PDS

@TopadoDuran

Followers

7,697

Following

1,139

Media

57

Statuses

2,895

Modern Global Macro Investor. Former Head of Macro at Soros. ex - Element. QFR. GS. DB. Macroeconomics. Markets. Bayesian. Data. Opinions are my own.

Manhattan, NY

Joined October 2009

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

#ปิ่นภักดิ์EP10

• 832115 Tweets

TLP THE SECRET OF RING

• 820836 Tweets

凱旋門賞

• 131569 Tweets

HUNTER×HUNTER

• 104212 Tweets

Jets

• 96604 Tweets

Vikings

• 60742 Tweets

シンエンペラー

• 59250 Tweets

Lewandowski

• 58789 Tweets

Rodgers

• 55328 Tweets

宇宙戦艦ヤマト

• 51075 Tweets

中嶋監督

• 47729 Tweets

Brighton

• 36981 Tweets

ブルーストッキング

• 25707 Tweets

Saleh

• 20806 Tweets

Mertens

• 16830 Tweets

ハンターハンター

• 15839 Tweets

#GSvALN

• 15027 Tweets

アヴァンチュール

• 14554 Tweets

Ange

• 14373 Tweets

Jefferson

• 10869 Tweets

Pinned Tweet

Weak-ish report from many angles, yet flows to unemployment remain subdued and permanent jobs losers are not gaining any traction. (Note to the strategy from last night dinner - PJL is the feature of every employment cycle and what makes the current one so different from the 2000

2

9

42

@OversightDems

Act on it.

@SpeakerPelosi

@SenSchumer

. Republicans are obstructing Democratic process and Dem leadership doing nothing

59

100

843

The Fixed Income macro crowd spent all 2023 between 2 narratives. A) Higher for longer amid sticky inflation and supply imbalances and B) Imminent recession.

US rates are ending the year on a strong note proving wrong the former crowd and giving a Xmas gift to the later crowd.

13

22

222

Macro playbook- we are transitioning from Goldilocks to Passive tightening where Fed is hamstrung on responding to economic weakness. Higher odds of Goldilocks regime supported the market, mainly a function of the powerful combo of still robust economic data and disinflation 1/3

Today feels like the first in a long time where bad economic news was bad for markets - could be an important turn, at last.

49

84

962

3

31

207

When thinking about US consumer demand, most Wall Street participants attach way too much importance to income and not enough to savings and taxes.

Modern consumption theory has evolved from the Keynesian static consumption function because ignores any positive effect of past

17

34

158

Goldilocks regime is fragile. Needs perfect sequencing -> fast disinflation, econ holding and Fed pausing. If econ weakens faster than the Fed is ready to pivot (amid still elevated but falling inflation) - which is now the case - then from Goldilocks 2/3

2

9

150

We transition towards hard landing. Fed still hiking and econ data showing clear and convincing signs of early recession, that’s is when u get maximum FCI pressure. Add to this mix, liquidity sucking from replenish the TGA through bill issuance . Toxic mix for risk

11

6

128

For this week -> What US econ data release will be most informative to your view of the US economy?

@federalreserve

#useconomy

S&P US PMIs

118

GDP 4Q22

102

Personal Consumption

171

Durable Goods Order

75

7

14

104

OER and Rent inflation NSA confirmed the major step down of March. It also confirmes the Detroit anomaly was just that.

This is highly relevant as the seasonal adjustments are clouding the trend. Now that high seasonal are behind, seasonally adjusted data will trend lower for

7

23

111

3 charts u need to focus to think about the US labor market with a forward looking lens

1. Narrowness of NFP gains continues to increase. 78% of March NFP gains comes from the 3 “hungry for jobs” sectors (Education and Healthcare, Leisure and Hospitality and Government). The

2

23

93

Chair Powell laid out 3 policy path scenarios - prolonged pause, goldilocks cuts and labor market weakness cuts.

So instead of telling us the policy rate is likely at its peak, he laid out 3 scenarios that imply the policy rate is likely at its peak. A great way to focus

3

8

71

There are a ton of so called Macro experts out there with an opinion on the upcoming

@federalreserve

dot plot. Almost none of these are surgically formed

Heres is a surgical approach to it

6 members wrote down 3 2024 dots in Dec SEP. I think these members are: Daly, Barr,

10

10

63

A gentle reminder to the bond bear crowd that UST bonds are safe assets. Many on that crowd completely confuses cyclical forces with structural forces, hence misleading a generation of retail investors looking for macro expertise. Just remember, the genuine macro experts are

6

7

63

2 quick facts about NFP forecasters:

1- They love to cluster around the median

2- Independent thinkers, those that deviate the most from the median, tend to have the largest misses

For tomorrow, and narrowing the sample to the last 3 prints, 2 of the best forecasters are above

4

11

58

Since we have so many macro experts who form conclusions from a headline number, let me add some granularity and add a few dimensions to this loosey goosey hot wages narrative.

First, 30 bps of the private industry workers +1.1% QoQ were contributed by Professional and business

3

5

58

A relevant identity for 24

r* = rho + a * g - ERP

r* is not really pinned down independently of risk-appetite, AI beliefs, etc. Most macro models of r* ignore these and focus on rho + a* g, but if your view on SPX is based on r*, then u need a risk centric framework

So If US

4

5

53

Some less followed but key US labor market stats

1- The strength of the labor market is evident in the elevated pace laid-off workers are finding new jobs. The flow from unemployed to employed is at levels consistent w/booming labor markets. 1 reason why claims are not ⬆️

2

7

54

Equity prices up = Bond yields up = FCI neutral market adjustments

Market continues to anchor on:

r* = rho + a * g - ERP

Lower ERP = Higher r*

To the benefit of the Fed this anchoring mechanism is keeping FCI constant. Bonds are held hostage of the AI led equity rally

2

4

51

Hi recessionistas - formerly in the higher for longer and sticky inflation camp - did anyone checked Initial Claims NSA today?

189k….

16

2

49

One of the recently loosely formed macro narratives is that given the stock market rally and its wealth creation, consumer spending will be “perennially” strong.

I wrote about wealth effect on consumer spending to refute the idea that the consumer was about to fall into a

When thinking about US consumer demand, most Wall Street participants attach way too much importance to income and not enough to savings and taxes.

Modern consumption theory has evolved from the Keynesian static consumption function because ignores any positive effect of past

17

34

158

9

7

49

Northeast OER NSA MoM prevented Core CPI to be closer to 10 bps

Very likely we see a reversal of this jump, which keeps the OER NSA MoM downtrend in great shape

The “New York” anomaly contributed 12 bps more to OER NSA MoM National Average !!!

@NickTimiraos

@jasonfurman

3

15

47

@GOPLeader

@HouseGOP

Take note: shutdown will continue for months, March 2 comes Dems will hold GOP hostage of the debt ceiling and wont support raising spending caps later on the year. Trump and GOP will be remember for taken a strong economy into a mediocre and indebted one

#GOP

not thinking

6

5

38

Investors and Analyst spent H1-23 trying to be long Chinese assets amid hope that Xi Jinping will decide to stimulate the economy. This is what I called the “hope” trade. Now that same group of investors and analyst is on the camp that China economy is lost or that Chinese asset

At a time when everyone had given up on the Chinese economy picking up, the data looks to be improving.

Good scan of the data below showing improvement. With the continued efforts stimulate, seems the baseline expectation of ‘no chance’ of a pickup is too gloomy.

14

12

112

5

3

43

The most relevant message “The Fed put is ATM”

All the rest is mental gymnastics

6

10

42

Fed Watcher 3 months ago. “Fed has to continue to hike maybe beyond 6% because demand is too strong and that will drive inflation higher…”

PDS: Inflation will surprise lower and fall faster many and Fed anticipated, because inflation was mainly a large supply shock phenomenon

6

6

41

CPI revisions will go a long way for

@federalreserve

to gain greater confidence - this was a sticking point for them and Powell response on the presser suggested so.

We think market consensus was expecting a +0.2% bump in Q4 3m SAAR number and we got about +1.3 bps of revision.

2

6

41

Here is what drove the Fed pivot.

@federalreserve

started the year too bearish on growth - with Dec 22 SEP forecast +0.5% for 2023. The most bullish in that SEP forecasted 1.0-1.1% for 2023 GDP. The forecast was just updated to 2.6%

In the same SEP they had revised Core PCE

4

6

38

Puzzles me that many investors are embracing a weak USD amid reflationary forces emanating from China reopening and a warm European weather. In 2017, the street embraced global reflation and the USD depreciated ~ -11%. This in a context of ~ 4.1% global growth 1/2

2

7

39

The relationship between r* and ERP is currently at the center of markets dynamics.

In a positive growth shock environment SPX drifts higher with EPS growth while bond yields sell off, as rates reset to a higher r* regime. To the benefit of the

@federalreserve

, this dynamic is

A relevant identity for 24

r* = rho + a * g - ERP

r* is not really pinned down independently of risk-appetite, AI beliefs, etc. Most macro models of r* ignore these and focus on rho + a* g, but if your view on SPX is based on r*, then u need a risk centric framework

So If US

4

5

53

2

5

36

Here is the only stat Powell should be looking at for tomorrow FOMC

@federalreserve

@NickTimiraos

Heading into March FOMC -> 2 banks in receivership. 6 other banks in the list with equity drawdowns larger than -30% since SVB

Heading into May FOMC -> 3 banks in receivership. 73

6

7

35

Welcome back 1.5% GDP regime

Most relevant data point today is retail control and revisions to the service line item of the retail trade report

How ironic is it that when GDP consensus are at the highs of the cycle, consumption is finally softening? The GDP forecasters started

4

2

34

Global growth is currently tracking below trend 0.9% while the USD is roughly -10% off its 2022 peak. China will need to deliver 6%+ growth and a growth impulse pass through of 0.5 (highly unlikely) for the world to reflate like in 2017. The USD seems a good bet to my 👀 2/2

3

2

34

Detroit Shelter CPI was responsible for 1.8 bps of March inflation or about 30% of the core inflation miss 💀

What's the stupidest finance-related thing you saw this week?

76

0

31

2

2

34

Bumpy road.. perspective is needed or a few years living in an EM country. DM folks are not familiar with price propagation in normal times so they confuse bumpy road with inflation broadening

@DanielSLoeb1

another one for

#UncleLarry

Is inflation reaccelerating, getting stuck or are we on a bumpy path down. The diffusion index of % of prices rising vs falling favors the latter--after soaring to >90 in 2022 it fell to 21.6 in Feb despite upside surprises. This was b/w 90-100 for years in the 70s...

9

26

140

3

4

32

Remeber how many pundits (in January) pointed to NFIB plans to raise worker compensation to tell a story of accelerating wages? Well…

3

4

31

Anyone out there thinking the labor market still tight is stuck in the past and not paying attention to the meaningful improvement of supply and now the now obvious proxy of this dynamic -> decelerating wages

6

3

33

Everyone looking for a grand resolution from authorities. Dodd Frank makes it very hard to use tax payer $$ for bail outs. But ultimately, why should the government be ring fencing banks when the solution is for them to raise their deposit rates? SIVB abused the use of HTM

⚠️ U.S. SENATOR MENENDEZ: NOT READY TO OFFER SVB A BAILOUT 'BY ANY STRETCH OF THE IMAGINATION'

5

6

31

3

4

32

@WhiteHouse

@realDonaldTrump

@SecretarySonny

A great day / month for South American farmers. Keep giving away your market share

@ASA_Soybeans

😂

0

0

20

There is a “dance” between markets and the

@federalreserve

as the Fed leans on markets to do some of their work - at times. My colleague and macroeconomic mentor Ricardo Caballero outlines the mechanics of this dance in his 2020 paper “Monetary Policy with Opinionated Markets”

Rate markets are trading super-erratically with respect to whether a big cutting cycle will take place between mid 2024 and mid 2025

Jan : 130bp cuts priced

Apr: only 60bp priced (at peak)

Now: 90bp

No anchor…

3

0

34

1

3

31

@CuomoPrimeTime

This kid wasn’t on top of his game. He needs to be more precise as to what regulatory requirements he is complying by restricting trading activities

1

1

29

2. Permanent jobs losers is showing its ugly head. Historically (ex-Covid) permanent jobs losers leads U3.

Can one of the 250 PHDs at the

@federalreserve

pick this up??

@NickTimiraos

2

7

29

What surprise me the most from a large number of equity investors is the idea that stocks can look through further policy tightening and Mike Wilson’s negative operating leverage thesis.

But the economy doesn’t transition from Boom to Boom without cost.

So expect equity

Friday’s PCE figures, with both core and headline inflation running at 7 percent last month and big upward revisions for the 4th quarter, are very troubling.

80

226

1K

0

3

28

ECB tomorrow may trigger a large risk off event if they hike 50 bps.

The most damaging environment for long duration asset is when u are in the intersection of “heading into a recession” and “CBs tightening” this dynamic will make 2022 look like a 🐶

This is now at critical levels and IMHO a major market moving event.

🇨🇭 CS CDS Update

6M 1400/1600

1Y 950/1150 (+200)

2Y 800/1000

3Y 700/900

4Y 600/800

5Y 600/700 (+100)

7Y 550/750

10Y 500/700

44

80

483

3

3

28

3. We argued in the past that the bedrock of the strength of the labor market was the ability of unemployed to find a job if they wanted one. Looking at the flows of the labor market revealed broad robustness and provided an explanation of why initial jobless claims remained

2

3

27

Fixed income investors reacted to today’s JOLTS data in a mildly hawkish way. SFRM4 dropped from 95.31 to a low of 95.23 before reversing some of the losses.

While I think JOLTS openings doesn’t move the

@federalreserve

policy needle - as it did in the spring of 22 - as Waller

0

4

27

@MarioNawfal

That France and Germany were leading Russia/Ukraine dialog. Now is the US. Name a conflict where the US has led and has not result in a total disaster for basically all parities..

2

0

24

The momentum crash likely amplifying bid in stocks. On this particular MoMo construction, the short leg has 22% representation in NDX. Likely the short momentum factor has the largest representation in a long while given tech/software heavy concentration

@CliffordAsness

thoughts?

3

5

26

Underneath the surface there is a meaningful cooling of the US labor market🧵

Over the past 6 month NFP gains have narrowed mainly to 3 sectors (Leisure and Hospitality + Education and Healthcare + Gov). These contributed on average 68% of monthly NFP gains (last month 72%) -

1

6

27

Most important message from today’s FOMC ->

Powell acknowledged higher growth - near term - is likely driven by supply side factors. So don’t expect the Fed to hike again on the back of growth alone.

Fed “vigilantes” need a sequence of events: data persistently above near term

3

3

24

@biancoresearch

@biancoresearch

focusing on the right side of the balance sheet while most of the analyst crowd spinning around stories to show the deposit outflow is not as bad as it was the week of the run

Small banks Loans and Leases back to back weekly drop only compares to March 2007,

1

1

24

Market participants fear the March FOMC SEP reveals higher Core PCE forecast for 2024. This is sensible given the market tends to overreact to recent data and January and February Core PCE were high.

Extrapolating from these two months for the rest of the year is premature given

9

4

23

The rebalancing process means lower share of goods spending via prices (more deflation) and quantities. It also means service inflation can run a little hotter than normal to allow the share of spending in services to revert to pre-pandemic. Labor supply allows this process to

The step down in consumer spending in Q1 was led by a decline in goods spending as consumers appear to be reverting back to a pre pandemic budget share at a faster pace

3

16

78

3

3

23

To square the mess..

They discussed cuts in the context of SEP, not as a short term policy action. Williams was sent to clarified this. But he didn’t play down the dots - so cuts remain the most likely next move.

Data will determine the timing and magnitude of calibration

@federalreserve

Powell Dec 1: it’s premature to talk about easing

Powell Dec 13: we’re talking about the timing of easing

Williams Dec 15: we aren’t really talking about it

2

1

15

3

3

23

Japan is one place where China reopening could be inflationary via tourism pressuring service inflation amid a tight labor market. Current inflationary dynamics are driven by food + electricity may prove to be a platform from where 2% inflation -> sustainable. Compounding nGDP is

0

6

20

2- The way the labor market is absorbing new entrants suggest JOLTS is not far off. An obvious consequence is with immigration ⬆️, leisure and hospitality will continue to print sizable monthly gains supporting NFP

@jasonfurman

@jc_econ

@federalreserve

1

1

20

Not a big fan of analogies based on historical price action patterns, yet at times we can infer changes in the market Zeitgeist.

SPX modern era doesn’t have a lot of negative monthly returns in December (8 since 1990), so 2022 was unique in this regard 1/2

2

5

19

@jdawsey1

The Fed is not the problem. The problem is debt induced fiscal boost when economy is tight, poorly managed and wrong strategy of foreign policy (aka Trade War) and a bunch of advisors clueless about what drives markets narrative /1

2

2

13

Greenspan July 1995 FOMC transcript. Fed starts “soft-landing” calibration cuts:

“I have concluded that, since the risks are beginning to ease slightly, there is no urgency here; but I do think we should move because I find it increasingly difficult to argue in favor of staying

0

1

18

Agreed.

Narratives on the back of data points won’t be sticky as marginal information won’t be enough to change stickier macro trends. Data dependency is now a “sequential” game rather than this or that data point

A bit surprised that the narrative is about the "hotter" CPI. Yes, 0.3% core, 0.4% supercore, 0.4% median, & 0.35% trimmed mean. All a bit firmer than you'd like to see. But, we are on track for a modest core PCE print. We'll know more tmrw, but Dec is looking soft.

13

27

108

1

4

18

There is an RKO effect where easier FCI leads to higher nominal growth and to GDP reversion to trend.

@federalreserve

will ignores FCI easing until output gap looks to be turning positive. The goldilocks regime will get knocked at that boundary. Sequence and pace matters

2

1

16

@OversightDems

@RepCummings

@RepAdamSchiff

@RepEliotEngel

@SecPompeo

plan was to run for the senate.. go after his New York fund raisers - cut him off

0

3

14

@NickTimiraos

Nick. 75 bps hikes will be portrayed as the Fed is panicking and slamming on the breaks of the economy. S&P 500 will be at 3100 by the end of the summer and CDXIG at 150. And inflation will still be high because energy and food prices will remain elevated. Fed is creating a mess

1

1

17

@dampedspring

6 month ago the Zeitgeist was about sticky inflation- data has challenged that prior and investors gave up on it and then some…

Narrative will change as data keeps tracking solidly above trend

4

0

16

% of SX5E constituents with RSI > 70%

Xmas came early in Europe. Time to ……..

#notfinancialadvice

#degen

5

6

17

Bom Dia. Channeling legendary

@concodanomics

Say it back

Labor market is balanced and cooling towards weak

Chair powell added the characterization of “relatively” in front of tight. Next is balanced (more like a little weaker than 2018-2019) specially on hiring flows

2

3

16

All Powell meant to say “we will have greater confidence once we get the

@BLS_gov

annual revision, so we confirm with the same degree of confidence we have today, that inflation is heading towards 2%”

This question touch a nerve

@federalreserve

8

1

14

Market motivated reasoning pushes the market analysts to look for a fire where there is no smoke. Haven’t seen in a while a market that is deviating from the Fed “tea leafs” for the purpose of confirming the higher for longer bias. Low bar for a dovish surprise…

This anticipation doesn't square much (at all?) with recent Fed communications:

1) The vice chair of the FOMC recently made quite clear he doesn't think r* has shifted up.

Williams, 5/19/23: "There's no evidence that the era of very low natural rates of interest has ended..."

12

67

294

1

3

14

Labor supply ⬆️⬆️

More goods news on immigration! I am loving this careful & timely work from

@courtelizashup

. So far in 2023 the flow of work visas granted to immigrants and non immigrants is running 20% above 2022 & 35% above 2019, working through backlogs, making up for lost time 🔥

8

23

104

2

2

14

@BobEUnlimited

How about banks start to raise their deposits rates asap?

SIVB was pretty unique by abusing of the HTM account. Why are we assuming that many more banks will fail when SIVB was an outlier? Do u think other regional banks don’t have the capacity to absorb a run for a few days?

4

0

13

@dampedspring

Sticky Growth 2% inflation 2% regime. Both pieces are falling in place. Converging from higher growth to trend like growth and inflation converging from 2.5-3.0% regime to 2.-2.5%

Caveat.. some of this is priced and we are likely to get a real pullback before marching higher

1

1

13

Equity focused folks asked me whether BOJ market operations were offsetting the liquidity withdrawal effects of Fed QT.

Interesting question, but an incorrect assessment of how BOJ operations are affecting Japan’s monetary base. SLF operations are off balance sheet and while 1/2

2

2

12

@jdawsey1

They blame the Fed, Volcker Rule or even global growth slowdown. The issue is simpler, in a context of tight capacity and high animal spirits due to tax reform, they decided to initiate a Trade War, which attacks the heart of what makes US companies profitable /2

0

1

9

Just as the

@federalreserve

acknowledged the benefits of immigration on labor supply, LFP of foreign born has already reverted to the mean

1

2

12

02 & 22 have a lot of similarities in terms of the market Zeitgeist - SPX in a bear market, beaten up for most of the year until strong reversals in Oct/Nov and sell off in Dec. It caught my eye how the rest of the quarter developed for 2003 -> Not investment advice

0

1

12

POWELL: Well, I would say it this way. The economy's strong. The labor market's strong. Inflation's coming down. There's no reason why that can't continue. We're gonna try to use our tools to give the economy -- to continue to improve as inflation comes down. We'll give it every

1

1

12

@BillAckman

@SBF_FTX

Doesn’t take too much to know here this guy is a crook. Stop out quick on this on Bill

0

0

12

@NickTimiraos

Clarida who at a private dinner table said Fed couldn’t go fast in raising rates when rates were still 1% and now prefers to hike into a regional banking crisis to pretend everything is well…. ChatGPT could add more value

2

0

11

Let’s say FDIC increases the non-interest bearing guarantee threshold from $250k to $5mm as the insightful

@BobEUnlimited

proposes. FDIC argues the deposit insurance funds consiste of premiums already paid by insured banks and interest earnings on its investment portfolio of US

3

0

11

@GOPLeader

@HouseGOP

I don’t care who made the strong economy. I care about the future economy - the strong economy of today was supported by a trillion plus hole in the deficit.. in the future, if you slowdown with these typs of deficits, it will feel worse.. so I care about forward!!!

1

0

9

@DsrPrivate

I think is rather simple analysis

Last QRA, term premium was expanding in a vicious way with markets extrapolating a number of narratives with questionable persistence resulting in higher yields and rapidly tighter FCI.

If Jan QRA were today is the opposite in term premia

0

0

11

So if the sectors that are hiring at rapid pace and keeping NFP elevated are not exhibiting wage pressure, why are we still talking about a very tight labor market? One has to wonder the

@federalreserve

with its armies of PhD can handle a nuance analysis beyond the headline NFP

1

2

9

@BobEUnlimited

@ErikHane4

Correct- are they profitable thou? What’s the average funding cost of regionals? Why haven’t regionals raise deposit betas above 60%?

Not a credit crisis - rather the biz model is being challenged with current monetary policy mix..

2

1

10

outright purchase continue at a briskly pace, covid loans retirement have more than offset these (hence monetary base contraction)

From here we are likely going to see further expansion of the monetary base as long as BOJ keeps buying JGBs💀 2/2

3

1

9

@DsrPrivate

Behavioral crowding is the easiest to bet against and produces the largest alpha for the contrarian.

When the argument is no catalyst can derail a year end chase, is worth to examine the catalyst pipeline, because while year end chase tend to happen often, I argue it already

3

0

9

But as labor supply recovers, the labor market is absorbing new entrants incredibly well, allowing wages to slowdown. Important -> the sectors that are leading job gains, are exhibiting a solid slowdown in wage growth. On the other hand, the sectors where we are seeing layoffs

2

4

9

@DsrPrivate

What I love about the game is there is always another day/month/quarter as long as one is humble to acknowledge what went wrong (and right), reset and do it all over again

One of the most valuable lessons I carry with me that I learn from George Soros, was to be humble

0

0

9

@boazweinstein

Down less than -2%. The real test is when European credit and US regionals open….

The fact the bonds are flattish is telling to me. No major unwind of Fed easing “premia”

1

0

9

ChatGPT3.5 to the Low U3 is a problem for the Fed crowd…

“A vertical labor supply curve implies that changes in the unemployment rate have no effect on the wage rate, as workers are not willing to adjust their labor supply in response to changes in wages. This means that there

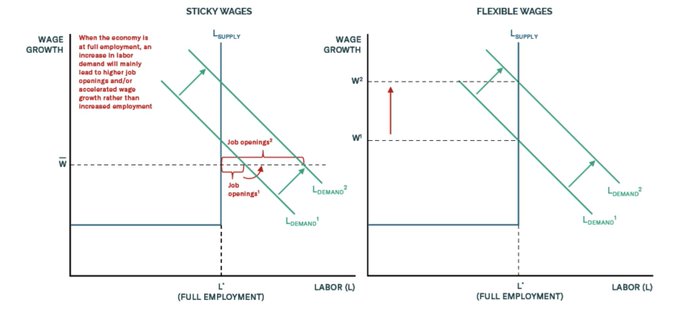

Confused about why job openings and wage growth have been falling, and yet employment has managed to hold up? Don’t be. This is exactly what you would expect if the labor supply curve were vertical.

1

24

94

0

3

9

@kjtc1979

@OversightDems

@SpeakerPelosi

@SenSchumer

That’s sensible, however the longer they sit tight the more the idea of an illegitimate election percolate across society. By now Biden will start his presidency with half of this country disapproving him just because the precedent we are letting Republicans establish

2

0

8

@rev_cap

2020 and 2021 distorted housing migration flows (when people move and where people move- because of the lockdowns and abnormal migrations to other states). The X13 ARIMA model does poorly with change of patterns, since it relies on stable seasonal patterns. The result are

0

0

8

@dampedspring

Not how the curve is trading but let’s see this week with 3s, 10s and 30s. What u argue should reflect in bear stepping action, which not what is happening (for now)

3

0

8

@dampedspring

@EconstratPB

@DannyDayan5

@Econ_Parker

@super_macro

@TheWineSwine

@brandonjcarl

@Johncomiskey77

@DanielSimonyi

@BobEUnlimited

@SteveMiran

Thanks for including me on the list Andy!! Looking forward to keep brainstorming the macro puzzle together

0

0

8