Michalis Nikiforos

@mnikiforos

Followers

1,380

Following

435

Media

33

Statuses

270

Associate Professor of Political Economy, @DEHES_UNIGE , @UNIGEnews ; Research Scholar, @LevyEcon .

Joined January 2010

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Ohio

• 377158 Tweets

Springfield

• 269130 Tweets

Haitians

• 221061 Tweets

#JACKANDJOKEREP1

• 190910 Tweets

EP1 U STEAL MY HEART

• 160650 Tweets

#AppleEvent

• 62420 Tweets

Draghi

• 33047 Tweets

Namaz

• 32198 Tweets

PIERROT

• 16677 Tweets

海ちゃん

• 14264 Tweets

Princess of Wales

• 13188 Tweets

Culiacán

• 12502 Tweets

LISA SOLO 3RD ANNIV

• 11984 Tweets

Big Lots

• 11834 Tweets

Dreamcast

• 10924 Tweets

対象作品

• 10915 Tweets

Cowboy Carter

• 10470 Tweets

$INSDR

• 10218 Tweets

Even in very mainstream economics (micro and macro), the moment you drop the assumptions of perfect markets/competition etc. price controls are an obvious policy implication. E.g., price controls fit perfectly well in DSGE models because they assume monopolistic competition. 1/4

34

108

454

Most European countries and the US have price controls. Switzerland (definitely not a communist country) has the highest % of consumer goods subject to price regulation. This has arguably helped to keep inflation relatively low in recent years.

4/4

13

63

211

This piece with

@SimonGrothe

just came out on the blog of

@INETeconomics

. A few points:

1. Profit-led inflation does not require an increase in the markups, and is compatible with the Structuralist/Kaleckian theory of prices and distribution.

4

58

162

...Rigidities cut different ways. The fact that most mainstream academic economists use these models but reject the use of price controls out of hand (and focus only on some of the models' policy implications) betrays an ideological bias more than serious analysis. 2/4

1

22

144

This is not to say that price controls are a panacea. However, their use on a case-by-case basis can be useful both for containing inflation and for improving income distribution. 3/4

7

15

110

Lance was one of world's best macroeconomists with a huge influence on all of us who were lucky to take his classes and work with him - and of course on many other people who studied his work.

We are saddened to learn of Lance Taylor's passing. His influence, in the field and among his students, will live on, and we are grateful for everything we learned from him.

0

21

94

1

17

89

As the saying goes, here are some professional news. Send in good papers!

The Journal of Post Keynesian Economics is delighted to announce the appointment of a new co-editor,

@mnikiforos

.

Explore theoretical research on contemporary economic problems.

Here:

#EconTwitter

0

5

24

13

3

88

A preliminary result from forthcoming work with

@SimonGrothe

. Using Compustat data we find that average markups kept increasing in 2022.

3

17

85

This paper -"Notes on the accumulation and utilization of capital: some theoretical issues"- just came out in Metroeconomica. It discusses some issues related to the triangle between capital accumulation, distribution, and capacity utilization. (short 🧵)

1

11

72

This paper (co-authored with

@pacarrillom

) was just published-open access-at

@SCEDjournal

. We estimate the time varying effect of income distr. on growth. We find that the US economy became more profit-led in until the 1970s and has become less profit-led since.

NEW ONLINE 🔔 Estimating a Time-Varying Distribution-Led Regime 🔔

Great work by authors Paul Carrillo-Maldonado (

@pacarrillom

) & Michalis Nikiforos (

@mnikiforos

)

📒 Read the OPEN ACCESS paper here ⬇️

#sced

#economics

#economy

#USeconomy

#Growth

#wages

0

7

24

2

7

64

Paul Davidson, a leading Post Keynesian economist and the founding editor of the Journal of Post Keynesian Economics passed away on June 20.

4

20

61

The Journal of Post Keynesian Economics is putting together a special issue in honor of Victoria Chick, with

@YannisDafermos

,

@anninak82

,

@JoMicheII

and

@M_Nikolaidi

as guest editors.

Details in the link:

0

26

55

Our MSc in the Political Economy of Capitalism offers a uniquely-plural approach to economics.

Two weeks left for the application deadline.

More details can be found here:

1

23

53

This policy report (co-authored with

@dbpapadimitriou

and

@GennaroZezza

) came out recently. We make 5 main points: 1. The current recovery has been an important macroeconomic success (accompanied by an increase in inflation and the the trade deficit).

2

19

45

This is great! Important data will come out of this. Congratulations to the Levy Institute MEasure of Well-being (LIMEW) team.

Outstanding news! Bard's Levy Economics Institute has been awarded a federal contract to aid the Labor Department in its efforts to broaden how it measures the economic well-being of US households.

#bardcollege

@levyecon

3

32

137

1

6

42

Is it really that different though? The baseline neoclassical model remains the same. The fact that different type of market imperfections and rigidities changed the results was well understood in 1979 and way before that.

A really frustrating aspect is that many heterodox economists argue against an economics circa 1979.

8

22

212

0

3

41

Just came out: New

@LevyEcon

Strategic Analysis on the US economy (with

@dbpapadimitriou

and

@GennaroZezza

).

🧵

1

19

38

My paper "Induced shifting involvements and cycles of growth and distribution" just came out in the Cambridge Journal of Economics (advance access and for the moment unlocked). 🧵

2

6

35

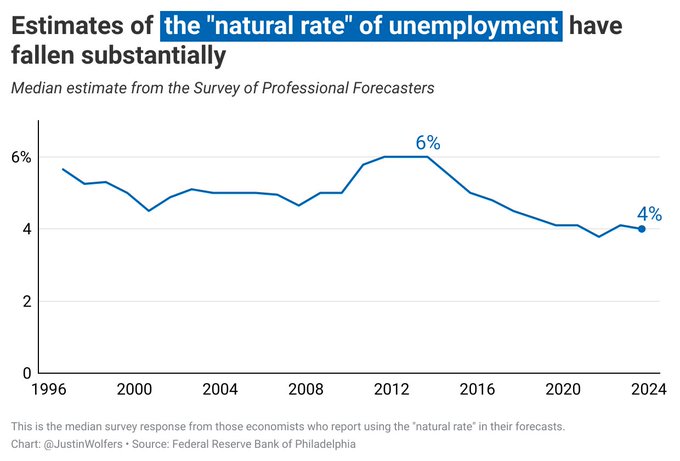

"NAIRU tracks the actual un. rate sluggishly. When un. rises, analysts discover that the demographic ch/stics are deteriorating, or that the w-p dynamic has become unstable. When the u.r. drifts down, those flaws mysteriously begin to disappear, and a lower NAIRU is estimated."

This might be the most important development in the labor market: Estimates of the "natural rate" of unemployment have fallen from six percent a decade ago to four percent.

39

50

251

2

5

34

2. An advantage of the term profit-led is that it emphasizes the distributional source of inflation: profit margins are maintained while all the burden of the adjustment is borne by real wages. Ignoring this distributional aspect naturalizes the claim of corporations on output.

2

7

32

He's never read Kalecki, but seems he didn't understand the source of unemployment!!!! 😂🤡

Just saw this reviewing a paper. I've never read Kalecki, but seems he didn't understand the source of unemployment:

14

15

59

1

3

33

For connoisseurs of capacity utilization -and the theory of growth and distribution- here is a new paper that just came out in Metroeconomica:

It makes three points:

🧵

3

6

30

Very good statement by

@TheNewSchool

. It is great to see that the NS stands its ground in this difficult period.

1

4

29

5. The piece is based on current and previous work but was inspired by Marc Lavoie's recent piece on inflation. We find profit-led inflation less controversial.

2

3

29

🇵🇸🇵🇸🇵🇸 University of Geneva, today! Assembly of the occupation in solidarity to the Palestinian people. Impressive particaption (especially on a holiday Friday).

0

7

28

This should be an interesting event. The review discusses among others our 2017

@rooseveltinst

report on UBI (with

@Econ_Marshall

and

@GennaroZezza

).

Tomorrow at 3pm ET on Zoom:

Join

@Claudia_Sahm

and

@socio_steve

for an hourlong session covering their latest white paper with

@Sidhya26

, "A Critical Review of Macroeconomic Models for a Guaranteed Income & the Child Tax Credit."

Register:

1

2

9

1

4

28

I have a chapter on "Demand, distribution, productivity, structural change, and (secular?) stagnation" in the new Handbook of Economic Stagnation (ed. by Randy Wray and Flavia Dantas). Overall great collection of papers. Check it out.

1

7

25

4. Has there been an increase in markups over the last three years? This is an empirical question. Using Compustat data we find that average markups kept increasing in 2022.

1

4

26

Join us for the Political Economy seminar next week. It will also be streamed on zoom for those who would like to join from outside of Geneva.

28/03 the Political Economy Seminar and the Advanced Research Seminar (Paul Bairoch Institute of Economic History) team up to organize a joint session with Clara Mattei

@claraemattei

@thenewschool

!

"The Capital Order"

0

5

42

0

3

23

Marc also provided a kind reply.

0

3

22

We have addressed this issue in our INET piece (link below). In a nutshell

@RiccardoTrezzi

is wrong. Ironically his graphs makes the points nicely. Even with constant markups real profits do not increase but real wages halve. This is not a distributionally neutral process.

🇮🇹 Inflazione "da profitti" e salari.

Questo commento di Andrea mi da modo di chiarire un aspetto che avevo lasciato volutamente fuori dal 🧵 precedente: il conflitto redistributivo salari-profitti creato dall'inflazione.

Sottotitolo: "Riccardo di' qualcosa di sinistra!"

1/N

0

14

78

1

3

22

Very sad news. Crotty was one of the most important heterodox macroeconomists. I only saw him once in person-at the inauguration of the "Crotty Hall" (the building named after him) at UMass Amherst- but it was always a pleasure to read his work.

Just received news that Jim Crotty is gone.

I don’t have words to describe the pain of losing Jim . He was not only my mentor and a great intellectual inspiration but also one of my best friends.

He will be greatly missed..

4

18

129

0

1

20

Here is a new paper (with

@pacarrillom

). It is yet another paper trying to estimate the effect of changes in distribution on growth. Its originality lies in that it allows this effect to change over time. 1/3

1

3

21

Yes, but accouting decompositions reduce the degrees of freedom of causal analysis. This decomposition says that the wage-price spiral story-which is the main mainstream explanation for inflation and guides int. rates increases by the CBs-does not hold.

This tweet frames an accounting decomposition as a causal effect. When demand rises and supply cannot follow, prices and margins go up. That doesn’t mean that companies decided out of the blue to raise prices and make profits, thus causing inflation.

39

184

829

0

0

21

Here is our entry on Stock-Flow Consistent macro models in the New Palgrave dictionary of economics.

0

1

20

Also very important, when the tide turned he refused to join the "dark side" (that is how he once called during a class the new-Keynesians and neoclassicals!).

We shall miss him but always treasure his work.

0

5

20

This is a great set of sessions organized by

@leilaedavis

,

@JFCogliano

and

@Kumar_EconIneq

. I wish I could be in NYC!

Attending the Eastern Economics Association conference in NYC this week? UMass Boston Econ professors

@JFCogliano

@leilaedavis

@Kumar_EconIneq

are organizing 15 different panels over Feb 24-25 covering a range of topics in heterodox economics.

#EEA2023

1

7

29

0

2

18

...Over the last decades profit shares have increased in most developed economies and this increase has been accompanied by a secular increase in the markup of the firms. An increase in the markups that would amplify price shocks would be consistent with these trends.

1

2

18

This is a great opportunity for a post-doc at UMass with

@IsabellaMWeber

!

Thrilled to be hiring a postdoc at the UMass econ department thanks to OSF funding!

I’m looking for someone with a PhD in social sciences, economics or history to join me in working out the economics of essential sectors for our age of emergencies.

9

141

368

0

5

16

3. In Structuralist/Kaleckian analysis, the *exogenous* markup does not mean that markups and profit shares are overall *constant*, but rather that they are determined by institutions and social norms outside of the economy along the lines of classical political economy...

1

2

17

I wrote this 8 years ago. Comes to mind every couple of years since then! Also, yet another example of the cliché metaphor of a "new Lehman moment".

0

5

17

A good summary by Kindleberger of New-Keynesian economics and their acrobatics: "I think you have provided a most ingenious solution to a non-problem" [i.e., reconciliation of the obvious inefficiency of the depression with the postulate of rational private behavior]

In the papers of economist Charles Kindleberger,

@PMehrling

found notes on the paper that won Ben Bernanke his Nobel Prize.

1

11

35

1

1

15

Congrats

@IsabellaMWeber

. At the same time I cannot help to mention that it is hilarious how in German translation of "How China escaped the shock therapy" becomes "The spook of inflation"!

BUCHPREMIERE ist wirklich ein schönes deutsches Wort. Der Vorhang öffnet sich, "Das Gespenst der Inflation" tritt hervor. Bin jetzt schon voller Vorfreude auf das Gespräch mit

@schieritz

! Herzlichen Dank an

@suhrkamp

@BoellStiftung

@IMKFlash

! Join us! 🍾🥂

8

47

186

1

2

13

He had a unique style of doing macro with a combination of sophisticated theory and applications/policy using broad strokes of data and orders magnitudes- along with history, institutions and the economy's structures (he was a structuralist after all).

1

3

12

2. Inflation is largely unrelated to the level of demand or the pace of the recovery and is mostly related to the disruptions due to the pandemic. E.g., Here is a graph with growth and inflation in several OECD countries; there is no correlation.

1

5

12

@heimbergecon

@spignal

@PhilippaSigl

These are the projections of the adjustments programs and their various reviews (in levels and growth rates). So, no, the collapse in GDP was not part of the plan. Given the projected growth rates GDP would recover to its precrisis levels within a few years.

1

1

11

We estimated the (very positive) macro effects of a (roughly) 2tn public infrastructure plan with a simulataneous increase in tax rates for corporations and rich households a couple of years ago here:

1

4

11

Truncated and paraphrased "quote" from James K. Galbraith's "Time to Ditch the NAIRU" (JEP, 1997)

0

1

10

Here is the lineup for our seminar series this semester!

Here is the program of the Political Economy Seminar for the next few months! For more information:

@bruno_amable

@lauraabcarvalho

@IsabellaMWeber

@aldelatte

@benjlemoine

1

9

27

0

0

11

J'ai été interviewé pour cet article dans "Le Temps" de Genève sur l'inflation, ses risques pour la croissance et ce qu'on peut y faire.

I was interviewed for an article of Geneva's "Le Temps" on inflation, its risks for growth and what we can do about it

1

5

9

If we account for "base effects" for shelter inflation, the rate of inflation today is not different from what it was in the five years before the pandemic. This leaves with sources of inflation pretty much unrelated to the strength of the recovery in the US.

1

0

9

Lastly, Ignazio Silone would recognize his beloved cafoni in the way this thread is written.

0

0

7

Lovely video-account of our fantastic summer school. Looking forward to the 2024 edition! 💥😍

@UNCTAD

@ysi_commons

@INETeconomics

(kick-ass comments by

@livia_dell

& Tinashe! thks!!)

2

6

25

0

0

9

Here is a new working paper coauthored with

@SimonGrothe

entitled "Contractionary effects of foreign price shocks (and potentially expansionary effects of inflation)."

A small 🧵:

1

2

9

@jj_carloriv

@IsabellaMWeber

Thank you for your kind reply. Indeed, the exchange rate and other factors (such as less reliance on gas) also played a role but so did price regulations.

1

0

9

Shame on you

@TheNewSchool

. You betray all the values the school is supposed to represent.

As announced on Monday, we have made the difficult decision to stop paying wages and premiums for healthcare benefits for employees who are striking. Up to this point, we have continued to compensate our faculty and staff who have chosen to exercise their right to strike.

2K

130

284

0

1

9

4. It argues that when it comes to the normal rate of utilization it is the expected growth rate of demand that matters, and not the level of demand. This insight provides a more straightforward way to link the adjustment at the micro and the macro level.

1

0

8

@Lprochon

@IsabellaMWeber

But is this really a "reply" or just a clarification (that increasing profit shares don't require increasing profit margins/markups)? I don't think that the story of

@IsabellaMWeber

is incompatible with constant markups.

5

0

8

Our calculations follow De Loecker et al (2020) and recent work from

@rooseveltinst

,

@mtkonczal

,

@NikoLusiani

.

1

0

7

Comments or -even better- criticism are more than welcome!

0

0

6

His work on macroeconomics, his insistence that macroeconomics is necessarily monetary, and his advocacy for policies that would promote full employment and social justice have been a great inspiration for many non-mainstream economists.

0

0

6

Material for a sequel of Dr. Strangelove!

Sen. John Kennedy (R-LA) presses Biden’s pick for currency comptroller Saule Omarova about “you used to be a member of a group called The Young Communists.”

Omarova explains, because she was born in the Soviet Union, she was part of school youth programs mandated for students.

1K

2K

9K

0

0

5

1

0

6

This looks like a very interesting get-together this summer at Duisburg-Essen.

---Call for Papers Alert ---

Join us for the 5th Pluralumn Workshop from August 6-8 at the University of Duisburg-Essen dedicated to connect young scholars with a pluralist approach to economics.

Deadline: May 19

Further info and submission:

3

28

31

0

0

5

Finally, the paper shows that it is possible to have fluctuation between conflict and cooperation within each of the distribution-led regimes.

0

0

5

3. It provides some concrete examples on why demand is a determinant for the long-run rate of utilization of capital.

1

0

5

One of the rare times Facebook algorithm proved useful. This is important now for more than one reasons.

0

0

4

It makes four main points: 1. It explains why utilization is a crucial variable for the theories of growth and distribution, and their ability to combine an autonomous role for demand (along Keynesian lines) and an institutionally determined distribution (along classical lines).

1

0

5

We find that the US economy became more profit-led in the first postwar decades until the 1970s and has become less profit-led since; it is slightly wage-led over the last fifteen years. 2/3

1

0

5

@cacrisalves

@farwasial

@hetecon

@heterodoxnews

The course is co-taught by

@bruno_amable

and Mary O'Sullivan. Here is its description:

1

1

5

In Dec 2008 we had occupied the building that stood in the place of the university center-with similar demands. 14 years and 2 administrations later the situation at

@TheNewSchool

seems to be worse. Solidarity to the strikers and the students.

@TheNewSchool

students

#occupy

the university center to protest the reckless polices of President

@dwightamcbride

.

3

9

62

0

0

4

Here is also an interantional comparison on the rate of growth and the rate of inflation (2019-21) for OECD countries. No obvious correlation.

1

0

4

This is very sad news. Peter Flaschel was a great economists and a very nice and generous person.

With great grief and sadness I announce the passing of my PhD advisor Prof. Dr. Peter Flaschel

@unibielefeld

, 2006 Heuss Professor at

@NSSRNews

. The profession loses a great & prolific scholar as well as a kind & humble human being, and I lose a dear friend. May he rest in peace.

20

9

97

0

0

4

@odavis_

@vebaccount

There is disaggregated data (see table), but no sector seems to be running too hot. I think the bottlenecks/constrained sectors story is correct, but these constraints come at this point outside of the US economy.

0

0

4

2. It responds to some recent criticism by Girardi and Pariboni (2019) and I explain that their interpretation of the model in Nikiforos (2013) is misguided, and that the results of the model can be extended to the case of a monopolist.

1

0

4

4. Because of the fragility of the corporate balance sheets and the overvaluation of the stock market, tightening monetary policy risks causing a financial crisis, with severe consequences for the US economy in terms of output and employment.

1

2

3

@Lprochon

@IsabellaMWeber

In the abstract and the paper they write that firm protect their margins - and some even expand them. Of course, the fact that rising markups is not a prerequisite for higher profits shares does not mean that there have not been rising markups. But this is an empirical question.

1

0

4

Haven't tried this yet, but looks interesting.

0

0

4

0

0

4

Presents our forecasts for the US economy, and shows why an infrastructure and families plan could have positive macro effect.

And argues that concerns about a sharp increase in inflation spurred by the fiscal stimulus are unwarranted.

0

1

4

And here is a video with me presenting the report in the latest Levy summer seminar in June.

0

1

4

Some preliminary analysis shows that the increase is not as broad based as in 2021. Some of the increase is due to firms with higher markups increasing their market share. More details coming soon.

0

0

4

@ProfDavidFields

@Lprochon

@ReviewofPE

@RicardoSumma

Rudi, Marcio and I have different takes on the profit-led story (I believe that the demand regime changes over time). But this is a different debate. And I do not find convincing a story where the cycle is driven by autonomous (exog.-to-demand) fluctuations in resid. investment.

0

0

3

The more the two classes prioritize the increase of their income share over economic activity, the more possible it is that the economy is unstable (lambda=degree of wage-ledness, pi=profit share).

1

0

3

@JWMason1

So, the accumulation of debt by the pr. and/or gov. sector are a consequence of this CA deficit increase.

1

0

3

@ProfDavidFields

@Lprochon

@ReviewofPE

@RicardoSumma

@ProfDavidFields

you are right that the results change when the two types of investment are treated separately. The critique though remains valid. We explain why this is the case in the rejoinder.

1

0

3

@JWMason1

@EconBerger

@andrewelrod

@rortybomb

Here are two more papers which might be relevant. The decrease in util. over the last 3 decades can only be explained by lower demand. All other factors have moved in a direction that should have increased it.

2

1

3

He continues: "If one believes in rational expectations, a nat. rate of un., efficient markets,...there is not much that can be explained about business cycles or financial crises. For a *****Chicagoan*****, you are courageous to depart from the assumption of complete markets."

1

0

3

Tomorrow at Uni Mail and online.

16/05 Next session of the Political Economy Seminar! We are pleased to welcome Thomas Fergusson

@INETeconomics

!

"Industrial Structure and Politics in the New 'New World Order': The Case of the US"

0

2

3

0

0

3

Argues the even before the pandemic the US economy was not anywhere close to full employment

1

1

3

@CFlowMuzik

"because of discrepancies in source data, timing differences, and difficulties in adjusting the source

data to remove holding gains from reported revenue or

changes in positions." See page 14 in this documentation of the IMAs:

1

0

3

@heimbergecon

@spignal

@PhilippaSigl

The forecast was that austerity and "reforms" would have a marginal effect on consumption, a medium run positive effect on investments, and would lead to a boom in net exports.

0

0

3

On the other hand, as the profit share increases, the economy tends to become more wage led. There are good theoretical and empirical reasons that justify this (think of the decoupling of investment from profits over the last decades).

1

0

3

@Lprochon

@IsabellaMWeber

There is for example some evidence (albeit still inconclusive) that the markups did increase:

1

0

3