🇱 🇦 🇲 🇵 🇸

@Nick_Lamparelli

Followers

2,645

Following

5,006

Media

809

Statuses

9,313

practicing gratitude…manifesting abundance

Florida, USA

Joined February 2013

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

MOONLIT FLOOR OUT NOW

• 262478 Tweets

JUMP

• 209784 Tweets

Mets

• 163607 Tweets

Falcons

• 66985 Tweets

Baker

• 64425 Tweets

天使の日

• 50895 Tweets

Pete Alonso

• 47049 Tweets

Diana

• 41942 Tweets

Bucs

• 27873 Tweets

Kirk Cousins

• 27492 Tweets

#PowerGhost

• 24940 Tweets

Bijan

• 21801 Tweets

Mooney

• 17983 Tweets

HAVE A SAFE FLIGHT JIN

• 16792 Tweets

Hayırlı Cumalar

• 16229 Tweets

ワートリ

• 15554 Tweets

#PowerBook2Ghost

• 14552 Tweets

Tariq

• 14094 Tweets

感謝マルチガチャ

• 13920 Tweets

Cane

• 13295 Tweets

Bleed

• 11622 Tweets

PRABOWOsiapkan YangTERBAIK

• 11411 Tweets

最大4体ゲット

• 11045 Tweets

人達同士

• 11007 Tweets

KEKUATANkita PERSATUANkita

• 10838 Tweets

Hodge

• 10268 Tweets

Bielsa

• 10053 Tweets

@TheBigDamnHero

@BadSportsRefs

exactly 1 person in the world doubts that Edelman caught that...you

0

1

171

@secondfret

Sports provides such a wonderful framework for business. Overlap is not 100%. Be a michael Jordan internally. Be a Michael Jordan in how your company aggressively competes in the market.

Inside your company...be a Phil Jackson

5

3

44

The effect of big data, predictive modeling & AI will have a slow arching impact on insurance. It is NOT that these techs aren't valuable. They are! It's more about the incentives and economics of the industry. Let me explain:

4

7

36

A reminder to underwriters of risk - "A ship in harbor is safe — but that is not what ships are built for.” — John A. Shedd

Your job is NOT to strive for a 0% loss ratio. Your job is to find the sweet spot of the tolerable loss ratio, make that profitable & DRIVE down that down!

3

7

31

I am pleased to be able to speak about the future of insurance and technology at the Athenium Analytics event on 10/22. Come say hi!

Speaker announcement!

@Nick_Lamparelli

from

@InsNerds

is joining our 2019 IQA Conference to discuss how tech will dramatically change the future of insurance. Still haven't signed up for our 4th annual IQA event? Now's your chance:

#insurance

#insurtech

0

1

4

3

4

30

🎺🎺 Announcement 🎺🎺

I have started a new podcast called The Yellow Book Road. It is a sidehustle where I get to geek out with anyone who is bringing insights, wisdom, best practices and results to insurance. (The Yellow Book refers to the color of the NAIC filing book)

7

1

26

This is the single biggest risk for InsurTechs. CompNies like lemonade are not

@the

role models to solve this. Most founders don’t have that level of credibility. Look for ways to gen revenue while also raising credibility.

If you start a startup that can only reach users by doing deals with big companies, the default outcome will be that you run out of money and die while waiting for them to make up their minds.

162

960

6K

5

0

24

I’ll be presenting on flood insurance in Orlando. There will be CE credits available. Let’s connect in Disney on Sept 23/24

The speaker lineup is incredible for

#In2Risk21

! Get to know your In2Risk speakers!

@Nick_Lamparelli

(

@rethoughtins

) will be presenting The Shifting Tides of Public and Private Flood Insurance. Click to view the agenda, full speaker lineup and to register:

0

0

2

3

2

24

@amytheartist

The Secret Life of Walter Mitty. The Icelandic scenes have made me fantasize about traveling there

1

1

20

This is a fantastic explanation of why typical startup growth requirements around venture funding will ultimately fail. Insurance economics are truly unlike any other industry and growth can become a cancer

#insurtech

companies growing at all costs doom their companies. The

#captiveinsurance

model mediates this significantly by providing a sandbox in which to perfect the model. Companies going public too early raise the odds of failure b/c of heightened liquidity risk.

4

6

20

2

2

21

I'm quoted...but in a critical way. As long as my name is spelled right, I'll take it

How Lemonade disrupted the insurance industry and built a multi-billion dollar business

2

4

20

The future of insurance will be about partnerships and joint ventures. How will legacy insurance companies need to think about their business models to survive and thrive. Stay tuned!

DROPPING TOMORROW! Season 2 of The

#FutureofInsurance

w/

@Nick_Lamparelli

Subscribe so you don't miss it!

#insurtech

#insurance

#video

#clip

0

0

8

0

4

21

At one point Theranos was valued at $9 Billion. Valuation is not validation!

3

2

20

Lots to unpack here:

4

6

19

#LMND

has hit Tesla mode where their cost of capital is going to go negative as investors throw money at them. Their exec team should win an award for how skillfully they are playing the markets like a fiddle. btw...this message was not powered by AI or behavioral economics

4

4

18

I don't think of myself as an insurance professional. I care about people...so much so, that I use insurance as my vehicle to protect the people I care about! That's my mission.

0

2

18

If you are a carrier, deciding on your back-to-work options, 1 option you should consider is finding agencies where you can rent-a-desk, & provide that option for employees who want to get out of home, but don't want to commute to an office. Best of both worlds, with flexibility

1

4

18

Whenever I get that tinge of imposter syndrome bubbling up, I will remember that a whole bunch of well paid and seasoned execs thought up, vetted and then went live with CNN+, and I can move on with the rest of my day

4

1

18

Time it took to put the tree up with ornaments - ~2 hours

Time it took to find and replace the naughty bulbs - ~(seemed like) 2 days

5

0

17

Just had a pleasant conversation with

@Broker_Brett

, catching up and talking shop. One thing that emerged from that is that

#Ian

always gets put into context for capacity, but what about distribution? Welp..read on my broker friends:

1/x

1

2

14

Every 4th, I watch Saving private Ryan to remind myself how terrifying war is and what sacrifices were made on my behalf by people I will never know. The history of the world has been brutal. I give thanks that I have this opportunity to live in this country. Happy 4th 💥 🧨 🇺🇸

0

2

16

I'll be speaking about AI and technology "disruption" of insurance on 10/22 at the

@athenium

conference in Washington, DC. Come join me!

Use discount code "INSNERDS" for 20% off

0

5

15

The Latest Blog Entry From

@InsNerds

PiR E158 – Chris Paradiso, on Branding – Be You, Be Real

0

4

16

0

0

15

So I want to come back and give a quick thread on how I think insurance underwriters need to evolve into the 21st century. cc:

@ayayrongreen

@Recruit_PRS2000

1/x

5

0

15

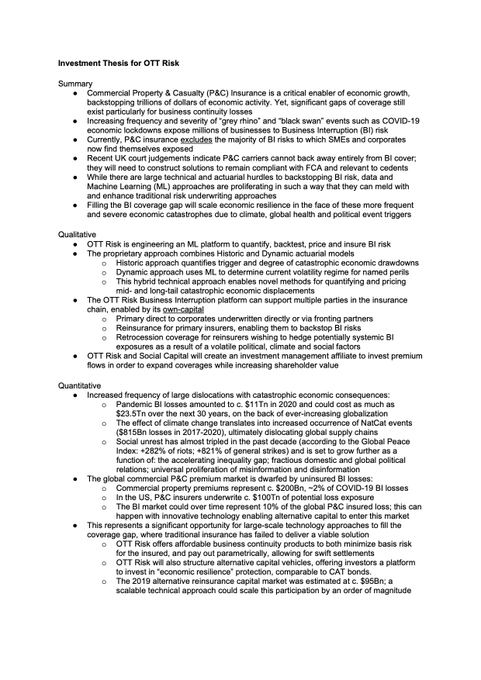

Parametric for BI is an excellent way to go. 1. don't need permission from lenders or others demanding trad indemnity. 2. can get creative with triggers and fit coverage to need better 3. should be easy to buy and easy to settle making experience better. - Wont be cheap though

Today we announce a new venture,

@ottrisk

Over the last year a few things have become clear: the world is more uncertain than ever, and the situation for small businesses is more perilous than ever.

Technology and capital can play a role in solving this problem.

222

302

4K

2

4

14

$LMND legacy incumbents can be profitable at >100 combined ratios due to their investment float. Capital lite companies will never have that benefit and will struggle just to be a low margin business

Is “combined ratio” the kryptonite for

#insurtech

?

@SpirosMargaris

@an_battista

@psb_dc

@nigelwalsh

@Nick_Lamparelli

@hedgequote

@InsuranceEleph1

@globaliqx

@robgalb

@InsurTechEd

@Xbond49

@SabineVdL

@jblefevre60

@InsuranceInside

@thepsironi

@JimMarous

1

11

30

4

2

13

Me creating a new set of insurance guidelines for reinsurers:

0

0

14

Another Florida based insurer bites the dust - AmCap to liquidate...a month ago they were an A- rated carrier

6

4

14

This is a huge story

Unprecedented.

Nationwide insurance company announces they will no longer write ANY new business in the US for the rest of 2023.

#nationwide

#nationwideinsurance

9

6

8

8

2

14

One of the big conflicts in business and financial decision making is discerning the difference between what defines an expense vs what defines an investment

6

0

12

@kevinwildes

If it wasn’t for Chris Jones and the defense, Mahomes would not have had a chance to redeem himself. The defense won that game

3

1

13

INSURANCE IS BORING? BULLSHITE! Not when The Insurance Nerdery broadcast their videos!

@AmberWuollet

takes a look at

@endofinsurance

by our good friend

@robgalb

in this episode of

#TheInsuranceNerdery

#AndIFeelFine

#GoodLuckNotGettingTheSongStuckInYourHead

1

1

2

0

3

13

The future on online events needs to be highly informative AND entertaining. Just too many distractions. I love webinars but find myself distracted by work. Make it sooo entertaining that someone like me is glued in

4

1

13

My focus when I’m trying to finish up a tweet while my wife is screaming for me to come into the kitchen to help feed the kid’s...

4

0

12

@AwardsDarwin

horrible technique. He needs to lean back hard and for gods sake, apply the rear brakes to slow the descent.

2

0

11

Fantastic thread on Hippo. As an insurance professional I feel confident in saying that $LMND can not compete with Hippo (nor Branch, Kin, Vault, Swift and others) in the homeowners space. If they can't lead in HO, then valuation is insane, which explains why I bought put options

A thread on $RTP -

@hippo_insurance

<SPAC Rumor> from Bloomberg. There are multiple threads on the company, and I wanted to give you my own experience in the space and why I am excited.

42

23

217

1

2

13

I hate to break it to you all, but not all of you deserve cheaper insurance. Many of you are horrible drivers. The total addressable market for food drivers is not that big yet somehow all these other people are also going to get cheap insurance too! How????

i’m thrilled for

@metromile

to be going public via SPAC $INAQ with

@chamath

leading the $160M PIPE alongside

@mcuban

and other leading investors. next step on what’s been a great 9 year journey. investor presentation w details:

35

20

575

0

1

12

I look to hire people who I feel can be coached and take feedback and will not hesitate to give me feedback. There may be a hierarchy but we are peers and colleagues. Should be like sports, we shouldn’t have to worry suggesting there might be a hitch in your swing

I hired 32 people and fired 10 of them.

We are growing like crazy, but I made every mistake in the book.

*Non-obvious* lessons from early hires👇

18

136

793

0

1

12

A bit past peak colors. Most of them are on the ground now.

0

0

12

Just read a news release where the marketing person for an insurance firm talked about a new relationship that would improve underwriting and hence, "the customer experience". Am I wrong if I believe that underwriting per se, isn't really about CX?

11

1

11

@bryanfalchuk

and I get deep into what the real future of insurance entails. It wont be disruption. It will be about partnerships. It will also require changes in business models. 1/x

@nick_lamparelli

"the nature of our industry is about risk sharing, so disruption won't look like it did in Tech"

Catch the full episode at

#insurancenerd

#futureofinsurance

#innovation

0

0

0

2

3

12

It is becoming obvious to me that digitization was supposed to free us from the heavy lifting of the analog world. It was supposed to make our lives easier, more effective. I coming to acknowledge that it is making life harder & complex in a way that we are not evolved to handle

3

0

12

@iancassel

there are thousands of books on how to trade but very few or no books on how to train your mind to hold on for those gains...someone should make a proper training class

2

0

11

Amazingly, this is the moment in time many insurance pros have been waiting for and yet I am seeing deer-in-the-headlights. This is your career moment, but you need to step in front of risk not sidestep it!

An “underwriting driven” hard market: Gallagher

2

1

12

Peter Thiel asks in his book, Zero to One: "Tell Me Something That's True But Nobody Agrees With"

Here is my controversial hard fact: Email is an atrocious and suboptimal communication tool for internal employees and should be barred from use. 1/x

4

2

12

@wrathofgnon

@SCP_Hughes

indoor plumbing! Imagine having to traverse 20 stories just to relieve yourself!

1

0

12

#WhatIAmListeningTo

: The Power of Geography by Tim Marshall. Incredibly fascinating.

@Itwitius

is the David Attenborough of geopolitics.

1

1

12

Mine is to travel especially for vacation. My parents were immigrants & we were so poor that except for 1 summer trip to Italy, we NEVER went on a vacation or stayed anywhere other than home & with family. Even when I stay at the HoJos @ Newark Airport, it still feels relatively

When I was a kid, I was so envious of my well off friends who had fridges with ice dispensers. We couldn't afford those nice fridges so I waited overnight for my ice trays to freeze to get ice cubes.

My dumb "made it" dream was to get one of those fridges someday. Now I finally

1K

501

9K

1

0

10

great thread on entrepreneurship. Ideas are a dime a dozen. It's the execution of the ideas, which means who is on the team & what is the culture within that team that fosters the experimentation to figure out which ideas are fruitful or not. A business is an economic experiment!

The problem of

#entrepreneurship

is not to come up with a unique idea or product, but to do it well--which means to supply a good or service that is well in line with what consumers value. It is as much about figuring out something new as it is to implement the idea well. It's a

6

34

115

0

3

12

I can't think of a better marketing opportunity than having one of your employees inside an agency. For the employee, it would bring advantages like WeWorks, but with people who work in the same discipline.

0

0

12

often overlooked...if you receive FEMA aid, you MUST purchase flood insurance to infinity and beyond...regardless of price.

If you receive FEMA aid, you are REQUIRED to purchase Flood Insurance for the life of the property!

0

4

3

1

2

12

Every time my 4 year old son gets told he couldn't make a more loud, obnoxious and annoying sound...he continues to redeem himself!!!

shoot me

4

0

12

The Latest Blog Entry From

@InsNerds

The Return of The Hanley in This Episode of The Attachment Point with Brett Fulmer!

1

4

11

Listen to this wise man. Insurance pricing is very very hard. If the wrong customers buy your product your underlying expenses can change dramatically.

Here's a thread about why many home and auto insurance startups founded 2015-present are having a hard time getting profitable. It's about insurance fundamentals, but explained for developers/people in tech.

1/

6

8

49

0

3

12

Random

#startup

tweet. One reason I rant about startups having prof sales people on board is, yes, to help sell. More importantly, it's to help in product dvlpmnt. How so? Who is better at inquiry-led product/market fit than a prof salesperson? ⬆️sales acumen = ⤴️ product design

3

2

12

Twitter expert

@AmberWuollet

discusses how to become better at Twitter to the Insurance Nerds Day audience.

1

1

9

Branch is another $LMND competitor who I believe has a structural advantage. Their CTO

@JoeEmison

is one bright dude and their bundling advantage from capital to capacity from auto to homeowners to umbrella is a winning combo long term

2

0

11

0

3

11

This is my favorite podcast. Why? Because I get to learn about all of these amazing companies and the sweat, tears (and sometimes blood) necessary to make something out of nothing.

There’s a NEW How I Built This!! And it’s poppin’ 🍿

In 2001 Angie & Dan Bastian started making kettle corn in their garage... 16 years later they sold

@Boomchickapop

for $250M.

Hear the incredible evolution of their partnership and their business 🔊

8

10

38

3

0

11

You can count on

@avibenhutta

&

@coveragerinc

to provide a beneath-the-surface analysis of

@Lemonade_Inc

0

2

11

@jasonkolb

100%. I get amused when technologists come into insurance salivating at how easy it is going to be to disrupt the model. I tell them to try selling some insurance policies to see how difficult it all is. When they tell me "it shouldnt be THAT difficult" , I say "I know - but that

2

0

11

“Auto Insurance as a Driver Companion Tool. Carey Anne Nadeau & John Henry of Loop Insurance.” Blog article and link to full video interview

1

0

11

PG&E sold a $200 million bond in August to insure against liability from infernos. Three months later, California was hit by its worst-ever wildfire. via

@WSJ

0

4

11

Lights flickering all morning. Expect power to go out sometime this morning to early afternoon as the winds are now picking up.

#naplesflorida

#Ian

10

0

11

0

2

11

The Latest Blog Entry From

@InsNerds

A Brief Interview With Eric Ross, Head of Venture Capital; Nationwide Insurance

0

0

9

Insurers are about to get ravaged by the War on Talent. Unprepared, inflexible with a centuries-old culture, the post-pandemic attractiveness of insurers is diminishing. But hope is not lost. My new podcast, The Yellow Book Road, will bring insights and wisdom to solve this.

2

1

11

I truly believe this. Implementing technology take rolling-up-your-sleeves fastidiousness. If you only write for profit then it's all how much premium I can collect vs how little I can payout instead of, how do I make people whole & do it while making a profit. 2 different things

“Somewhere along the way, we have lost track of why we underwrite. If the point of

#underwriting

is just to make a profit, then there is little impetus for us to evolve with technology.” –

@Nick_Lamparelli

,

@rethoughtins

&

@InsNerds

. Read the eBook:

0

0

0

0

2

11

@robgalb

@NicoleFriedman

@WSJ

@CoverWallet

@Aon_plc

@endofinsurance

My $0.02, Most small businesses that eventually buy business insurance online, as they grow and become successful (for those that do) will eventually want/need more sophisticated purchasing advice. Seed prospecting...

2

1

10

A note for all my friends in Insurtech...

Often forgotten, but obviously true:

“Superior sales and distribution by itself can create a monopoly, even w no product differentiation. The converse is not true”

-Peter Thiel

7

104

486

1

1

11

The single best piece of advice not only for entry level insurance sales producers, but anyone who is new at selling a complex product. Fail fast and establish credibility by building a catalog of stories.

@RyanHanley_Com

is the Gary Vee of insurance

SHOCKING!!

Goes against the what most every "guru" is preaching today.

You'll never guess my recommendation for how a 22-year-old insurance producer jumpstart his career -->

#insurance

#insurtech

#salestips

0

4

17

1

1

11

Twitter is (becoming) trash. Bringing out the worst of humanity. Allowing tribal instincts to amplify. We are all just members of mobs going after the other tribes using technology instead of fists or weapons.

4

2

10

Sales and managing people

Forget coding, sales is the most valuable skill in business

19

588

2K

1

0

10

Coach K once said: "I don’t look at myself as a basketball coach. I look at myself as a leader who happens to coach basketball."

I'm Sick of Talking About the Insurance Industry

2

1

10

AIG saying COVID19 will be largest CAT loss ever. Huge statement

2

0

10

Got to meet

@InsuranceEleph1

and

@InsurShawn

of

@SunlightSoluti2

at

#hartfordinsurtech

. Thank you for the pins!

1

3

9

Valid critique of $LMND's capital-light structure (though they were not specifically mentioned). Investors are unaware of the limited upside they placed on themselves. Investors want massive top-line results, but capacity will be an issue going forward

3

2

10

With every new tool coming to market, there will be new solutions. We are a generation away from having flood risk embedded into the global insurance ecosystem

1

2

10

Lamps tip of the day...when evaluating a major item, like a software platform, if price is the primary driver of the decision, then your odds of screwing the decision up is high and WILL inevitably cost you more. Don't be penny-wise and dollar foolish

0

1

10

As I have been saying, virtual events and conferences are doomed. We are Zoomed out and it is way too easy to check email and get distracted. Its time to think from first principles...

Zoom Fatigue

3

0

9