Willie Delwiche, CMT, CFA

@WillieDelwiche

Followers

21,967

Following

291

Media

5,735

Statuses

22,312

@HiMountResearch founder | Teaching Econ/Finance at @insidewlc | Urban farmer & vintner All models are wrong - some are useful

Milwaukee, WI

Joined September 2013

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

The U

• 631794 Tweets

#TGS2024

• 181335 Tweets

Miami

• 97891 Tweets

Washington

• 87428 Tweets

Knicks

• 79998 Tweets

Towns

• 71153 Tweets

Minnesota

• 68952 Tweets

León

• 64720 Tweets

Randle

• 60155 Tweets

Donte

• 38449 Tweets

Wolves

• 37973 Tweets

भगत सिंह

• 36891 Tweets

The ACC

• 29197 Tweets

#DAY6INBKK2024

• 28648 Tweets

Asharamji Bapu Case

• 26409 Tweets

Equality Exploited

• 24217 Tweets

Hart

• 22829 Tweets

日本破壊クソメガネ

• 19629 Tweets

Virginia Tech

• 18445 Tweets

Cam Ward

• 18291 Tweets

Canes

• 14294 Tweets

Rutgers

• 12511 Tweets

Celtics

• 11867 Tweets

Pinned Tweet

If you are paying attention to everything, you are focusing on nothing.

5

12

118

We've never before had so few stocks outperforming the S&P 500.

31

295

1K

This is Unprecedented:

We’ve had bonds down for 3 quarters in a row in the past & we’ve had stocks down for 3 (or more) in a row.

But we have never had stocks & bonds both down in 3 consecutive quarters.

Until now.

59

289

1K

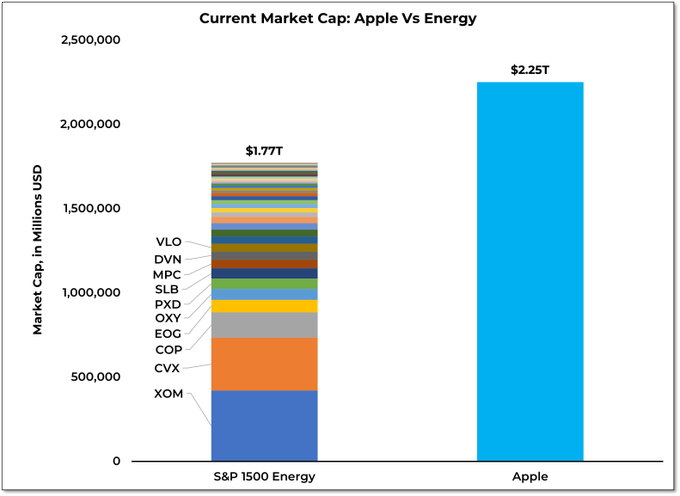

Apple has a larger market cap than all the Energy stocks in the S&P 1500 combined.

81

198

937

Marty Zweig's rules.

If you are going to quote them - know them.

Ignore them at your peril.

23

249

903

Investors are fighting the trend: $ARKK is down 60% YTD and has seen net inflows of $1 billion. $XLE is up 40% YTD and has had net outflows.

44

132

685

Stocks have been despised all year and yet remain historically over-owned.

If past is prologue, that's a recipe for a secular bear market and a lost decade of equity market returns.

37

151

639

CBOE equity put/call ratio had never before been above 1.5.

Yesterday it was above 2.0.

40

133

528

Bull markets: “It’s a great stock”

Bear markets: “It’s a great company”

16

58

507

Cash is running 12% ahead of $SPX so far this year.

29

32

501

If all I had were market indicators, I’d probably be leveraged long.

If all I had were macro indicators, I’d be net short.

34

36

449

Biggest mistake being made right now is assuming the bull market is still intact.

57

36

383

There is a yawning chasm between what people are saying & what they are doing.

29

68

396

It's never not been a recession when the Philly Fed Index has been as low as it is right now.

32

107

380

When equity market sentiment got washed out in 1990, 2003 and 2008, stock exposure approached 40% from above and cash exposure approached 40% from below.

16

95

372

Investors might be bearish, but they still haven't done much about it.

Positioning matters more than sentiment.

11

73

338

Last week's breadth thrust decreases the odds of this continuing, but recent $SPX price action remains eerily consistent with 2007-09.

19

68

299

2022 is not 2008 - but you might not realize that just by looking at the price action.

18

71

298

We have a Risk On backdrop for the first time in a year.

21

62

288

A pullback is when your neighbor's portfolio is down 20%.

A bear market is when yours is down 20%.

3

29

281

Bull markets take you to levels you never thought you would see.

Bear markets take you to levels you never thought you would see again.

1

61

266

55 days in a row (and counting) of more new lows than new highs.

That is not bull market behavior.

8

61

257

This year:

If you bought S&P 500 when VIX closed above 28.5 and sold when it dropped below 28.5, you'd be up 13% YTD.

If you bought when it dropped below 28.5 and sold after it closed above 28.5, you'd be down 30% YTD.

8

60

258

Just over 55% of $SPX closed at new 20-day highs yesterday.

That triggers a breadth thrust in our work - the first since June 2020.

12

64

227

71 days in a row of more new lows than new highs on NASDAQ.

Matches the Dec 2008 peak with a chance for the record tomorrow.

5

52

230

This one surprised me:

Even for the Magnificent Seven it's been two years with no progress.

17

44

219

A little more on yesterday's spike in NASDAQ new lows:

20+ years of daily data and we've never seen more stocks making new 52-week lows on the same day that the NASDAQ Composite was making a new 52-week high.

9

56

213

Decentralization was supposed to make things more transparent not more opaque.

FTX Corporate Structure - AKA the world's greatest shell game. Nothing to hide.

334

1K

4K

21

42

194

Previous instances over past 40+ years when % of $SPX stocks at 20-day highs exceeded 55%.

Nothing's certain (see 2002), but odds of further upside seem to be improving.

7

54

189

NASDAQ getting headlines for its YTD gains.

Beneath the surface, it's more new lows than new highs as breadth deteriorates.

9

46

187

Stocks don't usually suffer after persistent pessimism fades.

5

45

186

For evidence that a bear market is over, I want to see:

1. New lows contract

2. New highs expand

AND

3. New highs > new lows

So far we're seeing a lot of 1, a little of 2, but none of 3.

12

33

181

Since 2000, the VIX has closed above 28.5 just 12% of the time.

But when the VIX has been that high, the S&P 500 has produced an annualized return of greater than 40% (vs an annualized return of less than 1% when the VIX has been below 28.5).

Fade fear.

0

35

171

Buying panic among NAAIM members: median exposure (up to 45% from 1.25%) posted second largest weekly increase in history of survey.

10

38

162

34 weeks in a row of more stocks making new lows than new highs.

5

29

160

NDR Trading Sentiment Composite is at its lowest level since late-2022.

When short-term sentiment is this washed out, stocks usually rip.

7

46

162

Currently at 6 days in a row of more decliners than advancers on the S&P 500. That's the longest streak this year and tied for the longest since Dec 2018.

12

37

150

When new lows > new highs, talk of a new bull market is premature and expecting price bounces to persist is defying history.

13

35

151

Momentum thrusts without breadth thrusts can point to exhaustion.

But when seen with breadth thrusts, they've led to rallies that haven't looked back.

7

25

153

In taking out its 2018 high, 10-year T-Note yield has surpassed the previous cycle peak for the first time in 40+ years.

6

45

147

NASDAQ Composite ekes out a new high on the same day that NASDAQ new low list reaches highest level since March 2020.

8

30

139

2022 is looking awfully similar to 2008 in terms of the relationship between volatility and strength (or the lack there of).

4

39

142

Plot thickens as II bull-bear spread collapses. Getting close to bears > bulls on this survey.

4

36

141

Commodities have joined stocks and bonds in down trends.

Stage VI of Martin Pring's cycle.

Next is back to Stage I, when bonds turn higher.

5

36

137

Half of issues on NYSE+NASDAQ made new 52-week lows last week.

If that was exhaustive, then we should soon see the new low list collapse and end the 25 week run of new lows > new highs.

3

29

133

We are in the midst of the longest stretch of consecutive days of more new lows than new highs since the 2008/09 financial crisis.

6

36

130

1000 more stocks made new lows than made new highs yesterday.

Yet the pundits keep talking about "Year 2 of a Bull Market"

12

39

129

2022 is again the worst start in past quarter century for 60/40 portfolio.

7

38

128

50 years of trade offs between strength & volatility.

Only years comparable to 2022 are 2008 & 1974.

6

46

126

AAII bears jumped to highest level since Mar 2009 and are above 60% for only the 4th time in the history of the survey.

8

33

125

Energy sector: up 50% YTD.

Impact on S&P 500: negligible.

6

19

125

Dec 2018 looks like a cyclical low, meaning we are only a year or so into the current bull market. Mythbusting courtesy of

@Todd_Sohn

via yesterday's

@CMTAssociation

webinar.

5

40

120

For all the talk about rampant pessimism, retail still loves stocks.

Household equity exposure remained above its long-term average all of last year and has increased over the past two months.

12

37

125

S&P 500 being up 15% or more in 40 days tends to lead to more gains.

Strength begets strength.

7

32

121

A correction is when your neighbor is down 20% in the market. A bear market is when you're down 20%.

2

17

123

All the net gains for S&P 500 since 2000 have come with VIX > 28.5.

That leaves you with 87% of your time to go fishing.

7

21

121

It is hard (for me at least) to look at this fund flow data and conclude that there was not at least some degree of panic that occurred in December - Equity funds had outflows of nearly $100 billion over the past four weeks.

5

62

117

Payrolls & unemployment rates don't tell much about where the economy is headed.

Average weekly hours are the only part of today's employment report considered a leading indicator.

Decline there has accelerated in recent months.

Not looking very soft landing-ish.

4

28

118

AAII bears drop below 20% for the first time in 2.5 years and are at their lowest level since early 2018.

9

44

122

New highs > new lows for the first time this year.

2

38

122

Sentiment on gold has completely reversed from where it was this summer (when gold was hitting new all time highs). Pessimism at its most extreme since Aug 2018 (when gold was at $1200/oz). $GLD

10

33

115

Amazing how many things that made some sense at 0% rates make no sense at 4% rates.

Almost as if the cost of capital is an important input.

5

12

118

After today, NASDAQ Composite is ~6% of its peak. More than 2/3 of its stocks are at least 20% below their highs and nearly 40% have been cut in half.

9

32

118

The last time we had more new highs than lows on a weekly basis was 11/19/21. That was 700 $SPX points (17%) ago.

4

21

115

Plenty of focus on Emerging Markets ($EEM) finally surpassing the 2007 peak last week. Think its equally important to look at it relative to S&P 500 ($SPY) where a reversal of a decade-long downtrend appears to have only just begun.

2

40

116

Now at 29 consecutive weeks of new lows > new highs and some still stubbornly refuse to call it a bear market.

1

36

116

If it's not a recession, it's unprecedented.

16

35

114

Another spike to a new high for the CBOE equity put/call ratio.

14

28

115

48% of trading days in 2022 saw a 1% swing on the S&P 500 & 92% had new lows > new highs.

Going back 5+ decades, that was an unprecedented combination of volatility & weakness.

4

32

115

Lots of focus on the S&P 500 & it's 200-day average in recent days.

Over the past couple of decades, whether the average is rising or falling has mattered a lot more than whether the index is above or below it.

4

16

110

Based on Philly Fed new orders indexes (current and future), avoiding recession would be unprecedented.

1

32

108

We are searching for truth, but what we find is perspective.

Where you look determines what you see.

3

31

111

Everything has been down more than the S&P 500 this year.

6

16

108

50% of days in 2022 have had the S&P 500 move +/-1% or more.

Fewer than 10% of days have seen new highs > new lows.

Strength & volatility tend to be inversely correlated over time.

When market trend turns higher, it should be volatility down and strength up.

7

20

109

If the patterns of history hold, we are likely to see a bull market in bonds before we see a bull market in stocks.

Right now, it's persistent downtrends in bonds, stocks and commodities.

4

27

108

Today was the 8th day in a row with new lows > new highs and the S&P 500 moving less than 1%. That’s the longest stretch since 2018 and fifth longest in the past quarter century.

Persistently quiet weakness is a market anomaly.

2

32

109

If you're looking for market rallies to be sustained while more stocks are making new lows than new highs (which is currently the case), you’re fighting the tape.

12

21

109

NYSE+NASDAQ last week:

more stocks were down than up & more made new lows than new highs.

If it’s a bull market, it’s a weird one.

8

26

109

No need to overthink or overreact to specific $SPX levels.

We continue to see new highs > new lows (27 days in a row is longest stretch since mid-2021) and that is bull market behavior.

12

21

107

Friday's 9-to-1 up day was followed by a 14-to-1 up day yesterday.

Argues that downside momentum has been broken and puts our bull market re-birth checklist now at 1 out of 5.

7

26

106

Finishing the week with VIX < 28.5 and net new high A/D line still falling.

That leaves our VIX-Breadth Tactical Model with a negative reading.

Since 1990 that has been case 25% of the time, during which the S&P 500 has lost 40% of its value.

6

27

106

More bear markets end in October than in any other month.

Most bear markets do not end in October.

10

12

103

Bond yield breakout has been a global phenomenon.

1

40

102

Ford - Tesla relationship at an interesting juncture that goes beyond just suburbanite truck preferences. (chart courtesy of

@sstrazza

) $F $TSLA

8

26

100

We are coming out of the most protracted period of pessimism in the history of the AAII survey.

When persistent pessimism has faded in the past, it's usually been good news for stocks.

6

35

106

Do stocks typically rally this time of year (especially heading into mid-term elections)? Yeah.

Does everybody already know this? Also yeah.

10

27

105

We’re at 7 days in a row without a 1% swing in the S&P 500 - that matches the longest such stretch we’ve seen since Nov 2021.

Bear markets are characterized by day-to-day price volatility. Bull markets are characterized by extended periods of relative calm.

6

17

103

Coming into this week, our "bull market re-born" checklist was still 0/5.

Haven't seen anything yet this week that would change that.

5

30

100

Plenty of wailing and gnashing of teeth over weakness in tech land this week, meanwhile 75% of stocks in Financials sector hit new 52-week highs - the most in at least a decade.

4

14

101

It gets dismissed because it doesn't fit with the narrative, but new lows > new highs (13 weeks and counting) is not typically consistent with bull market behavior.

8

20

102

99% of industry groups are above their 10-week average.

Last three times this happened:

Nov 2020

Jun 2020

Mar 2019

8

21

104

Over at the NASDAQ:

-95% of the trading days in the past 3 months have seen more new lows than new highs.

-Nearly half (45%) of stocks in the composite have been cut in half.

-$NDX is 15% below its Nov peak.

Can't we stop pretending & just call it a bear market at this point.

6

18

99

New highs > new lows last week for first time since August and only 3rd time since Nov 2021.

4

26

100

Don't mean to ruffle feathers with everyone gawking at where stocks & indexes are relative to 200-day averages, but here is a contrarian view of breadth:

Over the past three years nearly all net gains in $SPX have come when fewer than 61% of stocks were > 200-d avg.

5

28

101

NAAIM exposure index increased to 57% this week. That's not fear. Stocks usually don't find a bottom until NAAIM is at or below 30%.

6

20

100

"Full Capitulation" back to Oct'08 levels means just 30% more downside for $SPX.

6

26

98