the pleasure of joining

@jjcarbonneau

and

@practicalquant

on their podcast

@excessreturnpod

.

We explore the effects of AI and LLMs on the world of finance! 🌐🚀

#AI

#Finance

#Investing

The Impact of ChatGPT on Investing

1

4

22

This is also my recommendation for finance PhDs

I found this amazing book named "Interpretable Machine Learning" by

@ChristophMolnar

while I was researching about explainability. It covers lots of core concepts from beginner to advanced. I highly suggest reading it.

0

2

22

0

2

20

My first paper in

#NeurIPS2023

! We produce open-source benchmarks and training data for LLMs in finance tasks, and even a fine tuned model!

🎉 "PIXIU: A Benchmark & LLM for Finance" is now accepted by

#NeurIPS2023

! Dive in:

🔗Paper/Datasets/Code:

Thanks to Qianqian Xie, Weiguang Han,

@alejandroll10

& team! 🙌

#FinancialNLP

#AI

#LLMs

#fintech

0

2

8

0

2

20

This is the first lesson of my undergrad class

Universities should consider putting together a single class on generative AI that covers the hot button issues: LLM basics, AI literacy, ethics issues, how to prompt & use AI, etc.

Otherwise a lot of this content is partially taught & is ad-hoc scattered across various classes.

31

89

586

1

0

20

Good news for anyone hoping for a natural experiment about AI! 😅

#EconTwitter

BREAKING: 🇮🇹 The ban was ordered by the Italian privacy regulator on Friday over alleged privacy violations. More updates to come...

3

29

38

3

1

18

Looking forward to presenting some cool new asset pricing results in the Theory-based Empirical Asset Pricing Research (TBEAR) Network!

With

@CarterDavisFin

1

1

20

We are happy to announce the launch of the FinNLP-AgentScen at IJCAI-2024, FinLLM, which includes three subtasks tailored to effectively and holistically address diverse financial challenges:

- Financial Text Classification: Designing LLMs to categorize financial texts as

3

2

20

@Stephsaguudefan

@veganhonk

@agraybee

It's literally the definition of 130... Two standard deviations above the mean in a normal distribution

0

0

18

@lukestein

You know there's extreme political polarization when waffle cones become part of the political identity

2

0

19

Can LLMs really help you outsmart the market? 🤔

I explore the potential, limitations & future outlook in my latest article - a taste of the in-depth insights in "The Predictive Edge," available for pre-order!

Book out on July 11!

Article and Book links on thread⬇️

1

1

19

@paulnovosad

But then you reject if not all requests are satisfied. If as a referee I think clustering is causing the issue I'll ask for a specific specifications, same for the data sample. If it breaks or authors don't do it then you reject the paper

1

0

19

My first post is out! Based on my class using ChatGPT

How to persuade students not to use ChatGPT for essays⚡️

Why the pretraining in ChatGPT can get students into serious academic problems‼️

Link ⬇️

1

0

19

@Simeon_Cps

If you limit the amount of computing power available, all the effort is going to go towards making training more efficient

2

0

19

Heading to the

#AFA

! ✈️

Check out tomorrow our paper documenting data mining is as good as the peer reviewed process in finding asset pricing anomalies!

You can get out-of-sample returns as large as the anomalies literature by just mining 29,000 accounting ratios for t-stats > 2.0 🤣

4

14

94

0

1

18

Testing academic ideas just became an order of magnitude easier with

#ChatGPT

If it's less costly (timewise) to write academic papers, will it result in better or worse average quality in peer reviewed journals?

#EconTwitter

This 🤯 is a very big 🤯

I have access to the new GPT Code Interpreter. I uploaded an XLS file, no context:

"Can you do visualizations & descriptive analyses to help me understand the data?

"Can you try regressions and look for patterns?"

"Can you run regression diagnostics?"

146

1K

6K

2

1

18

Just found out you can opt-out from your data being used to train ChatGPT

4

5

18

1

3

17

I always wondered why ETFs don't strictly dominate index mutual funds

🚨Job market paper🚨

Ever thought about the differences between ETFs and index mutual funds? Heard about ETFs' advantages, incl. tax efficiency (in the US) & intraday trading, and wondered whether ETFs will eventually replace mutual funds in the index segment? My JMP suggests no.

7

33

154

0

2

17

@paulnovosad

Growing up in Mexico top USA colleges didn't even cross my mind as a feasible outcome

1

0

16

I'm convinced consumption asset pricing models can rationalize the extremely high Sharpe ratios we observe in the cross-second of returns.

We just need to add more unobservable latent variables that affect consumption but do not materialize in-sample.

April 1st.

4

0

17

RF are still my favorite supervised ML technique. Great thread on why they perform so well.

Why do Random Forests perform so well off-the-shelf & appear essentially immune to overfitting?!?

I’ve found the text-book answer “it’s just variance reduction 🤷🏼♀️” to be a bit too unspecific, so in our new pre-print ,

@Jeffaresalan

& I investigate..🕵🏼♀️ 1/n

15

224

1K

0

0

17

This is a *lower bound* on GPT-4's predictive capacity.

Better prompts and current information will increase the performance.

See our paper for a case where it performs very well.

Can ChatGPT Forecast Stock Price Movements?

How good is GPT-4 at forecasting?

In this new paper (with

@Dr_Park_PhD

), we test this in a real-world forecasting tournament

@Metaculus

.

🔴 We find poor LLM performance compared to humans!

🔴 GPT-4 fails to outperform predicting 50% on every question!

6

37

124

1

1

16

@paulnovosad

But p-hacking means select specific results/data preparation no? You can just ask for a variety of other samples, specifications and assess the coefficients and statistical significance for each of the exercises you suggest.

2

0

16

Teachers casually using prompt injection to detect ChatGPT generated essays

0

0

16

Session info with

@SBryzgalova

chairing

Heading to the

#AFA

! ✈️

Check out tomorrow our paper documenting data mining is as good as the peer reviewed process in finding asset pricing anomalies!

0

1

18

0

1

15

I'm working on a post on how to obtain good research ideas using the insights from my PhD class (LLMs can help but not ChatGPT)

Some PhD students seem to think a good way to find research ideas is to read the conclusions paragraph of good papers, and do the things authors say are natural next steps for research

This is a terrible idea! Absolutely terrible! It is hard to do worse than this!

18

20

318

1

2

15

Interesting idea! In finance, we can see the tractability trap with the pervasiveness of CARA/CRRA utility models despite their fragile empirical foundations.

#WeekendRead

This recent working paper presents hypotheses on how tractability has shaped economic model:

@Undercoverhist

@CNRS

#EconTwitter

0

3

7

3

3

13

It's interesting, because machine learning cannot help with causality, but it can give you the best prediction

Unpopular opinion: Causality is **not relevant** in the majority of

#quantfinance

modeling applications! “Successful prediction does not require correct causal identification.”

Causal relationships are important if you want to **intervene** in a system. Quant traders are not

24

33

314

3

0

14

@_RodolfoOcampo

@OpenAI

Can you try to ask your advisors to use their research budget to cover it? Otherwise maybe a GoFundMe?

1

0

14

One of my favorite conferences! Be sure to apply or attend! A perfect place to learn the latest in

#BigData

,

#MachineLearning

, and

#AI

applied to finance research!

1

3

13

I will allow (and encourage!) the use of LLMs like ChatGPT in my classes (finance and ML) this semester.

I plan on starting two newsletters with the outcomes.

One for professors/PhDs on ChatGPT in teachings (and research) and one for students.

Thoughts?

Both newsletters!

43

Only research/teaching

13

4

0

13

@momin_rayhan

@mark_berlin2

works great for this, you get an email summary and can follow my authors, journals, keywords

1

1

12

Looking forward to the conference! It always features amazing papers and participants!

Next week, the

#FutFinInfo

Conf is coming to

@HECParis

, for investors to understand the changing nature of financial information and its consequences for market efficiency

#NLP

#MachineLearning

#bigdata

An occasion to reward the best

#PhD

paper!

Program:

1

10

18

0

2

13

I appreciate the nice comments!

Here's the link to the paper:

@alejandroll10

&

@NickRoussanov

's attempted murder of the APT is probably my favorite paper in the last several years. They find the more risk you hedge, the *better* your Sharpe ratio!

Highly recommend the NBER SI talk + Bryan Kelly's discussion

2

2

14

0

2

12

I mean, it took me a couple of tries but here:

A simple puzzle GPTs will NEVER solve:

As a good programmer, I like isolating issues in the simplest form. So, whenever you find yourself trying to explain why GPTs will never reach AGI - just show them this prompt. It is a braindead question that most children should be able to

350

416

4K

1

0

12