Anna Wong

@AnnaEconomist

Followers

30,132

Following

297

Media

217

Statuses

984

Chief US Economist, Bloomberg LP @economics . Former Fed/CEA/US Treasury, @uchi_economics @UCberkeley . All opinions are my own.

Joined May 2022

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Jack Smith

• 488762 Tweets

FEMA

• 480552 Tweets

Messi

• 184316 Tweets

SURPRISE FROM BECKY

• 154939 Tweets

Kalafina

• 114432 Tweets

Padres

• 83250 Tweets

Inter Miami

• 49378 Tweets

#AgathaAllAlong

• 42554 Tweets

GOLD RUSH

• 40599 Tweets

Brewers

• 33884 Tweets

Braves

• 33070 Tweets

#नवरात्रि

• 31958 Tweets

ROADRIDER X LINEMAN

• 31447 Tweets

学園アイドルマスター

• 30415 Tweets

プロデューサー

• 28621 Tweets

Sant Shri Asharamji Bapu

• 27488 Tweets

#Navratri2024

• 24623 Tweets

Shakti Upasana

• 24621 Tweets

BABYBOSS YINYIN DAY

• 24398 Tweets

梶浦さん

• 23910 Tweets

Maa Durga

• 23722 Tweets

#今年も新作スイーツラテ飲みたーーーーい

• 23313 Tweets

岡田監督

• 23088 Tweets

#もうすぐ三角チョコパイの季節

• 20683 Tweets

Saint Dr MSG Insan

• 20074 Tweets

ميسي

• 18837 Tweets

渋沢栄一

• 18694 Tweets

マナー講師

• 18671 Tweets

マナー違反

• 16690 Tweets

藤川球児

• 13710 Tweets

梶浦由記

• 11865 Tweets

शक्ति उपासना

• 11009 Tweets

This chart is pretty striking. Shows the share of new 90 day delinquencies citing unemployment for reason of delinquency of FHA single family loan.

H/t gopal sharath

Source:

43

298

1K

Lacy Hunt mentioned the “long tentacles” of payrolls revisions on other upstream economic indicators.

Some of them I identified are: personal income (lower), which also means saving rate (lower), GDI (lower). Ultimately, GDP (lower).

There is this myth that GDI always get

39

169

983

For gloom and doom commentary, look no further than the comments section of the Dallas Fed Services Activity:

"As a search and staffing firm in the business of hiring not only in North Texas but across Texas and the U.S., we have felt like we are in a recession now for months.

41

200

759

This article is the most potentially bearish thing I read this weekend ( and have been watching this issue for awhile).

Recall Q2 GDP surge due to a curiously large positive contribution to inventory. Which begs the question: are firms preparing for a surge in consumption?

61

130

759

Recall the October beige book is what did it for Powell for him to pivot last December. This beige book is even worse than that one. I think Powell is going to strongly push for a 50 bps now.

42

112

735

Construction payrolls should cool, possibly sharply, about…imminently. Our leading indicator leads by 7 months. It is about that time.

@TheTerminal

Our latest:

14

142

716

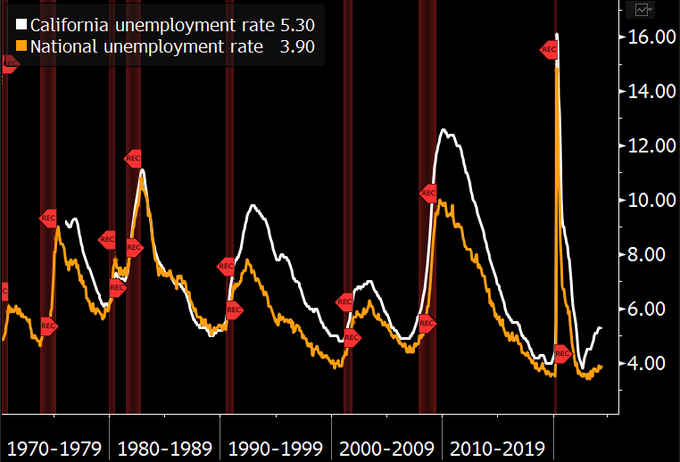

Since mid-1970s, all national recessions involve California. Or put it another way, the conditional probability of the national unemployment rate spiking given what California looks like right now is quite high.

45

151

696

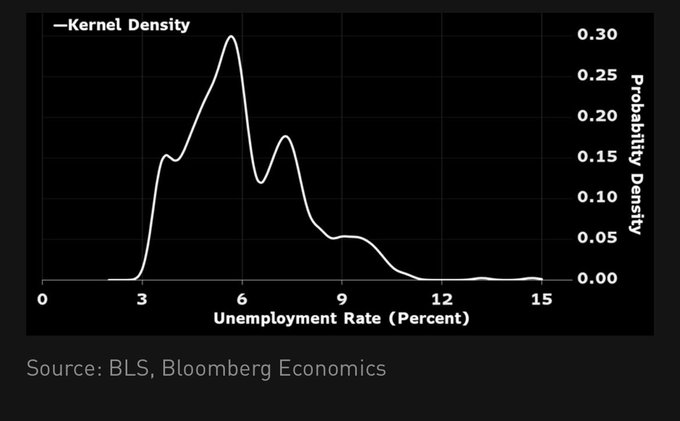

Our explanation for why soft landing confidence is misplaced: 1) the process governing unemployment (u) is nonlinear, its distribution is multimodal with long right tail. Linear forecasting models on past labor values would tend not to predict sharp upswings. (1/2)

@asokol_econ

Almost every hard landing looks at first like a soft landing

What's standing in the way of a soft landing now:

-The Fed staying too high for too long

-A too-hot economy

-A rise in oil prices

-A financial market rupture

"Planes land. Economies don't."

131

504

2K

11

124

585

I thought markets overreacted to JOLTS today but underreacted to Beige book.

In Powell’s words, what he thinks of Beige book (and also GDP):

“I spent most of my life in the private sector looking at companies-individual companies individual management teams and then building

15

94

558

Listening closely to Powell, my take is that he is already on board the 50 bps boat given the current data. It is now a matter of: can he convince the other FOMC members?

41

84

537

This is what happened to GDP q1 2001 print from first print to now. The recession began March 2001.

If the point is to get at the ground truth, I would downweigh things that get revised so drastically.

24

84

521

A short thread about a curious observation from unemployment forecasts ahead of tomorrow’s “make or break” jobs report.

Of the 69 submissions to Bloomberg survey for August’s unemployment forecast, the overwhelming majority (72%) expect it to fall from July’s 4.3%.

The realized

24

78

488

So the BLS prelim benchmark revision is -818k (in line with our 800k forecast). But the 1Q QCEW county data implies a bigger revision of -958k.

To put this in context, the typical revision is 0.1% of payrolls…the past year was 0.5%, 5x as large.

18

88

471

Powell mentioned he will be mentally adjusting down the payrolls number because of revisions. That adjustment should be about 91k per month, we estimate.

21

55

429

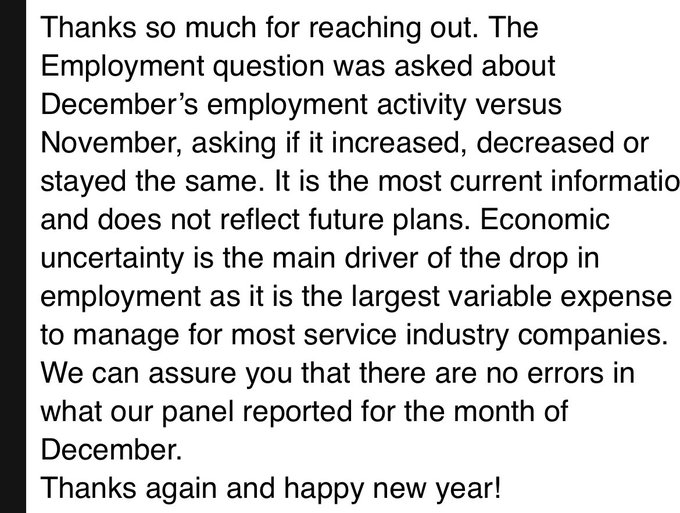

The ISM employment plummet was so sharp that I emailed the ISM folks to ensure they check if there is an error. This is their reply. So this really begs the question of why nonfarm payroll increased by that much.

41

91

407

Hot core CPI stole the thunder, but the real signal is with NFIB today.

16

95

409

Unemployment flows...up 21% in July year on year. Say what you will about this.

26

69

405

Measurement issues of nonfarm payroll should rise onto the top of Fed's policy work agenda.

For this May's nonfarm, we took a different approach to forecasting nonfarm payrolls, by forecasting both the "false" number, and the "true number" (the latter guided our unemployment

16

64

404

Underwhelming holiday retail sales was one of the first piece of data to alert certain Fed officials of a recession back in 2007/2008…the holiday season’s not over yet, but so far not looking good. Mastercard forecasts 3.7% y/y for the season, so far 2.5% y/y for Black Friday.

40

63

391

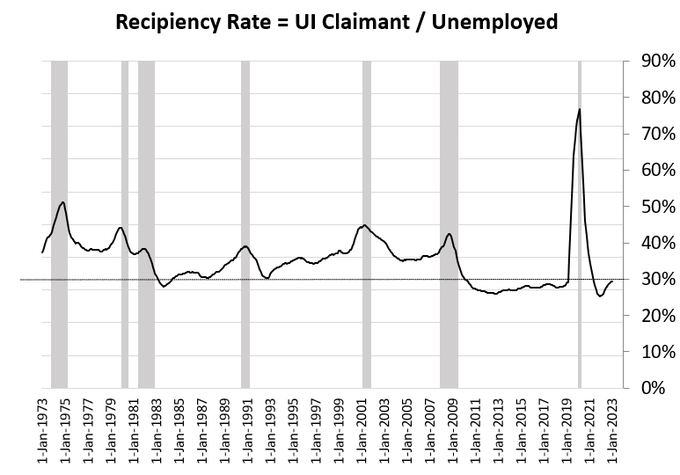

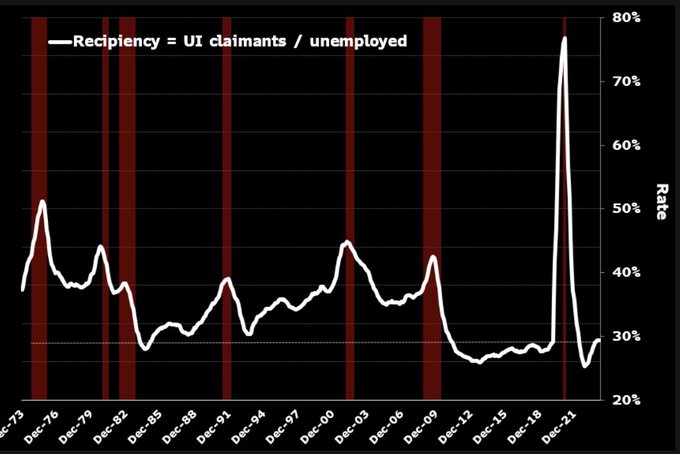

Only 25% of the unemployed is filing for unemployment benefits in July. That has further dropped from 31% in the beginning of the year —and this is while unemployment rate is rising. In comparison, the recipient rate was >40% pre-1990 and 2001 recessions. In this aspect, this

30

87

396

I agree with Julia that this Beige book is the most downbeat one in ages. For example, it reads even worse than July 2008’s.

From July 2008:

Reports from the twelve Federal Reserve Districts suggest that the pace of economic activity slowed somewhat since the last report. Five

Oof. Today's Beige Book is the most downbeat I've read in ages, especially the sections about hiring. Take a quick tour through some hiring-related quotes. They point towards a slowing, slackening labor market, not one that is stabilizing at pre-pandemic levels.

15

150

815

8

83

396

I’ve been ranked since I was in 1st grade (in the Asia system), more often coming up 1st from last, rather than 1st from top, as in my mid adulthood.

28

23

392

In fact, the recession from 1974-75 —the worst one at the time post WWII, and the one that sealed Arthur Burns’ notoriety — can dispel the notion that an unemployment driven by labor force expansion and temp layoffs can be dismissed as benign. Even though there are obvious

17

75

389

Jobless claims are very low, whatever seasonal factors one uses. Our latest on

@theterminal

assesses what the low level means. Spoiler: less unemployed people are applying for claims, meaning that the low level doesn't mean it what it used to mean. (1/4)

18

81

370

Just out today, June consumer credit. Here is how revolving look. Does it look like it is “normalizing”?

35

70

362

Was at NABE conference to listen to Kugler’s speech (good one, shows sensitivity to data nuances). Key take away: she said she would support “earlier” cuts only if unemployment rate increase is driven by layoffs.

So sounds like the Fed is not feeling urgency because of the

18

88

363

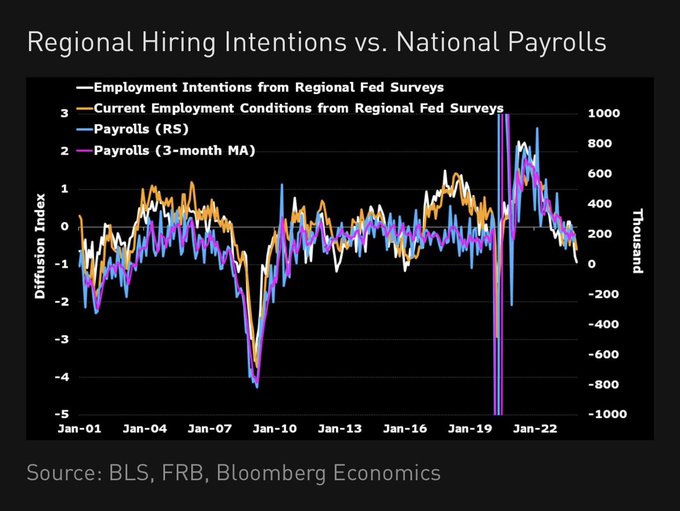

ISM employment plunge vs NFP blowout — which one will the Fed believe? Here is an employment intentions diffusion index we constructed from regional Fed surveys: it shows a similar steep drop as ISM.

17

74

348

It’s been tough being a bear, but we have forecasted unemployment to rise to 4.3% in Q3 and 4.5% by end-2024 since early this year. But even I am surprised by how quickly everyone is abandoning the previous narrative.

Our midyear note here.

14

42

355

To elaborate on former BLS Commissioner Beach’s explanation, here is what he meant in picture:

Net establishment counts changes is 51% lower compared to a year ago.

And yet the monthly nonfarm payrolls are using very very similar birth and death jobs forecasts as in 2023 so far

8

84

355

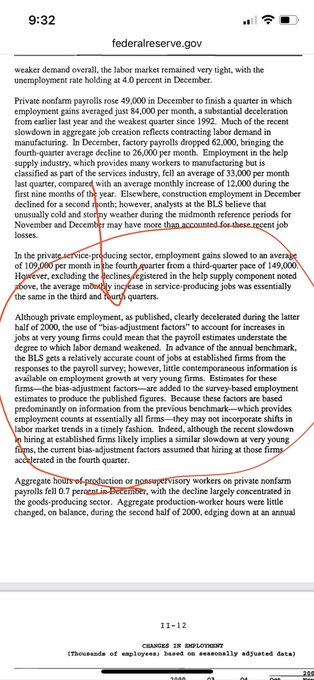

So 42% of the 3.1 million payroll gains in 2023 is due to BLS birth-death model. Here is Fed’s staff explanation back in Jan 2001 in the Greenbook on why the adjustment may overestimate job gains and “may not incorporate shifts in labor market trends in a timely fashion.”

13

79

339

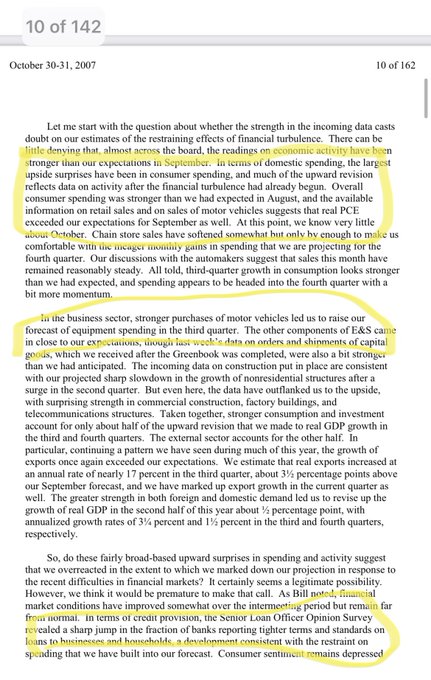

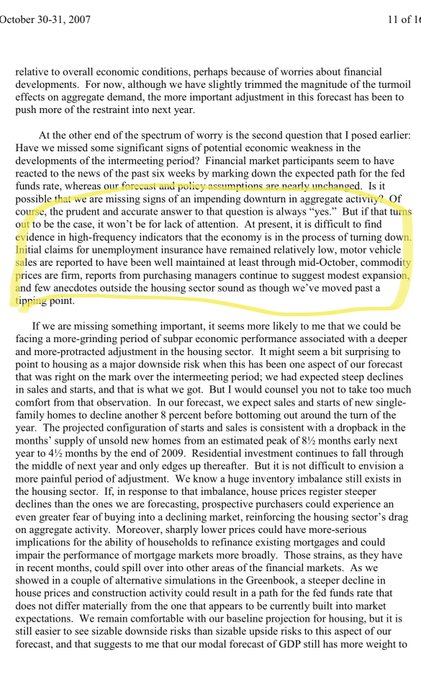

Don’t fight the soft landing narrative? This discussion at the Oct 2007 FOMC meeting (2 months before the start of NBER dated recession) calls into question just how much confidence one can derive from recent soft landing calls. Hint: little. The only true signal then was SLOO.

12

62

338

If these odds continue to swing in favor of 50 on Monday and the gap opens up, even if there is no additional Fed signal, I think we have an answer.

27

57

334

You know, we are in this predicament right now (close to even odds on 25 vs 50 bps next week) because Powell is pushing behind the scene. The Beige book strikes again!

21

35

327

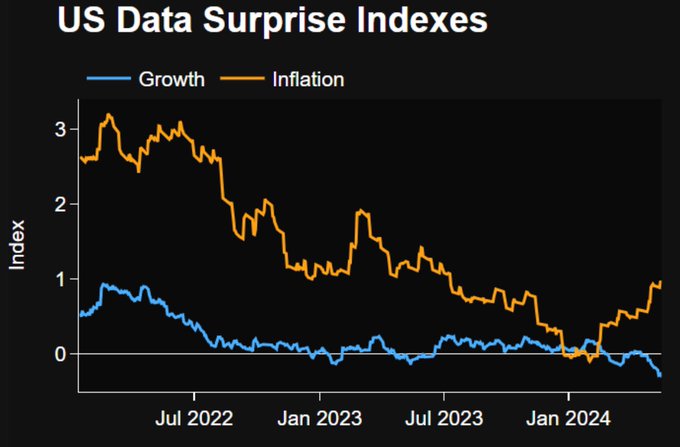

Our own growth surprises index (which uses 66 indicators) and inflation surprises index (33 indicators) are trying to tell us something. Typically they move in synch, but so far this year they have moved in opposite directions.

Inflation surprises also saw a U-turn in early 23’

18

82

325

We found a similar conclusion. Of the 20 bps increase in unemployment rate in July, we could attribute 3 bps at most to Hurricane. That would mean July’s unemployment rate would have been 4.22%- rounded to 4.2%- in the absence of the hurricane. The rest— a lot due to higher than

I thought we settled this a while ago, but I keep seeing people incorrectly blaming Hurricane Beryl for the spike in July unemployment.

Apparently, my analysis linked below wasn't convincing enough, so let's review and I'll add some more context.

Let's start with some basic

6

21

111

9

50

300

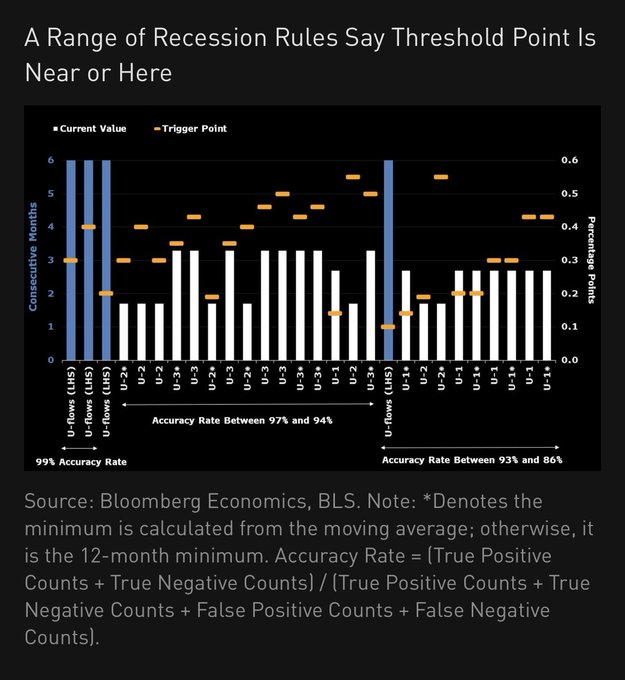

A 🧵 to add to the debate on whether this time is different when it comes to recession. In a piece with Bill Dudley today, we looked into reasons why or why not recession rules will hold in this cycle. First, U-1, U-2, U-3, Uflows say recession trigger is either near or here. 1/5

9

59

291

The reason why policymakers need to seriously consider the possibility that the economy is slowing much more than data appear is that, by doing so, they could increase the chance of soft landing. Complete denial or downplaying that will just do the opposite.

Consider this

14

65

296

Rare to go into a FOMC meeting with this split odds. If it remains this split tomorrow, chances are Fed needs to signal one way or another before the meeting …probably Monday.

17

53

288

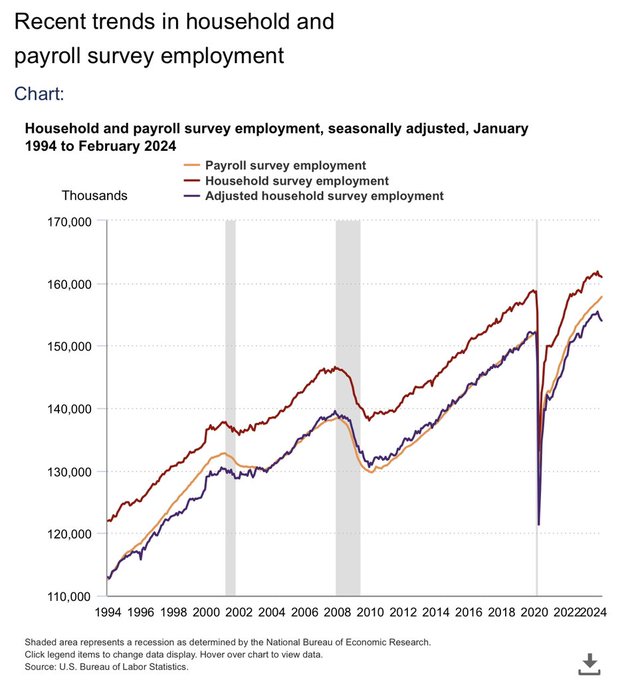

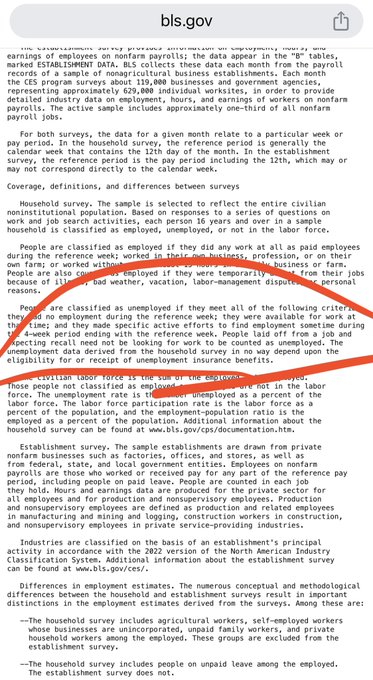

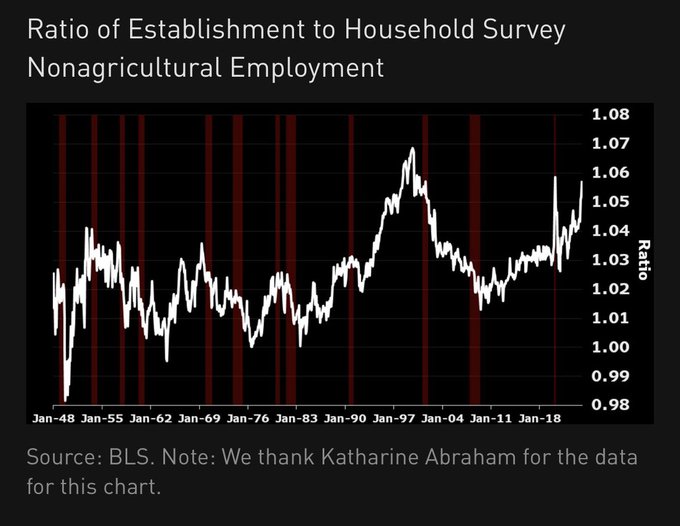

BLS has a very clear exposition of the household vs establishment survey now:

There is a simple chart there that is very striking. No need to say more. It is amazing that markets are pricing in a no landing given this.

13

74

287

A 2019 IMF paper on anatomy of sudden yen appreciation. Consider 3 episodes of sudden yen appreciation. Some feature of all three episodes are present.

5

72

286

What FOMC omits in the minutes says a ton. The 3 things that were absent but which you know they discussed:

1) cuts will happen before 12m change in pce inflation hits 2% (Powell, Daly, Goolsbee all mentioned this)

2) neutral rate may be higher (5 FOMC officials used almost

14

56

278

Now that Sahm Rule is triggered, what happens next?

Would unemployment rate continuously rise by another 1.9-2.0ppt as it always had?

@chrisgcollins1

and I wrote about this ahead of the July report here:

Using CPS micro data, we found that unemployment

13

60

276

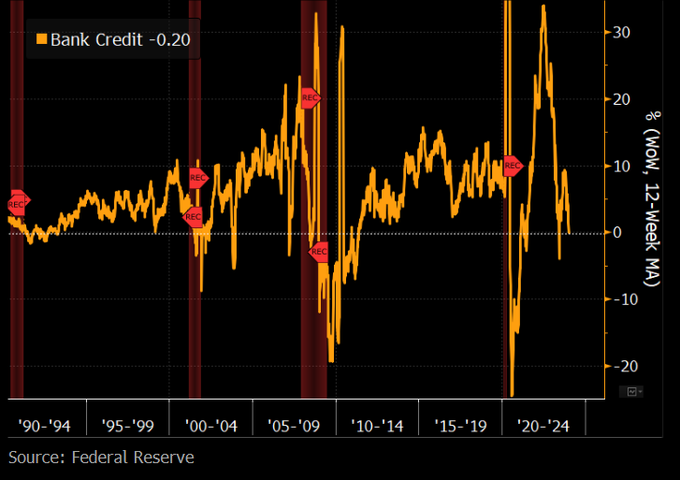

A weak data point Fed has in their pocket: bank credit contracting for 5-consecutive weeks from early Dec through early January (last seen in 2020, and before that, 2012 before QE3). Hence Waller's point that financial conditions not easing. If credit goes, so goes economy.

18

55

267

Beige book strikes again.

I don't follow the Fed. But I do sit near

@AnnaEconomist

. And earlier this week she told me the Fed would probably go with 50 bps. Anna was right. Slightly less than half of you were wrong.

2

1

20

11

23

259

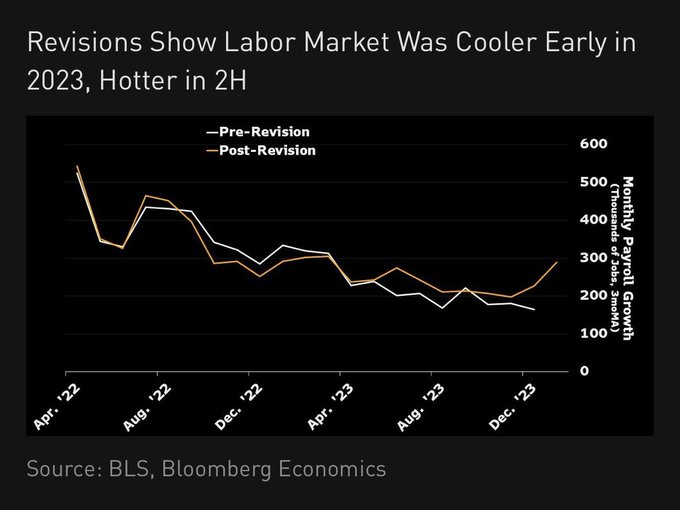

Great that Powell acknowledged payrolls are overstated yesterday —now staff can scrutinize the issue. Philly Fed just released the q4 23 early benchmark estimates - once again foreshadowing big revisions down. CES says payrolls grew 1.6% in q4, Philly Fed early benchmark says

11

60

258

There is a lot of chatters about whether last Friday’s weak payrolls was because of Hurricane Beryl: my answer—no.

The sectors that led the declines (white collor jobs) aren’t the ones that typically drove declines in hurricanes affected payrolls.

Food services and

12

52

241

While tech layoffs got all the attention, several state/local schools are laying off teachers and admin workers. That’s odd, given how JOLTS and payrolls say education sector still short of workers.

Turns out there are 3 reasons: more states are reporting budget issues, and

7

33

230

This is your infrequently-posted reminder that jobless claims is overstating the tightness of labor market. The number of unemployed that is on UI is now less than 1 in 3.

Two reasons: low eligibility and low take up.

On take up, California a good example—max weekly benefit of

12

42

229

So John Williams and Goolsbee were already pushing for a rate cut in July.

12

30

225

Frontloading over.

Biggest ever one-week drop in cost of shipping a container from Shanghai to New York. Since hitting a July peak below $6000 pr 40ft box, the Drewy global

#container

#shipping

index has seen a sharp reversal, slumping 13% this past week alone to $4168, slowing the YTD advance to

56

324

999

11

25

220

Former BLS commissioner has spoken.

The big, downward preliminary revisions to non-farm employment (-818,000) announced this morning by BLS probably stem from overestimating the number of firms in the economy. Slowing as well as recovering economies often post challenges for BLS's "birth/death" model, which BLS

51

84

343

12

43

220

Why the unemployment rate can go up even if jobless claims remain low, in BLS own words: “The unemployment data derived from the household survey in no way depend upon the eligibility for or receipt of unemployment insurance benefits.”

If you also believe that immigration drive

7

46

218

Strangely Powell mentioned several times “unexpected” intermeeting events or deterioration in labor market that could prompt earlier rate cuts. But given the low baseline for unemployment this year (4.0%), it is quite easily for it to meet that “unexpected” condition.

22

30

211

The 5 stressful Ds of life:

Debt, Deaths, Divorce, Dismissals, Disasters = Delinquency

The last D for those delinquent on FHA loans is: Disappearance (aka, “ no contact”)

H/T:

@atanzi

22

47

221

We are changing our Fed call to a cut in May on the basis of this jobs report. We have doubts about the January blowout, but the revisions for 23’ shows a hotter labor market (though even further boosted by birth death model). 3 charts:

18

40

211

We don’t think the CPI revisions are a nothingburger. Disinflation momentum stronger for core services (ie rents). Powell’s pce supercore, and core pce will be lower in end-2023. More room for core goods disinflation. This has to give fed greater confidence.

11

38

212

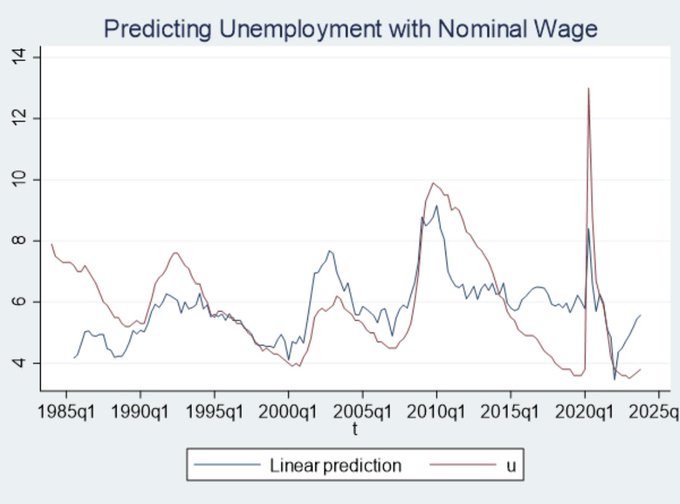

Turns out that 6 quarters of lags in nominal wage growth historically can predict the directional change of unemployment quite well. Based on that, unemployment rate should be rising much more rapidly according to this simple model. Is job openings doing all the work? Can the u

16

33

209

Highligh from FOMC minutes: “Several participants noted the risk that, if labor demand were to weaken substantially further, the labor market could transition quickly from a gradual easing to a more abrupt downshift in conditions.” They believe in the mechanics behind Sahm Rule.

14

43

203

We estimate that Dec’s core PCE inflation was 0.14% m/m. 1- 3- 6-month annualized measures all below 2%. Solid case for March rate cut based on inflation alone. (Wild card: cpi seasonal factors revisions in Feb).

17

33

198

For weekend reading, I recommend to head to the

@TheTerminal

and read this latest piece by

@ou_estelle

and me titled:

“How Fear, Carry and Tax Could Trigger Credit Crunch”

We even have a date for this risk scenario.

9

38

205

Just launched our NLP Fedspeak Index on

@TheTerminal

today. Our Fedspeak Index combines Bloomberg's timely Fed reporting+labels trained on my read of Fedspeak. It flagged for us Powell's Dec Dovish pivot. Right now its readings is similar to March 2019-4 months before rate cuts.

5

42

199

Another thread on nonfarm payrolls revisions -- An alternative jobs indicator says that the underlying pace of job growth is most likely <100k currently.

@TheTerminal

During the pandemic, both the Fed and the CEA – relied on high-frequency alternative

9

40

198

I just watched this entire interview. Listening to Lacy Hunt talk about the saving and investment identity, and walking through the aggregate econ implications, reminds me of the late Michael Mussa (further IMF chief economist) using it to explain why global imbalance was a

@AnnaEconomist

@DiMartinoBooth

I just discussed this with Dr. Lacy Hunt! Anna, he mentioned you in this episode around 32 minutes.

7

7

57

12

14

195

Here’s another forward looking thing to think about: so the CPI and PPI next week, while likely to be soft, also likely suggest that core PCE inflation will drift back up to 2.7-2.8% (from 2.6%). You think markets gonna like that? (Genuine question)

30

25

194

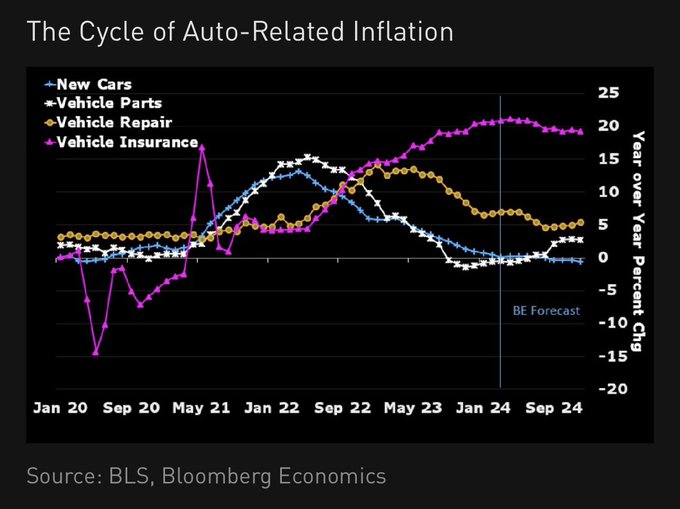

Car prices may continue to contribute to disinflation in the rest of the year, but the residual impact of two years of high cars inflation is still working its way to other auto-related services categories. Looks like the order of spillovers go like this: car prices -> car parts

14

46

198

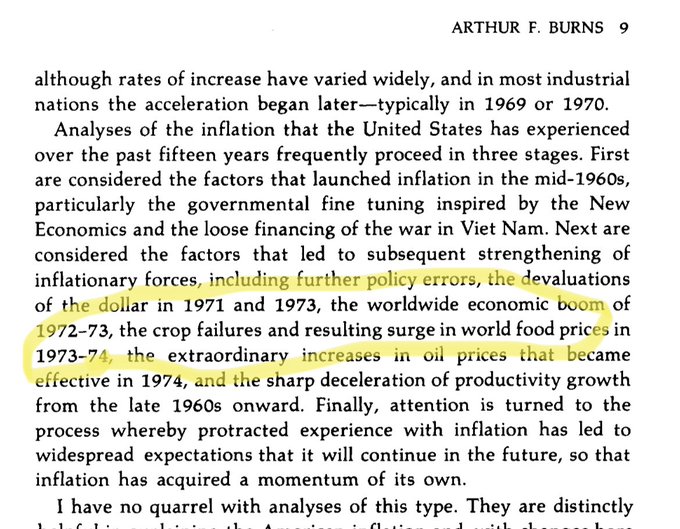

A 🧵 on weather and inflation. While we’re more optimistic about core inflation lately, progress on headline is worrisome. One of the key risk I see: el nino. A little known fact: Arthur Burns indirectly blamed El Niño on contributing to out of control good prices. 1/4

11

61

194

Hmmm…Mortgage transition into delinquency rising in q2.

@m3_melody

please give us more color please!

11

30

193

Mentions of the word “decline” spiked in beige book. 9 out of 12 districts reporting declining or flat activity, and the other 3 just “grew slightly”, is not consistent with a GDP growth of >2%.

10

38

193

I admire the ernestness of Powell’s answer at the presser on how the Fed won’t be swayed by politics in its decisions.

But let’s face it, there is no such thing as pure data dependency, as so much of policymaking requires a normative view of the economy, which in term is often

17

35

184

There's a note on immigration on the Richmond Fed website, and the most interesting sentence in it is this:

"Despite all Fifth District states experiencing positive net international migration from 2020 to 2023, immigration's contribution to population change tended to be

14

39

193

To elaborate on why this is my takeaway: he didn’t say anything about the need to be gradual, or methodical. He didn’t characterize the risks as “even”, but rather it simply “changed.” Language used to describe labor market is assured, ie cooling is “unmistakable” and cooler than

16

32

191

How the GDI and GDP gap has predictive properties on unemployment.

3

22

186

Common theme in beige book: Turnover within firms slower, but more job applicants = an unemployed worker will take longer to find a job. That is the typical beginnings of persistent rise in unemployment. Next step: as workers aren’t voluntarily leaving, firms will go to layoffs.

6

43

183

Hot CPI surprise: residual seasonality? If that's the case, Feb reading is not gonna be nice either.

7

35

179

A new FRBNY paper finds that FOMC tends to be more dovish in internal discussions than in public speeches during easing cycles (no such bias for tightening cycles). Tells you just how much to discount Powell’s performance today.

13

32

174

A theme from May’s CPI: price cuts across the board on things that consumers can skimp on, ie clothes, electronics, personal care, recreation goods and services.

Forget OER and primary rents, let’s talk about something more interesting: men’s underwear — or the lack thereof —of

29

24

179

A weedy, potential explanation about the hotter than expect ed core PCE inflation implied by the gdp print today: pce deflator weights uses a Fisher Ideal index formula, vs cpi uses Laspeyres weighting.

Why does that matter? So the PCE inflation uses moving weights, so if the

10

42

177

Why I think dot plot next week will still show 75 (not 50) bps cuts for 2024: I don’t think any of the 10 dots that saw >75bp cut will defect. My guesses of those 10 dots are:

Goolsbee

Cook

Harker

Jefferson

Collins

Williams

Barr

Kugler

Daly

Powell

19

23

170

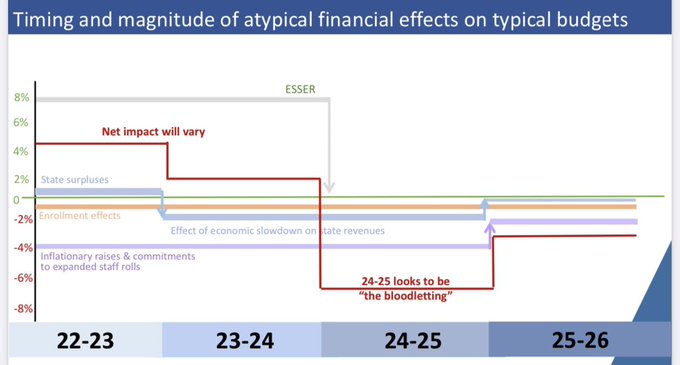

Another🧵 on the layoffs coming for state/local education sector. The minicipal fiscal cliff will be at its worst in 24-25, but 23-24 is no good either. Key drivers are:

1. Expiration of federal covid funds (ESSER). This hits 2024-25.

2. Worsening state budgets (hits 23-24)

3.

7

32

176

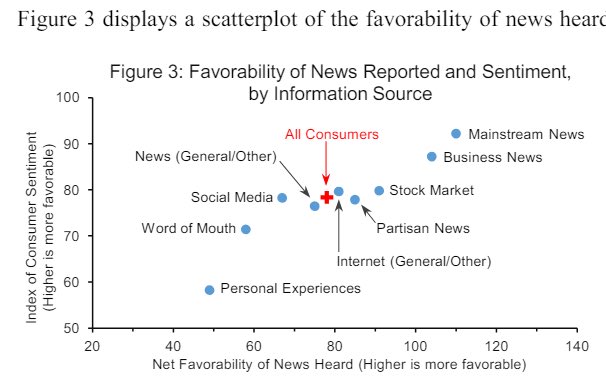

Umich sentiment survey did a very interesting survey on how people consume economic news. For one thing, it is clear that mainstream media reporters don’t need to worry too much that they are not depicting the economy positively enough.

14

44

171

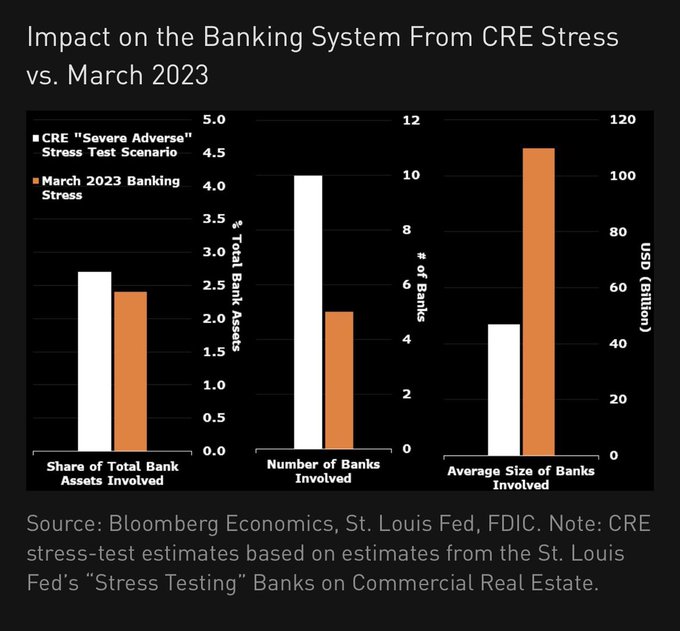

Our take on commercial real estate in comparison to the 2023 bank failures - in 1 chart. Need a 40% drop in cre valuations to equate to same amount of total bank asset affected as in 2023. But cre is more spread out risk in time, and across banks, though smaller banks.

2

40

174

Car insurance cpi jumped 2.6% in March. The problem with this kind of services inflation is that it will still keep on going in a recession.

Car prices may continue to contribute to disinflation in the rest of the year, but the residual impact of two years of high cars inflation is still working its way to other auto-related services categories. Looks like the order of spillovers go like this: car prices -> car parts

14

46

198

12

33

175

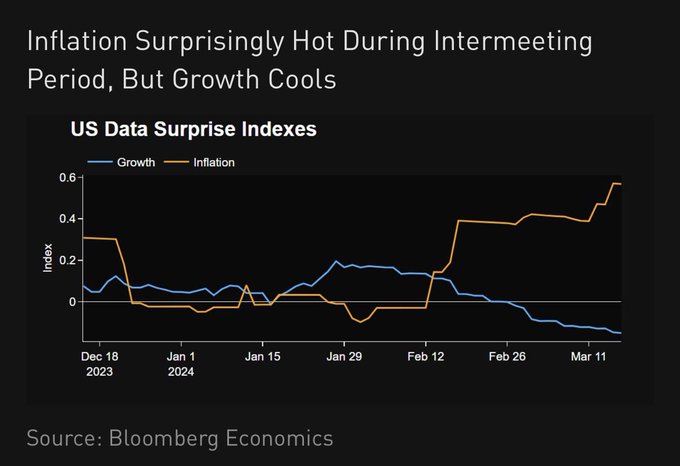

Another reason why it just isn’t clear the median would shift to 50 bp cuts for 24’: growth surprised on downside (based on 66 indicators) even as inflation surprised up.

20

52

169

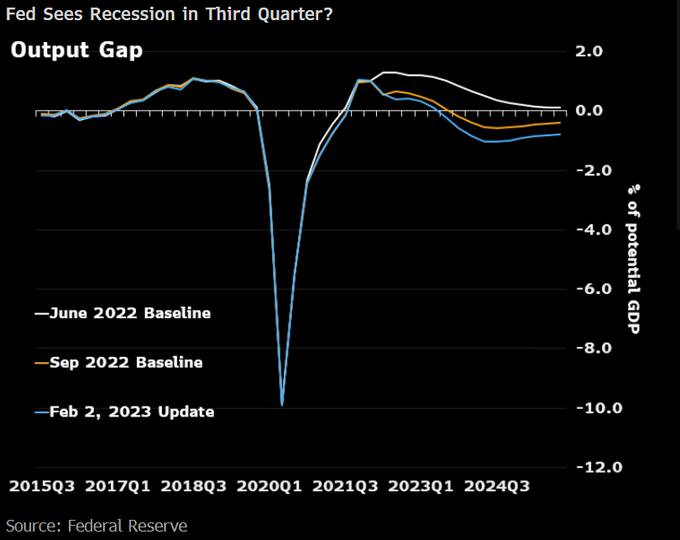

A 🧵on what Fed minutes won't tell you but FRB/US model baseline (also published by Fed, but quietly, after Feb 1 meeting) does. 1) the staff model revised down output gap. Now it falls to negative in 3Q 2023 (recession, anyone?)

7

64

162

Fastest way to stimulate the economy: have Taylor Swift add to her 9 Eras concerts in Q4. But that would probably push personal saving rate to 2%.

12

12

167

We question the emerging consensus that the nfp neutral pace is 200k+ because it is picking up the surge in immigration. There’s a more straightforward explanation: establishment is more procyclical than household survey. Has been true since 1940s. (H/t to former BLS

4

26

166

There are potential rhymes of 70s inflation today: favorable base effect of inflation decline after two years about to exhaust, Fed pivot just when that happens, just when a second oil shock may strike, officials possibly overestimating productivity, Fed keen on achieving a soft

13

42

160

Next narrative in markets I think is not whether Fed is doing 50 bps cut in Sept but could….an intermeeting cut.

Not that I think will happen. But market narratives matter.

17

12

161

This year’s Jackson Hole topic is reassesssing the effectiveness of monetary policy. Powell’s speech will come 2 days before the news release version of QCEW 2024q1.

Papers on the conference are in full swing and likely completed. But how many of them will conclude that

16

31

159

We've been suspecting that labor market is weaker than it looks. The decline in JOLTS recently seemed too small to be consistent with the ECI drop in Q2 (lately, price data has seen less drastic revisions than quantity data). A thread on wage Phillips Curve (1/n)

ZipRecruiter withdrew its annual earnings guidance due to “atypical hiring patterns”

“The number of job openings and employers’ willingness to pay for those job openings has been declining significantly from the peaks of prior years," said CEO Ian Siegel

29

150

611

6

32

159

Sitting next to me on my quiet car in the Acela from DC to NYC was a famous finance media personality. I did not eat my sushi dinner, even though I am hungry.

22

2

158

Based on CPI and PPI, we are at 0.42% for headline PCE and 0.34% for core PCE inflation in Feb. Still, we see 12-month change in core touching 2.5% before June.

9

38

157

Another key quote from fomc minutes —the key here is that “many” is actually two notches higher than “several”—so very low bar for 50 bps cuts:

“Many participants noted that reducing policy restraint too late or too little could risk unduly weakening economic activity or

11

19

157

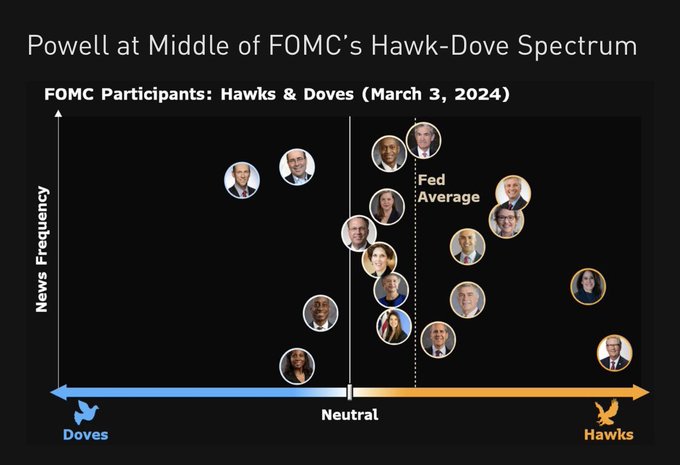

Powell will testify before the Congress tomorrow. Our NLP algo tags him as the median FOMC participant. But even the middle one is on the hawkish side. Goolsbee is on his own.

15

35

154

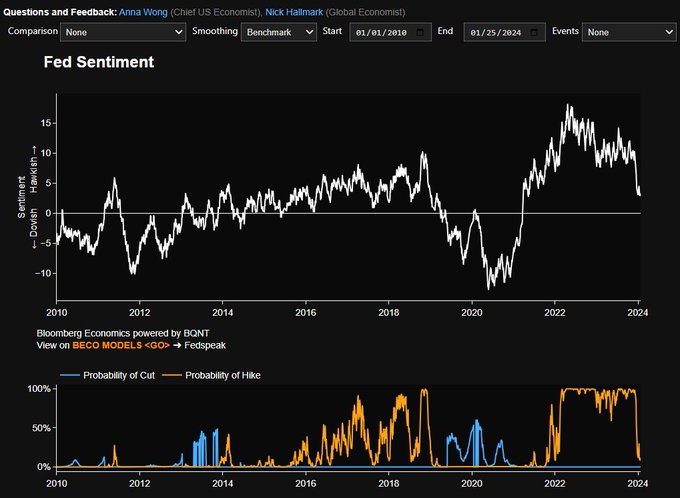

Another reason why FOMC not ready to cut: members not yet of broad agreement of that need. Here’s visualizing the dispersion of FOMC views with the help of our new weekly NLP Fed spectrometer. (Interactive version at

@TheTerminal

BECO models —> Fedspeak —> spectrometer)

6

36

152

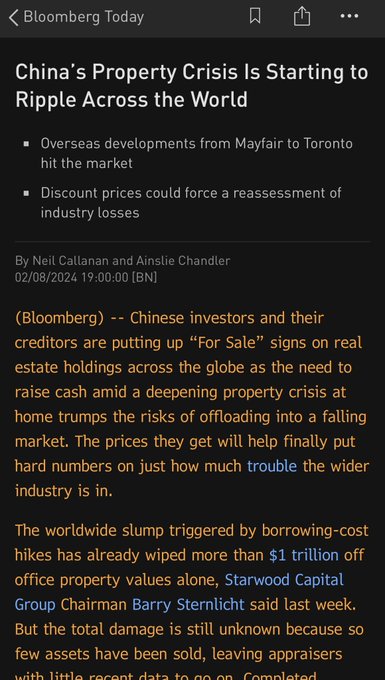

Can the world handle real estate trembles from not just one, but two largest economies at the same time?

7

24

150

There is huge body of econ literature on the role of temporary layoffs in business cycles (recessions), mostly from the 70s.

Key contributions to this literature from:

Marty Feldstein, Robert Hall (currently chair of the NBER business cycle dating committee since 1978),

5

22

149