Ira Joseph

@ira_joseph

Followers

12,944

Following

134

Media

1,259

Statuses

16,185

Global Fellow, Center on Global Energy Policy, Columbia University. Former Head of Pricing & Analyics for Generating Fuels & Electric Power at S&P Global

New York, NY

Joined November 2012

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

النصر

• 932542 Tweets

التعاون

• 714319 Tweets

Washington Post

• 217653 Tweets

Durk

• 201587 Tweets

Virginia

• 175759 Tweets

Bezos

• 97452 Tweets

Tommy Robinson

• 83839 Tweets

LA Times

• 75798 Tweets

WaPo

• 70445 Tweets

Boulos

• 53123 Tweets

Democracy Dies in Darkness

• 42509 Tweets

Edwin Santos

• 40629 Tweets

#荒野7周年空前の超感謝祭

• 40507 Tweets

#史上初金車確定無料ガチャ

• 40157 Tweets

Marçal

• 39024 Tweets

Chicó

• 38512 Tweets

#الاهلي_الاخدود

• 26945 Tweets

レジェンド車両

• 23316 Tweets

全員最大金枠アイテム5つ

• 23276 Tweets

Tether

• 20341 Tweets

Spider-Man 4

• 18601 Tweets

بن زكري

• 18167 Tweets

Leicester

• 16754 Tweets

Albon

• 14256 Tweets

Last Seen Profiles

No, general public, you’re not confused. Yes, the Russians and Ukrainians are fully cooperating to send more Russian gas through Ukrainian pipelines to European buyers, who will pay the Russians, who will use the proceeds to invade Ukraine. War above ground, capitalism below.

42

270

639

Here’s another thing. The Chinese will never stop building more EVs, solar panels, and wind turbines at any cost. It all minimizes reliance on oil & gas imports. It’s not about being clean for China; it’s about more self reliance & sitting at the table of major energy producers.

This is the thing that people are having a hard time grasping, higher oil and gas prices make input costs higher across the energy spectrum.

16

81

385

22

26

174

Europe could buy a lot less Russian gas if France could get its nuclear act together. These pitiful numbers will not be turning around soon, as the problems are widespread. EDF is currently declaring ~50 GW of capacity will be available in Q4-22 & 54 GW in Q1-23. We'll see.

#ONGT

14

45

128

#LNG

is now the dominant form of trade in gas. Even if all the Russian pipeline gas would return, LNG would still be a larger market than pipeline gas. These two lines will continue to diverge as most investment flows into creating more LNG supply.

#ONGT

@ColumbiaUEnergy

8

37

125

If 2024 European gas demand stays on YTD trend, we are looking at demand levels equivalent to 1984. Yes, 1984 as in mid Thatcher. Policy decisions favoring renewables, combined with high gas prices tied to the Russian invasion of Ukraine, have been devastating for use.

#ONGT

9

37

125

European storage today is where it normally resides on Jan. 10; put another way, about 20 bcm of withdrawals into the future. Not good for buyers; real good for sellers. Starting to talk myself into a possible TTF/JKM winter inversion if regional temperatures break a certain way.

6

45

125

2021-22: the world cannot conceivably keep up with projected lithium demand

2023: we found a lot of lithium

2024: supply is outpacing demand and we need to shut in capacity.

202?: turns out the rapidly evolving battery and EV markets may not have core dependence on lithium.

The lithium market has experienced a turgid 12 months, during which demand failed to keep pace with supply, weighing on prices, and the new year has already seen its first major project suspension, with market participants warning that more are to come.

7

12

42

10

23

124

Big week for the

@abaxx_exchange

@nsundar79

@James_Duade

@ira_joseph

@ColumbiaUEnergy

@abaxx_exchange

is launching a LNG physically delivered contract this week with delivery points around the world

1

2

34

1

12

100

JKM is spiking, Henry Hub is falling, & US LNG producers are as wide-eyed as a kid in a candy store. US LNG send outs will shoot up as soon and as quickly as possible because these types of opportunities do not grow on trees. JKM/HH Nov. spread is $2.65 and freight is only $1.50.

7

49

111

Two areas of focus. 1) Despite high prices, European gas demand is smack dab on the 5Y avg. 2) Look at how wide the demand possibilites are (5Y range) once seasonal gas demand kicks in. The highest degree of variability emerges when colder weather arrives...or doesn't.

#ONGT

7

39

112

To avoid further confusion caused by yours truly, here is the complete Qatari

#LNG

contract palette through 2030. Portfolio volumes do not have a fixed destination and the Others are geographically dispersed.

10

38

108

The electricity consumption from crypto mining is equivalent to around the 20th largest country in the world. A plunging Bitcoin price is capable of having a demonstrative effect on power consumption. Where the effect occurs is trickier to determine, as mining is so fluid.

Bitcoin's plunge from a record high last year has erased $200 billion in value from crypto stocks

10

19

69

9

39

102

China, as a buyer, is diverting

#LNG

to Europe for the same reason that the US, as a seller, is diverting

#LNG

to Europe; they are maximizing returns. No one is trying to be anyone's bestie here. Nobody is discounting. Europe is paying top dollar and China is happy to take it.

China deciding to go heavy into coal, thus freeing up LNG to meet Europe demand, is a big reason Putin's energy leverage over the EU has dissipated.

Explain to me again how Beijing is Putin's ally?

5

54

136

7

26

96

A banner year took place for Russian gas production in 2021. Record production still dipped seasonally, but from a much higher apex. Volumes are going full throttle now, but what's leaving the country is an entirely different matter, especially when it pertains to Europe.

#ONGT

6

32

98

August was a brutal month for European gas demand; the lowest I could find this century. Seasonal use should lift demand slightly in September, though Y/Y losses will continue due to lower industrial & power sector use tied to stubbornly higher prices.

#ONGT

@ColumbiaUEnergy

9

46

96

Does this look to you like the demand profile of a $30 (€91) gas market? Yeah, me neither. Will need to re-write the books on European demand elasticity to price going forward, as gas grows its intermittancy role. Note that sector swings are occurring within this total.

#ONGT

12

27

94

Wouldn't slap the train wreck moniker on European demand just yet, but signs are emerging that it's traveling more sideways than heading northeast; a more typical direction for the season. Fuel switching signals remain unfavorable for gas burn, while more LDC use is inevitable.

5

20

93

The swing in US

#LNG

exports to Europe is not the 1st & will not be the last. Notice the drop in Qatari volumes to the point where Russia (yes, that Russia) is now the 2nd largest LNG supplier to Europe. Egyptian volumes are also up, threatening to pass Algeria for the 5th spot.

7

29

88

Never seen European gas demand rise M/M in February, even including weather. Then again, prices falling by $6.50/MMBtu since Jan. 1 will do some strange things. February demand is still below the range, but the ability to afford burning gas around $15 seems to be growing.

#ONGT

2

23

89

Major European buyers must be making a boatload of money. Even if they re-sell off a small fraction of their oil-indexed Russian gas, they must be cleaning up. I’m going with silence = complicity as my answer. And don’t forget the margins on gas in storage. It’s contango heaven.

We have to admit that

#Putin

has a gas narrative that makes sense.

European gas companies are lacking transparency to check this narrative😡

8

26

66

5

25

88

Total’s Pouyanne, in the middle of a Faulknerian sentence run, talks to the bottom line on coal to gas switching, “If we replaced the world’s 9,000 coal plants with gas plants today, we’d achieve the 1.5 goal immediately.”

#GlobalEnergySummit

8

27

85

Record high prices? Meh. Europe is consuming gas like it's trading at €15 and not €80/MWh, which is going to keep the pressure on storage to make up the difference, even 2 months ahead of winter. If more LNG & Russia gas arrives, so be it. For now, demand is ignoring price.

6

21

84

January marked the 2nd month in a row of record gas production in Russia, even as Gazprom reported a 41% Y/Y drop in overall exports. Jan. output of 2,239 Mcm/d is up a smidge Y/Y, according to official figures. Production of 2,090 Mcm/d in 2021 was also an annual record.

#ONGT

6

29

83

Perhaps this is a mere coincidence. The Y/Y decrease in Russian gas exports to the EU is the exact same volume -- 150 Mcm/d -- as the capacity of NS2 pipeline. Overall, gas exports to the EU are half what they were back in 2018 and 2019.

#ONGT

.

10

32

83

The story for me thus far is how intensely inelastic gas demand remains at these prices. Anyone concerned about the bridge-like qualities of gas should keep this in mind. The greatest curse and blessing for gas is the stickiness of its infrastructure compared to coal or even oil.

6

17

82

Correct. Between their attractive Russian & US gas contracts, some European utilities are going to have some explaining to do because they are importing vast amounts of gas at attractive prices relative to the spot market. I’m sure they’re fully passing it through to end users.

@hcanercan

@APIenergy

Yes, spot

#LNG

prices in Europe (TTF) remain too high, but don't forget that several European utilities bought

#USLNG

years ago and THEIR volumes are priced not at TTF, but Henry Hub + Liquefaction + Transport. Deals by

@Naturgy

,

@centricaplc

,

@Endesa

, EDF, EDF seem prescient.

2

5

22

9

19

79

Speaking of effective lobbies, hat tip to the US shipping industry. The US has zero Jones Act-compliant

#LNG

tankers, so the largest LNG exporting country in the world must import LNG or truck it a mighty long way. Which sounds safer to you, the ocean or I-81 and I-95? Madness.

7

20

78

Looks like European gas demand is fairly agnostic to both price & weather with little in the way of deviation from history. On aggegate, that's bullish for price given that constraints on imports, stronger storage draws, and low wind are also playing supporting roles.

#ONGT

2

24

78

Highest Oct. gas production. Ever. They must be stuffing it in the seat cushions at this point because it's not going to Europe & seasonal demand is still ramping up. Higher gas switching domestically is possible, but it has to be tempting to cash in on exports at this point.

7

29

74

Sept. production was still 195 Mcm/d below the record (Feb. 2021), but it does suggest we could run up against potential capacity constraits well before the winter peak if it's cold inside & outside Russia. Production is up by a sizable 12.5% (229 Mcm/d) so far in 2021.

#ONGT

2

44

76

OK let's review. NS2 was lobbied into purgatory because pipeline flows were going to be used as a commercial and political weapon. OK, now what? Frankly, I'm not sure the Russians ever want NS2 to open given how they're now cleaning up financially. Unintended consequences 101.

Gazprom has not booked any capacity on Yamal Europe for Friday. (In the first half of December it was booking ~40% of Yamal's daily capacity)

5

9

40

8

13

77

Well stated. Makes you realize that perpetual war is profitable for Russia, so why stop? When war pays, you keep at it, especially if no vulnerability on the home front is readily apparent. Hard to justify a deflation in the risk premium if the status quo remains indefinitely.

First month of war:

EU > Ukraine ~ €5bn

EU > Russia ~ €20bn

Unfamiliar to give 4 times more to the aggressor than to the attacked…

When will we all acknowledge that?

3

23

65

10

25

75

Russia is doing Germany and the rest of the EU a favor by forcing them to confront what they wouldn’t otherwise on their own. We can have a reasonable discussion whether Russian gas was a weapon of war pre-invasion. Now it’s there for all to see and there’s no going back.

#ONGT

3

35

73

It's the biggest mystery since Roswell. The lack of drilling response at these prices is hard to understand. Investors were throwing money upstream if gas approached $2.50 and was maybe in the money. Now they're treating $4 gas like the plague when it's definitely in the money.

23

15

73

Compelling argument by Rystad at

@GastechEvent

that $8 is the new $5 when it comes to demand for higher

#LNG

imports. They also mentioned India is well contracted thru 2028, so maybe we should see India as a limited spot buyer.

#ONGT

@ColumbiaUEnergy

7

12

74

European gas demand will be at its seasonal low point for another 2 months. This year's data shows demand hit closer to rock bottom earlier in the year, although dropping below 600-Mcm/d on a monthly average is not out of the question in August and Sept.

#ONGT

@ColumbiaUEnergy

4

23

71

Looks like New England will be buying its

#LNG

this winter from Trinidad once again and probably for the time being. Why not from the US Gulf Coast you ask? Please don’t make me say it. I beg you.

The US imposed sanctions on Russia’s new LNG export project

🇺🇸 🇷🇺 ⚠️

🚢 Arctic LNG 2 was added to a list of sanctions. Production is slated to begin by year end

👉 This is the first US sanction directly on Russian LNG

🇫🇷 France’s Total, Japan’s Mitsui are investors in the plant

10

91

207

10

15

72

Norway certainly isn't holding anything back in its quest to cash in on European gas prices. October exports are approaching a 5-year high, touching levels usually reserved for mid-winter. UK imports have become the top destination, followed by Germany & the Netherlands.

#ONGT

7

30

68

October 8 established a new all time record for European gas storage. Injection season has roughly another 30 days to go, and Norway is back near full production capacity as of today. Another 3.3 Bcm of storage capacity is available to utilize.

#ONGT

@ColumbiaUEnergy

3

22

69

When I look at European demand & storage levels, neither are as unprecedented as this price. Not even close. The difference maker is supply & fear of overseas buying. No way to cap how high this can go...or how quickly it nosedives if the wind sustains & the weather is warm.

NATURAL GAS MARKET: Both UK NBP and Dutch TTF natural gas benchmarks have closed the day at their **highest ever settlement level**, up ~11% on the day (to a closing price equal to more than $26 per mBtu).

30

230

531

6

19

68

It’s just downright bizarre that Germany would restart coal plants rather than first extending the life of its remaining nuclear plants, at least for a spell. Limit the in-office work week to 3 or 4 days for next 6 months to curb demand and then give it a rethink.

12

14

68

It’s also clear that the Russians are watching the European gas storage number and saying “it’s filling too quickly and we’re losing control. Let’s cut more.” Russia wants to control the winter swing and the more gas that’s in European storage, the less swing they control.

#ONGT

5

31

66

Without a doubt, it’s coming. Then some piece of equipment sourced in The Netherlands or Newark will be unavailable for replacement and the venting will begin. Environmental blackmail is next because the cruelty is the point and nihilism is the sport of unchecked power.

In a short time from now you will all here about Gas Flaring

Russia will have to burn tremendous amounts of gas because they have no infrastructure to re-sell it to other destinatons than Europe

96

60

446

9

17

66

Had to lower the Y axis because August gas demand is really low in Europe. All sectors are getting pummeled with power stations being the most noticeable. No doubt industry is also down, but it's far from the entire story. Europe is pricing itself out of its own gas use.

#ONGT

3

13

64

If you're not following solar panel manufacturing capacity & output in China with the same intensity as Opec production, you're missing the bigger picture on how China is vying to undermine the global energy balance. Profits don't matter; it's a pure power play.

@ColumbiaUEnergy

56 gigawatts/year of manufacturing capacity! At a single facility. That's 73% more than ALL solar PV installed in the US last year. In the not too distant future, the emergence of ubiquitous, cheap, clean energy from solar PV will be regarded as an epochal moment in human history

13

75

379

9

24

65

A LNG import terminal is more like a storage facility; you would never use it 100% of the time.

#LNG

receiving terminals have a long history of operating at 40% capacity as they are designed for peak, not baseload use. The flexibility is the point and where the value rests.

#ONGT

Europe at Peak LNG Heightens Risk of Stranded Assets, IEEFA Says

Half of EU terminals had utilization rates below 50%: report

Germany’s renewables push likely to trigger LNG overcapacity

3

6

20

5

13

64

Hear me out. Europe needs to inject at 155 Mcm/d to be full by Nov. 1. It's currently injecting at 315 Mcm/d. If it continues, it's full by mid-Sept. If the market loses 150 Mcm/d of Australian

#LNG

, it loses it here as injections & will still be full by Nov. 1.

@ColumbiaUEnergy

8

12

63

If the

#LNG

spot market is not robust enough for you yet, look what's in store. Roughly half the world's LNG under contract needs to be resold if end users continue to shy away from long-term deals. Plus, look at the unsold liquefaction capacity post-2027.

#ONGT

@ColumbiaUEnergy

2

18

63

European gas demand stopped the Y/Y bleeding in October. Seasonal gas demand will more than double in the next 60 days, although aggregate storage is still showing net injections. How weather-sensitive demand responds to price is the not-so-secret ingredient in this mix.

#ONGT

4

31

60

Bookmark this one. It will take another 15 versions of this piece to make people realize the significance of this observation. Especially in China and major global cities. Important on the power demand side too given the potential impact on renewables, gas, and coal.

#ONGT

"E-bikes and scooters displace 4x as much demand for oil as all of the EVs in the world."

74

720

4K

5

22

61

Henry Hub is starting to behave like it has the same risk profile as TTF. It does not. Non-commercial money is loading up on HH, with lack of production growth as the fundamental feature. Market is tighter, but $7 tight seems a bit exaggerated. Producers smiling from ear to ear.

4

24

61

Exactly correct. Who's to say that we can't go from an incredibly bullish market during the lowest point of the year for seasonal gas demand to an incredibly bearish market during the highest point of the year for seasonal gas demand? Rules you say? Rule

#1

is there are no rules.

6

11

59

When I can cut back the Y axis to 85%, it's a moment. Back in the day, the assumption was 85%-90 globally & annually! Not anymore. The 10% point drop since April has been a real driver of price. Nigeria, Trinidad, Peru, & Norway provide the biggest losses. The US has surged up.

6

22

57

#LNG

is roaring into Europe at a record clip of 390 Mcm/d, eclipsing the Nov. 2019 all-time high. Do not expect it to drop. Russian volumes are thin & Norwegian volumes finicky. Higher US sendout is thickening the batter with the UK & Belgium taking the biggest incremental chunks

7

28

60

Can’t ever remember a market where it was impossible to forecast the top. Trying to peg TTF prices to fundamentals at this point is useless. Still curious why it keeps spiking. If everyone largely agrees no one can afford to burn gas at this price, why does it continue to rise?

European natural gas prices extend rally toward an all-time high 📈

🥵 Hot and dry weather is rapidly drying up rivers and hampering transport of coal and oil. That's forcing utilities to use more gas

🇷🇺 Meanwhile, Russia pipeline gas flows remain weak

8

83

243

21

14

60

Been debating this with myself for a week. Should I non-gas post? Is modesty the best course? But dammit, I’m just kind of proud. Haven’t been this proud since winning the geography bee in 3rd grade at Cynwyd Elementary. So here we go. Number 1 at Jackson for one magical day.

8

2

58

Here’s a piece of gas demand loss that will not be returning unless the EU is willing to reintroduce Russian gas at some point. Even then it still may not make sense. Fertilizer production will chase low cost gas. Not hard to see where it will be migrating

#ONGT

@ColumbiaUEnergy

At least 50 fertilizer production facilities have closed in Europe. This is stated in a report by Mitsubishi UFJ Financial Group (a major financial group among the world's top ten).

Fertilizer production in the EU has become completely unprofitable due to gas prices. 75% of the

189

1K

3K

8

28

58

Here's the core strength of the

#LNG

spot market in 2024: Asia pulling in more LNG from other regions to meet demand growth, even as Asian production has grown slightly. Sellers from US, Qatar, and Nigeria are cashing in with most of the incremental volume.

#ONGT

@ColumbiaUEnergy

4

26

59

Power demand in Europe remains below sea level, which is why lower nuclear output is not more of an issue this summer. Gas burn is also relatively low thanks to a strong turnaround in hydro availability and use.

6

20

58

Every energy analyst I've known made their reputation on understanding supply and every energy analyst I've known risks their reputation by not understanding demand. Me included. It's the primary hazard of the business. Easy to count barrels. Hard to count how they're used.

12

10

53

Every time I read or write about the Saudis still direct crude burning for power generation in a country with the world’s 5th largest gas reserves, it makes me rethink the possibility of the same country building and leading a world class ammonia and hydrogen business.

(Remember that we are getting into the summer season, and Saudi Arabia will have fewer barrels to export as oil domestic demand swings as much as 1m b/d due to direct crude burn in power stations to meet the surge in electricity for air conditioning)

#OOTT

7

42

221

7

13

56

This paper by my

@ColumbiaUEnergy

colleagues deserves much more attention. The world is sleeping on Russia’s emerging

#LNG

strategy, which may drive other LNG producers to drink if they understand the implications. Do not read at your own risk.

#ONGT

5

21

57

Unless a late cold snap emerges, net injection season in Europe started at its 2nd earliest point in a decade in 2023. Gas storage is already at an all-time high for March. Stocks can be full by Nov. 1 at 68% of normal injections. At 100%, stocks will be full by Aug. 4.

#ONGT

5

20

54

Bad news for

#LNG

sellers, as it could undermine the story that China will outbid Europe for more LNG in Q2/Q3. Rumor always was that this gas was priced at 10% Brent. If so that would be a bargain these days. Maybe Xi said that they can pay a little more for extra volumes.

12

16

55

Rule number 6 in

#LNG

markets: when India & Pakistan see an uptick in Qatari volumes, it means Qatar is having trouble selling it elsewhere in Asia. These countries only buy more at a lower price. Not uncommon for spring, mind you, but still telling regarding Asian demand.

#ONGT

Uptick in Qatari LNG contributes to higher LNG imports in India, Pakistan in April: GECF

1

1

6

5

14

54

The great European gas storage refill has received plenty of assistance from South America. While Argentine, Chilean, and Colombian

#LNG

imports are slightly up this year, Brazilian

#LNG

demand has cratered due to extreme high hydro availability.

#ONGT

@ColumbiaUEnergy

6

18

54

European industrial gas demand has been dropping since Q3-21, although the total impact has been limited by cost hedging thus far. As more hedges roll off, additional bites will be taken out of industrial gas demand, which accounts for ≈30% of total annual gas demand.

#ONGT

5

19

54

Look at the growth in 2019; up 8 Bcf/d in 12 months when HH went down from $3.11 to $2.22. Now we are down by 6 Bcf/d from April to May, when HH went from $1.75 to $1.75. What’s the warning? If oil prices don’t move a little higher, gas prices are going to move a lot higher.

4

24

53

A brutal drop off in Japanese imports in May helped fuel the decline in JKM prices. Mind you, lower Japanese imports are not a surprise. It's been in the works for some time. LNG under contract will fall by 20 Mcm/d in 2023. This drop also corresponds with more nuclear.

#ONGT

1

30

54

This move almost convinces me that Berkshire Hathaway has convinced itself they can unlock additional

#LNG

exports using Marcellus/Utica gas. My experience with them is that they are logistical wizards and they see an opportunity here to unleash a massive de-bottleneck.

#ONGT

.

Berkshire Hathaway has agreed to buy Dominion Energy's remaining stake in the Cove Point LNG terminal in Maryland in a deal valued at $3.3 billion. Berkshire will now own 75% of the facility. Brookfield Infrastructure Partners owns the other 25%.

0

5

30

8

11

54

Europe prevented a return of coal in Europe by igniting one in Asia. Not a judgment; an observation. Acceleration of energy transition in Europe may lead to a deceleration in Asia if LNG producers cannot price gas low enough to entice change. Cheap coal is a tough habit to kick.

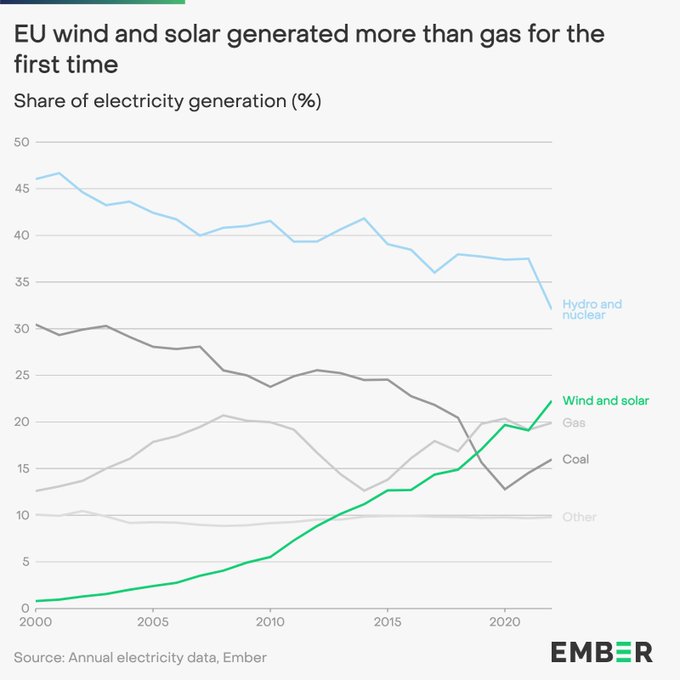

BREAKING⚡️🇪🇺

#Solar

&

#Wind

generated a record 1/5 of EU electricity in 2022, for the first time overtaking fossil gas.

Despite the

#gascrisis

and record lows in hydro and nuclear, Europe prevented a threatened return to coal power.

#EER2023

38

256

564

4

15

54

So glad you researched this point. It’s been bugging me this whole time. It helps explain some of the gas demand inelasticity we’re experiencing despite higher prices. So difficult to gauge if energy is under, over, or properly priced, given how its role in society has changed.

In the 1950s and 1960s, energy was 7 percent of U.S. personal consumption expenditures. This is known as the era of "cheap oil" which supposedly fueled economic growth. Now we hover between 3 and 4 percent, and people think economic collapse is imminent if oil prices go up...

8

102

228

2

21

51

Lack of European gas demand or strength of Asia

#LNG

demand? Take your pick. Europe is just not interested in buying LNG these days. Ample storage is not helping, though Norway's maintenance-related production cuts in September should turn things around.

#ONGT

@ColumbiaUEnergy

4

23

52

NBP is getting absolutely throttled due to too much LNG pushing into the UK, too little UK storage to fill, & not enough export pipeline availability to release pressure. Even Norwegian flows won't budge. UK gas production (remember that?) is also up & the spread is now $20.

#ONGT

8

22

53

Worth repeating. This speech, made yesterday at

@ColumbiaUEnergy

’s epic

#globalenergysummit

, was important and somewhat groundbreaking in the evolution of US energy policy. Please take the time to read it. Trade and energy transition.

#ONGT

10

16

53

Anyone have 106 Bcf/d by end 2023 in their forecast? Now's the time to show it; I want your call to be recognized. Production in November is up by 3.9 Bcf/d Y/Y, even though the rig count is down by 164. Shale producers and their productivity leaps never cease to amaze me.

#ONGT

13

17

52