Peter Conti-Brown

@PeterContiBrown

Followers

7,688

Following

377

Media

131

Statuses

7,899

Class of 1965 Assoc Prof of Financial Regulation @Wharton , financial historian, #finreg , Nonres Fellow @BrookingsInst . I blog at

Philadelphia, PA

Joined May 2012

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

#LISAxVictoriasSecret

• 955104 Tweets

#VSFashionShow

• 626037 Tweets

Messi

• 310203 Tweets

Argentina

• 270357 Tweets

Adriana Lima

• 198804 Tweets

Chile

• 193392 Tweets

Allred

• 152420 Tweets

Ted Cruz

• 149203 Tweets

gigi

• 131230 Tweets

bella hadid

• 128962 Tweets

Tyla

• 91337 Tweets

Bolivia

• 84993 Tweets

Yankees

• 83454 Tweets

Julián

• 58935 Tweets

kate moss

• 55290 Tweets

Paraguay

• 48187 Tweets

Cher

• 47724 Tweets

Uruguay

• 46525 Tweets

Candice

• 42014 Tweets

Tyra

• 32733 Tweets

Jazz

• 32274 Tweets

ميسي

• 20364 Tweets

#DWTS

• 19278 Tweets

Andreas

• 17097 Tweets

#RepBX

• 16443 Tweets

ALL RISE

• 16260 Tweets

Luiz Henrique

• 15147 Tweets

Nico Paz

• 14848 Tweets

Aaron Judge

• 14238 Tweets

#RoçaAFazenda

• 13893 Tweets

शरद पूर्णिमा

• 11514 Tweets

Raphinha

• 11256 Tweets

Rodrygo

• 10399 Tweets

Machis

• 10388 Tweets

Last Seen Profiles

So when SBF told

@TheStalwart

@tracyalloway

and

@matt_levine

that he was effectively running a Ponzi scheme we should have taken him literally and seriously.

26

61

826

To be fair, I have some bad hambre right now but immigrants and their food trucks are the cure for that hambre. Unless he meant hombres?

7

268

734

Your regular reminder that things have always been weird

32

102

518

Delighted to receive tenure

@Wharton

& to be the first holder of an endowed chair in financial regulation. Wharton is building on a big commitment to finance & public policy—more details to come!

Also, a thread on what I really think of all of you now that the gloves are off /1

62

9

461

On the recent survey suggesting that Latter-day Saints are the only universally despised religious minority, some anecdotes from the academy for why that resonated so much for this Mormon /1

52

60

357

Historians of the Great Depression write about the “false dawns” that gripped the public in 1930-1932.

Can’t shake the sense that we are currently in an economic false dawn.

10

64

289

Very good analysis from

@IrvingSwisher

on why Mnuchin's move here violates the CARES Act and could be corrected by the Biden Administration promptly. /1

*MNUCHIN TO PLACE $455 BLN UNSPENT CARES MONEY IN GENERAL FUND ... *TREASURY NEEDS CONGRESSIONAL APPROVAL TO USE GENERAL-FUND MONEY

Transferring to the general fund before Jan 1, 2026 would be in violation of the CARES Act

140

2K

6K

5

96

268

In 2004 I was a low income student at Harvard. Larry Summers had just made school free for us. I was hired to run recruitment. We used low-income zip codes cross tabbed with high test scores and ended up recruiting a massive number of…the highest income kids in these places.

12

25

261

“Bailout” is a pejorative term with no clear conceptual meaning (never mind that it has no legal meaning at all).

But if bailout means government elimination of downside after private capture of upside then, yes, uninsured SVB depositors were bailed out.

@Noahpinion

I disagree. It's a bailout. "Taxpayer funded" is a canard. And also Treasury is putting up $25 billion to backstop the creation of the new Bank Term Funding Program.

So if fiscal authority is the determinant, then that still applies here.

51

67

834

12

52

254

I want to push back on the idea that shareholders, bondholders, and management were “wiped out” in this. /1

7

55

213

Fellow Econ historians: can you recall anything like this outside of a financial panic?

@SeanVanatta

@rauchway

@csissoko

@bindersab

@Undercoverhist

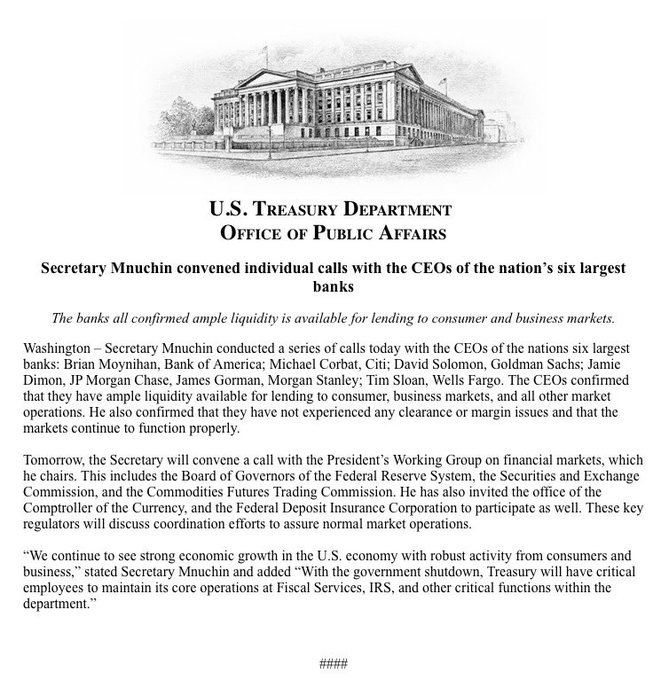

Today I convened individual calls with the CEOs of the nation's six largest banks. See attached statement.

5K

2K

5K

14

70

190

This invocation of 13(3) is an implicit rebuke to supervision and regulation of SVB and beyond.

This move is a big intellectual victory for those who see money as sovereign and banking as an infrastructural public good. Read

@MorganRicks1

@STOmarova

for the best of these. /1

6

45

165

A thread on the chaos and futility that will occur if Trump attempts to fire Powell, building on this oped from earlier this month. /1

14

112

159

I remember reading my first Isaac Chotiner Q&A and thinking that if he ever asked me to be the subject I would gather my family, tell them I had made some life mistakes, and announce that we were leaving the country.

Well, it went better than I feared:

6

18

167

Someone added the entire Penn faculty to a shared document.

The fusillade of reply-alls (1) insisting on removal, (2) expressing confusion, or (3) lambasting the others for reply alls while replying all is the funniest email thread I’ve read in a long while, can’t get enough

11

6

159

I like this but let’s go further. Why do we have “private” “boards of directors” for what should probably be considered the branch offices of our central bank?

It’s like saying the managing partners at Big Law firms get to have a role in overseeing federal judges.

One of the most absurd aspects of the Silicon Valley bank failure is that its CEO was a director of the same body in charge of regulating it: the San Francisco Fed. I'll be introducing a bill to end this conflict of interest by banning big bank CEOs from serving on Fed boards.

1K

4K

24K

15

32

152

The brrrr is the fan kicking on to keep the hard drive from overheating

Fed Chair Powell says the central bank creates money digitally.

In other words, the money printer doesn’t actually go brrr.

48

60

551

5

11

155

I think even

@MorganRicks1

and the other sovereign money/public banking folks will blanch at this.

It’s a breathtaking guarantee a single weekend into a crisis when banks have not paid for such insurance and have not been subject to supervision consistent with such commitments.

The Fed says its new lending facility is big enough to cover all US uninsured deposits and that it is "prepared to address any liquidity pressures that may arise"

@FinancialTimes

13

22

58

5

39

148

My sister, a nurse who has been beyond exhausted during Covid, sent me the attached texts and I have nothing I can tell her since I think this was either an overreaction (and thus a policy failure) or suggests a broken banking system (which, again, a policy failure).

9

17

149

I really don’t buy this argument that depositors with seven- and eight- and nine-figure accounts at these banks can’t be good monitors. On that theory there can be no consumer monitoring, corporate governance, or good grief democracy itself. /1

P.S. I'm not particularly worried about moral hazard. The CEO, management & Board all losing their jobs. Equity going to zero. Bondholders won't be paid in full. These are all the entities that can effectively monitor, is unrealistic to expect depositors to do much monitoring.

75

74

606

10

28

142

I have finally read

@jeannasmialek

's book Limitless on the Fed. It is probably my favorite book of central bank journalism I have ever read.

What Jeanna does so well is nail the need neither to praise the Fed nor to bury it, but to assess it and its extraordinary powers. /1

5

10

146

I’m decreasingly sure we need crypto legislation & increasingly sure the proposals under discussion are bad.

Better to regulate securities as securities, exchanges as exchanges, and banks as banks.

How much crypto activity would go away if de facto became de jure? 90%? 95%?

15

23

140

Having fun with some 1970s Fed history today and enjoyed learning that Arthur Burns in 1977 sent the just-inaugurated Jimmy Carter an unsolicited memo on how to fight inflation, with 20 points, and did not mention monetary policy once.

7

23

138

I share this for (1) non LDS who wonder about this dynamic, (2) solidarity for academic Mormons who live it, & (3) some further solidarity for people whose identitarian commitments make them feel like they aren’t taken seriously as individuals.

Now, back to banking Twitter /end

3

4

136

Shareholders and managers especially had a stellar run through privatized upsides all along the way. There’s a substantial amount of cold hard cash that these individuals have pocketed (which will stay in their pockets) because of this asymmetry. /3

2

20

132

Today I asked a group of journalists 2 questions:

1. How many of you have had conversations about the ways AI will change your jobs in 2023?

All hands went up.

2. How many of you have ever used crypto to solve problems that ordinary banks could not solve?

No hands went up

19

18

124

Point is that a system of such asymmetries rewards so many at public cost - and that includes the other stakeholders who are today “wiped out” (but still get to keep their gains from the good years). /end

6

14

120

If I were a member of the FOMC, I would vote to pause.

I know the Fed is worried about its credibility as an inflation fighter.

I’m worried about its credibility as a crisis fighter and bank supervisor.

That credibility is lower than any time I can remember.

9

24

113

Delighted to announce the launch of the

@Wharton

Initiative on Financial Policy and Regulation that I will co-direct with my colleague Itay Goldstein. More details below and much more to come.

9

10

116

These ten individuals/organizations received a taxpayer bailout.

Now that that’s established, we can debate why the government felt the need to give it to them.

Gruenberg: The ten largest deposit accounts at SVB held $13.3 billion in the aggregate.

40

126

494

8

32

109

I don’t think it is fair for Democrats (including me) to expect R central bank nominees to have the same worldview as us.

But it is not too much to demand explanation for harsh critiques of accommodation 2009-2016 followed by harsh critiques of normalization 2017-present. /1

Zero rates? hmmmm. September 2016 "The Fed has adopted monetary policy decisions that channel low-cost funding to wealthy investors and corporate borrowers at the expense of people with ordinary bank savings accounts and retirees on fixed-income pensions."

6

4

18

4

24

103

I don’t like the proposal to guarantee all bank deposits without limit. I explain why in a guest essay in today’s

@nytimes

6

20

110

It’s true that the Treasury, FDIC, and Fed moves today - together and separately - will not provide *more* to these parties, but the guarantees now on tap make the bonanzas to these parties in the preceding years possible in the first place. /2

2

13

107

Pleased to announce my book, The Federal Reserve: An American History, to be published by

@LiverightPub

@wwnorton

. Especially delighted to work with

@dan_gerstle

as editor. Aiming for definitive but comprehensible &, as the subtitle suggests, integrated into US history generally

4

27

109

Remember cursive?

What a spectacular waste of time and human energy that multicentury effort turned out to be.

22

9

103

I lost a beloved friend and mentor to Covid-19 last night and feel both bitterly deprived of so much and deeply grateful for the shared humanity we enjoyed that now makes this loss so exquisite.

11

1

98

The problem with catching up on email is that people then write back to you and we're back where we started

1

6

102

Delighted to announce a new project of the Wharton Initiative on Financial Policy and Regulation:

The Business, Economic, and Financial History Project.

Link here:

/1

3

21

102

Shortly after I got tenure at a school I love that is the last job I’ll ever need or want I added “Latter-day Saint” to my Twitter profile. I’m sad at the (good) advice from people who were looking out for me. I’m ashamed of myself for taking it. /8

5

2

99

The idea that everything was going great and then some loud VCs on Twitter broke SVB is the 2023 banking crisis at its dumbest*

*I'm not even going to dignify the anti-woke idea that floated in the first few days.

8

8

85

My 12 yo son watched this and has some notes:

1. Your books are a mess.

2. You should wear a tie. Did you not know the interview was going to happen?

3. You look very pale. Very pale. Like a vampire. Did you see that too?

Trouble at a major European Bank today has injected fresh turmoil into global financial markets.

@WmBrangham

spoke with

@PeterContiBrown

about the recent turbulence in the banking sector.

0

7

17

9

4

95

This idea, that no one could ever have known that there was a deposit insurance limit, is so strange to read as a historian. The existence of the limit was the saving grace of deposit insurance, the thing that justified this dramatic expansion of public support for banks.

8

12

88

Today I made a healthy version of a Philly cheesesteak w/ lean deli meat, fresh spinach & onions/peppers grilled w/ a drizzle of olive oil, a bit of cooked brown rice, & a cottage cheese & tomato horseradish purée on top.

It tasted like absolute garbage. Never do that.

2

2

91

Addendum: for my immediate colleagues at Wharton and finreg - the people who know me personally and with whom I interact all the time, including in debate - I have had wonderful experiences where Mormonism comes up regularly but humanely. So don’t read me to overclaim here.

4

1

90

And the second-most this election

71,000,000 Legal Votes. The most EVER for a sitting President!

341K

95K

722K

2

7

87

Just finished

@JohnCarreyrou

’s masterful book on Theranos, Bad Blood, in a couple of fevered sittings. Will be assigning it next year to my Wharton MBAs

5

10

89

His fear was that people who might see quality in my work would be talked out of it and those with whom I was debating might use it against me. To be clear, my field is banking and financial regulation. Except the occasional reference to Marriner Eccles, this doesn’t come up /3

2

2

87

I don’t think I’ll ever get over the fact that the US government bailed the stablecoin industry during that fateful weekend in March 2023.

11

19

82

This is not true. It is a sweeping overhaul of 13(3) that has nothing to do with pandemics, CARES Act, or the debates of 2020. As written, it rewrites the Fed’s emergency authority for anything it might undertake that is “similar to” what happened in 2020. It should be removed.

Sen. Toomey in a statement: "The language Senate Republicans are advocating for affects a very narrow universe of lending facilities and is emphatically not a broad overhaul of the Federal Reserve’s emergency lending authority."

h/t

@JessicaASmith8

1

2

2

2

29

78

I wish the Fed had never announced this rushed investigation. Here I am at more length in the American Prospect saying why.

5

24

80

How does a central banker that “just follows the data” make a decision about rate hikes today?

It’s impossible. You need a framework/worldview to think through trade offs.

This is one reason why the scientistic epistemic model of central banking is not a useful one.

16

26

80

As I read Lewis, I see a phenomenon I’ve seen before.

Some people just crave the approbation of billionaires.

It’s a corrupting defect. I’ve seen otherwise grounded people toss away core principles in fear of offending the billionaires. /1

11

18

78

Uhhh, news has been on a wire for a lot longer than there has been a Federal Reserve.

“Tightening happens much faster now than it used to in a world where news was in newspapers, and not on a wire,” Chair Powell says.

5

4

45

6

5

77

I overheard in west Philly today a hipster grad student say “No, seriously, that’s why a projector with transparencies is so much better than PowerPoint”

I wasn’t ready for it.

5

7

78

Wild to me that we refer to US Bancorp, Truist, and PNC as "regional banks" when they each have *ten times* total assets as the SIFIs of 2010. Seems like a tic to me that journalists should expunge.

7

12

74

One of the tragedies of Covid is it’s robbery of time to honor, say goodbye, comfort. A dear friend is hospitalized, prognosis bleak, & all I can do is write a letter about all he has been to me, a letter he may never read. It is so much less than I want and than he deserves.

6

4

77

My man they’re your needles. Tell them this directly!

My strongly held view is that the needles are greatly overstating the uncertainty at this point

143

487

6K

2

3

76

I want to assign an overview of FTX for my MBA students taking business ethics from me next semester. What's the best 5-10 page overview of the scandal to date accessible to an outsider?

26

7

76

One of my most beloved mentors who has only ever wanted every good thing for me, after learning years into our relationship of my religious affiliation, told me to keep that secret before tenure. /2

3

3

75

There remains no credible alternative legal interpretation to this result, whatever Secretary Mnuchin and others have insisted to the contrary.

Congressional Research Service says it’s likely “a court would determine that [CARES] does not prohibit the Fed’s emergency-lending programs from using funds invested prior to December 31, 2020 to continue lending and purchasing assets after that date”

3

7

42

2

17

72

I continue to think the emphasis on social media in the SVB collapse is completely wrong. The new paper (link below) is interesting but doesn't dissuade me. And I think the policy stakes for this narrative are very high. Brief thread /1

6

10

73

Another time, before tenure as I was receiving visiting offers at other universities, one of my cheerleaders at one school said I should never divulge my Mormonism. Same impulse, same affection for me as a scholar, same fear that pure religious bigotry would block me /4

4

2

74

My incompletely potty-trained son just provided a metaphor for our times.

Scene: he jumps up, tears his pants off, walk-run-trips to the bathroom relieving himself copiously as he goes. Finally he collapses on his froggy potty, empty, & declares: “Whew! That was close!”

1

9

74

This kills me from the

@WSJ

. For years they have been mocking the Fed as a bunch of out-of-touch tweedy technocrats who need to stick to their knitting. Now this?

The idea of massive loans to distressed industries during a crisis is incredibly sound.

For Congress.

6

11

68

I’m curious about others’ priors.

What’s the probability that by invoking the systemic risk exception and announcing a 13(3) crisis at the $250 bn level the Fed etc created a run on regional banks rather than prevented it?

This probability, initially low, is going up

14

10

67

This from

@washingtonpost

coming out strong against unlimited guarantees for deposits, adapting the proposal from

@tphillips

and with spicy (and correct) language from

@SheilaBair2013

Unlimited deposit insurance is an idea whose time has not come.

7

11

67

Last one: a dinner at a school when I was a PhD student testing job market. Senior scholar has just seen the South Park Book of Mormon musical and raves about Mormonism’s idiocies. In a flash of courage I self identified and explained why I and so many LDS hate that musical /6

4

2

72

Look, it’s not always about a professor’s pet theories, BUT:

Fed governance is broken.

We should not have private bankers needing bailouts on the boards of their supervisors.

We should not have quasi-private central banks.

Perhaps now we can change this once and for all.

4

19

69

Another: At a conf where a BYU grad presented a good not great paper. In the after discussion out of student earshot (I was in cognito), the serious critiques came as condescension about the church and what this person must believe as LDS that made him a bad scholar /5

4

2

71

So delighted to see the news that my friend

@MehrsaBaradaran

is on a very short list for Comptroller of the Currency. She’s outstanding, one of the leading scholars in our field, passionate, expert, broad-minded, also hilarious.

/1

5

12

69

I hope we can get similar litigation against title insurers. Their global tax on real estate, mandated by state laws everywhere, is astonishing in its longevity and pointlessness

My goodness the realtors are crying. Heard another one today. Do they really think we feel sorry for them for taking 6% of the entire housing market for filling out a form??

83

45

714

7

8

70

I agree with

@MorganRicks1

’s framing here. Either we need to fix the system to make credible commitments not to bail out uninsured depositors, or we have to guarantee them all explicitly. I don’t see a third option.

@PeterContiBrown

@STOmarova

@Jeremy_Kress

@DanAwrey

@ProfKateJudge

@Aarondklein

One of the things we're learning -- to the extent we didn't already know it -- is that there is a pretty large implicit guarantee behind uninsured deposits, at least at non-small banks. So we seem to have this problem either way.

1

5

19

12

11

69

I think it inelegant at best and outrageous at worst that the Fed is using 13(3) for bank liquidity. A reminder that the stigma associated with the Discount Window is a silly policy choice. The DW is so vastly superior for emergent bank lending to 13(3)

5

13

68

Astonishing to me how much energy I expend each day keeping the 1 year old alive.

Not saying he’s not worth it. Just saying he’s not good at self-preservation.

3

1

67

He spent the rest of the dinner explaining my religion to me and insisting that I missed the entire point, that it was a celebration of our idiocies and that I was too thin skinned. /7

1

2

67

Depositors don’t promote discipline because they have been trained to be undisciplined. This is a policy choice. We can choose a better system with better creditor monitoring if we want. We decided against that today. /end

3

10

67

“Taxpayer money” has about as much analytical content in it as “bailout”.

My view is there’s money managed by the public sector and money managed by the private sector. Seigniorage and DIF are public.

So this was a public bailout.

4

7

65

What is so frustrating with the pushback from the administration and others on “bailouts” isn’t about SVB necessarily is the fact that this is a bailout of the other banks that should have failed this week because they were poorly run. /1

Bailout is one of the words where, though it can obviously be fairly applied here, is so broad as to not be very illuminating.

When we talked about bank bailouts in 2008, those moves prevented banks from failing. Here, the two banks in question are still dead.

6

1

15

2

22

65

Look, delighted the circus catastrophe gets postponed, so I’m not cherry picking here.

But I genuinely don’t understand R desires to increase tax evasion. Free money from criminals! And not a little!

Summary of deal as I understand it:

— Debt ceiling raised 2 years

— Domestic programs frozen next year, up 1% ‘25. Inflation-adjusted cut

— Boosts defense, VA $

— Some tightening of work requirements on TANF, SNAP

— Energy permitting (details tbd)

— Claw back some new IRS $

385

1K

4K

11

8

61

When you read that Treasury officials said that they had identified several banks similarly situated to SVB and Signature then you can be sure that this was indeed a bailout of managers, shareholders, and bondholders…of those other banks.

3

14

63

The court issued an order (below) canceling the trial re the Fed's management of access to a Master Account (disclosure: I was an expert retained by plaintiffs on the history of the legislation that governs the case).

I think this means the Fed is about to lose, as it should

5

13

60

The TreasuryDirect website is, in a word, awful.

Why is this? It has implications for banking stability. Seems like we could get this to a better state of play with minimal cost?

13

4

63

My sixth grade son, who adores

@planetmoney

, saw my copy of

@jacobgoldstein

's new book and told me that I had 48 hours to complete it to verify that it is appropriate for him and if I did not he would read it anyway and reach his own conclusions.

4

3

63

This (and the WSJ editorial that blamed

@STOmarova

for being born in the wrong place at the wrong time) is an embarrassment for those who fixate on it. Saule is one of the most accomplished finreg scholars, one of the true leaders of our field, with unparalleled expertise /1

GOP’s

@SenToomey

is asking Biden nominee

@STOmarova

to give the Senate Banking Committee a copy of her thesis, “Karl Marx’s Economic Analysis and the Theory of Revolution in The Capital,” which she wrote while studying at Moscow State University in late 1980s.

22

17

77

3

18

58

I have many thoughts on the Fed’s actions but will say for now that the quality of Fed journalism is simply exquisite. It has been good for decades but we really are in a golden era. (I have read thousands of articles throughout Fed history and feel confident in this conclusion)

4

3

60

Payments news of the week:

Delta’s 8k reports that HALF of the airlines profits come from its partnership with AmEx.

Delta is half airline and half payments company.

My mind still hasn’t recovered.

3

16

59

Should the Fed use emergency powers to lend to some industries but not others? Let's read the statute to check legality (TL; DR: it's legal), & then turn to what this means for the Fed's relationship w/ Congress & the appropriate division between monetary and fiscal policy. 1/x

5

23

54

And it would represent a governance crisis that would damage the Fed, damage the presidency, and damage the nation. Let’s hope Trump’s impetuous narcissism doesn’t take us here. /7

5

12

52

Banks are right to resent the soaring costs of the FDIC’s bailouts of uninsured depositors like Roku and Circle. It’s really an extraordinary trade those businesses made, leaving the bloated bill for others to pay.

6

14

57

Here’s the survey:

A fascinating (and kind of hilarious) finding in this Pew survey: Mormons are among the least popular religious groups in America. They are also the only group that expresses a net favorable opinion of *every other group,* including Muslims and atheists.

165

360

2K

12

2

58

When people nail EST vs EDT in emails I just bow to them in their superior cognition and temporal awareness.

I started writing ET years ago because I often have to struggle to remember which year it is, let alone where I am relative to daylight savings.

6

0

58

Listen, constitutional and criminal law people, we banking folk only rarely dominate a news cycle.

You do it all the time.

Give us a few more days - we’re really close to getting to the bottom of this.

3

2

56

Labor of love with my sensational co-author

@SeanVanatta

- our history of bank supervision is now forthcoming (peer review pending)

The Bankers Thumb: A History of Bank Supervision in America, 1789-1980 is in to the press, and (soon) off for review.

High Five

@PeterContiBrown

!

1

5

60

3

6

56

My wife and I once randomly ran into her ex-boyfriend at a restaurant and it was less awkward than I expect this will be

Powell and Mnuchin are scheduled to testify together before the Senate Banking Committee on Dec. 1 on the Cares Act lending programs

1

15

36

2

5

52

Bondholders are a bit different, its perfectly plausible to imagine how SVB’s bondholders monetized the bonanza - I’d just want to see some more specifics before drawing that firm conclusion. /4

1

3

54

This isn’t just a low-stakes, high-brow intellectual debate (though it is that). It’s a pretty central set of commitments for our political economy. I see profound downside risks to the path we are taking here. /end

2

6

55

It's not the bad prediction that bothers me. It's the failure to reflect on the ideology that made the bad prediction

John Taylor, 2010: "We've got a high inflation down the road for sure..we're going to have inflation like back in the 1970s, or even more."

5

55

80

7

29

52

As I noted, the law isn’t clear. Trump can probably de-designate a Fed Governor as Board Chair, but not fire the Governor. That would violate a deeply held norm in Fed governance, but then, norms and Trump aren’t fast friends. /2

3

7

49