Money Visuals

@MVMoneyVisuals

Followers

3,237

Following

1

Media

655

Statuses

1,650

Sharing Timeless Ideas for Long-Term Investors | Helping Financial Advisors Publish Great Client Newsletters | Tweets Not Advice

Joined February 2021

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Iran

• 714480 Tweets

ايران

• 552985 Tweets

CENTURY OF LOVE EP7

• 165621 Tweets

Félix

• 140064 Tweets

Guatemala

• 103481 Tweets

アルゼンチン

• 95596 Tweets

Maligno

• 94232 Tweets

Be Mine

• 91270 Tweets

اسماعيل الغول

• 87132 Tweets

スペースマウンテン

• 85115 Tweets

BMX Freestyle

• 47311 Tweets

Adriana Ruano

• 41008 Tweets

Marta

• 40958 Tweets

#REVELINGinRV10VE

• 40145 Tweets

RIGI

• 36004 Tweets

男子バレー

• 23895 Tweets

taehyun

• 23890 Tweets

#STAYDominATEsFor6Years

• 22503 Tweets

#스테이도_스키즈가있어야_존재

• 22312 Tweets

رامي الريفي

• 21564 Tweets

Shane

• 17587 Tweets

TUBATUBBIES REVEAL PARTY

• 14058 Tweets

Hugo Calderano

• 13033 Tweets

千歌ちゃん

• 12706 Tweets

Ginting

• 11729 Tweets

松木平くん

• 11681 Tweets

Pinned Tweet

As an FYI, I'm taking a temporary break from all social media. If you love learning about long-term investing, I'd love for you to join my Rational Investor Newsletter.

0

0

3

Risk is NOT what you think.

When the media speaks of risk, they're almost always referring to volatility.

This is wrong.

Howard Marks has said "Volatility is, at best, an indicator of the presence of risk. But volatility is not risk."

So, what is it?

Risk, when properly

17

50

280

When we look back, all we see are all the missed opportunities. In hindsight, it all looks so obvious.

But looking forward, all we see is risk.

This is what makes successful investing so difficult.

4

42

231

Compound interest is not intuitive to most investors. Let me prove it to you.

Quick example: Suppose the average investor has $100,000 to invest for 30-40 years and is offered two portfolio options:

Portfolio A: Less volatile, but should earn a 5% return.

Portfolio B: More

6

30

177

14.5 years ago, Lehman Brothers filed for bankruptcy with almost $700 billion in assets.

11 days later, Washington Mutual went under with another $327 billion in assets.

From 2008-2012, over 400 banks failed.

Guess what. The world didn’t end. It only FELT like it was ending.

6

20

110

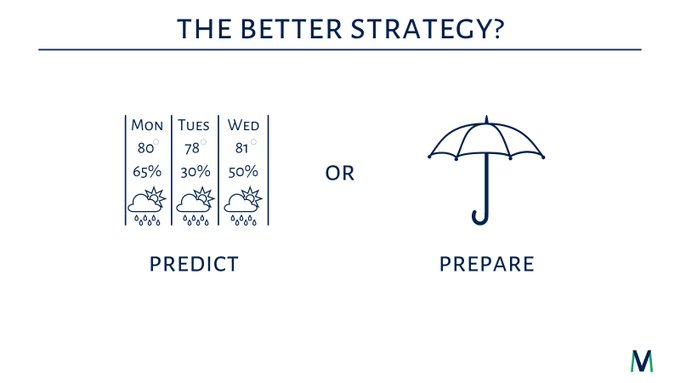

Financial planning is a lot like driving your car at night. You can’t see past your headlights, but you can make the whole journey that way.

We don’t NEED to predict the future to have a successful journey. We just need to make sure we don’t drive off the side of the road.

4

17

107

It's a factor of human psychology that what we are routinely exposed to is deemed normal, appropriate, and rational.

If we watch the financial networks, we can become convinced that knowing the future is possible and that we can successfully time our way into and out of the

1

21

91

Conventional wisdom has long held that:

Bonds = Income

Equities = Growth

But have you ever stopped to question this "conventional wisdom?"

What if equities are actually better for both growth AND income?!

Aside from my obligation to remind you that equities have grown by

4

14

93

When I tell people that my portfolio is 100% equities, I'm usually met with one of two statements:

1) Wow, that's risky.

2) Well, you're young…

Trust me when I tell you that it's not that I have a high risk tolerance and it's not that I'm young.

It's that I know what the deal

13

9

81

When we look back, the past seems so obvious which allows us to see all the missed opportunities.

Yet, when we look into the future, everything seems so uncertain and unpredictable.

And this feeling of uncertainty breeds feelings of risk.

If, instead, we use the past as a

2

12

77

This is NOT the time to sell.

It never is and never has been.

A simple look at the historical chart of the market is all the proof you should need.

Any attempt to time the market has been at worst detrimental, or at best, completely unnecessary.

Will there be more pain ahead?

3

11

70

Compound interest is not intuitive to most investors. Let me prove it to you.

Quick example: Suppose the average investor has $100,000 to invest for 30-40 years and is offered two portfolio options:

Portfolio A: Less volatile, but should earn a 5% return.

Portfolio B: More

4

15

69

The more certainty you seek from your portfolio in the short term, the lower your long-term returns will be.

It's obvious that the lower your long-term returns are, the probability of achieving your investment goals will decrease in lockstep.

While most investors think

2

10

67

THE HEADLINES ARE (ALWAYS) NEGATIVE:

- Inflation is still high.

- Banks are failing.

- The Fed has no idea what they’re doing.

- Interest rates and volatility are up.

- Plus a million other ever-present apocalyptic headlines.

THE TRENDS ARE (ALWAYS) POSITIVE:

- The global

2

6

60

When investors say that stocks are risky, what they mean to say is that stocks are volatile, which is true.

But the market, on average, goes up about 3 out of every 4 years.

And the result of these three good years for every one that’s bad has been an annualized return of about

7

5

54

"Every past market decline looks like an opportunity, every future decline looks like a risk."

-

@morganhousel

3

16

53

Same old song and dance during every single bear market decline.

I'm going to go out on a limb here: Nope, this time is not different either.

That must mean that bear markets are opportunities and we should treat them as such. Just keep buying.

3

7

53

We all know that the market averages 10% per year.

But it almost never returns 10% per year.

This is a problem for most investors because their return expectation of something "close to 10% per year" collides with reality (+22%, +14%, -16%, +7%, -21%, +19%, +13%, etc…).

This

1

5

50

It's a factor of human psychology that what we are routinely exposed to is deemed normal, appropriate, and rational.

If we watch the financial networks, we can become convinced that knowing the future is possible and that we can successfully time our way into and out of the

1

8

37

We’ve all heard the adage, “Buy low; sell high.”

Hard to argue with that idea on the surface.

But when you really think about it in practice, it comes with unavoidable issues.

First, investors very rarely want to “buy low” because they always think it’s going lower.

It

7

6

47

A truth that can never be forgotten once it's learned is often the most powerful truth. Here's one example:

The financial networks and mainstream media do not exist to help people become successful investors.

They exist to sell advertising.

To sell more advertising, they need

1

5

46

For the last 12 months, the market has gone pretty much nowhere.

For amateur investors, this is frustrating.

But for those who know their history, they realize that this is a great opportunity to dollar cost average into the market.

The reward is simply a matter of time.

1

7

43

"It's waiting that helps you as an investor, and a lot of people just can't stand to wait."

-Charlie Munger

Since the October bottom:

The S&P is up 17%.

International stocks are up 31%.

2

5

41

By the time you feel comfortable investing more money into the market, it will be well beyond where it is today.

It may decline from here, sure. That's always possible, even likely.

But they don't announce an "all clear" at the bottom.

Put the money to work. Then, be patient.

1

6

44

"All that glitters is not gold."

In other words, things are not always as they seem. There's a surprising amount of investing wisdom here.

For instance, in the media, they only discuss two things:

That is, what happened in the market today sprinkled in with "why" those things

5

6

46

What makes each bear market different:

1. A unique catalyst.

2. The depth of the crisis.

3. The length of the crisis.

What each bear market has in common:

1. They all end.

2. In retrospect, they are all seen as obvious buying opportunities.

Focusing on the bottom two instead of

0

14

45

From Howard Marks' latest memo:

"We don’t say, “It’s cheap today, but it’ll be cheaper in six months, so we’ll wait.” If it’s cheap, we buy. If it gets cheaper and we conclude the thesis is still intact, we buy more. We’re much more afraid of missing a bargain-priced

1

7

45

Anytime you are considering selling out of the market, take a moment to think about this:

Being wrong compounds forever.

This means there is significant risk involved in your decision.

It's obvious that the times in which we are most apt to sell is when the market is

0

4

45

Behavioral advice is worth exactly nothing, until it’s worth everything.

The problem is, the client nor the advisor knows when this point will come.

But, what if that point never comes…won't the fees be a complete waste?

Beyond the countless other benefits advisors have to

2

10

44

Just keep buying.

Given enough time, you'll wish you had bought more.

0

6

42

Suppose you go to the race track to watch the horses run.

As you walk to the counter to place your bets, you gather the following intel about the 1st race on the card:

1) There are only two horses in the race.

2) Horse one has averaged a pace of 2mph over his racing career.

3

0

42

Suppose you flipped a coin one time and I correctly guessed "heads." You might respond, "Lucky guess."

At the very least, I'm quite sure you wouldn't think I'm some kind of savant when it comes to coin-flipping.

But if you flipped the coin 20 times and I guess correctly every

3

10

43

Everybody has heard the adage that "the house always wins."

It's true because even though they only have a slight edge on some games, time is forever on the side of the casino.

And yet, casinos are full of starry-eyed gamblers hoping to hit it big.

In the stock market, we get

4

4

39

In 2022, the market fell 25% to its bear market low.

That is volatility.

Since the October low, the market is up almost 20%.

This is also volatility.

Over the last ten years, the market has averaged over 11% annualized.

This is BECAUSE OF volatility.

The fact that we have a

1

7

39

The SVB implosion is a great reminder of the risk involved when picking individual stocks--even seemingly good ones.

SVB was the 16th largest bank in the United States, and yet, it has collapsed.

You just never know.

There is a long list of companies that were considered the

3

1

37

The market always feels like it's either:

1. Too expensive.

2. Too risky.

Or occasionally, both.

The truth is, it doesn't matter.

Just keep buying through all markets and you're likely to do quite well.

That's all you need to know.

2

3

37

There's plenty of negative news out there, so I thought I'd point out a few charts from the JP Morgan Guide to the Markets that are worth noting...

Chart 1/8

Valuations are much more reasonable now than just six months ago.

2

3

38

If there is one truth we can all agree on regardless of our current level of wealth, it's that we'd all feel comfortable with "more."

The problem with this idea is that "more" is not a number. It's a perpetually moving target.

We might achieve a portfolio value that, in the

0

6

37

Thanks to the media's never-ending stream of soothsayers, it’s easy to become convinced that there must be some value in the forecasts of "market experts.”

And our clients may come to believe that we, as professional advisors, can sort through it all to offer some level of

0

3

36

It's been said that the people who made the most money in the 80s and 90s were those who dollar-cost-averaged through the 70s.

This makes intuitive sense, but most people ignore this wisdom.

As such, many investors have been miserable since the start of 2022 instead of

2

9

36

When the market is in (temporary) turmoil, it can be helpful to think smaller.

Let me explain.

Suppose you own a pizza place, IT support company, machine shop, or cleaning business, or whatever.

When the stock market and economy inevitably falter, I'm guessing you wouldn't

2

2

38

"Bull markets are born on pessimism, grow on skepticism, mature on optimism, and die on euphoria."

-Sir John Templeton

2

4

37

Two of the insurance industry's favorite marketing phrases are that their products are "not correlated to the market" and have "zero downside risk."

Sounds good at first glance.

Except, the market's probability of a positive return has historically been as follows:

1 Month:

1

4

36

The entirety of our investing lives has shown that human progress and a market moving up and to the right (over time) is the appropriate fact-based worldview.

And yet, this image so cleverly explains the perspective of most investors.

You don't have to let it describe you.

1

7

34

When you seek shelter from volatility, it feels a lot like you've eliminated "risk" from your portfolio.

In reality, it's highly unlikely that you have eliminated risk; you've simply shifted the risk to the future.

Here's how it works:

(1) Lower volatility = Lower Long-Term

0

4

34

We all know that the market averages 10% per year.

But it almost never returns 10% per year.

This is a problem for most investors because their return expectation of something "close to 10% per year" collides with reality (+22%, +14%, -16%, +7%, -21%, +19%, +13%, etc…).

This

2

5

35

"Volatility is, at best, an indicator of the presence of risk. But volatility is not risk."

-Howard Marks

So, what is it? See the visual below...

FYI: The possibility of a permanent loss of capital has historically never existed for the diversified investor.

That leaves

2

4

35

Many people believe that the job of a Financial Advisor is to be all about the numbers. I couldn't disagree more.

It's all about helping our clients better align their spending with their values.

This is what I wrote about in a new style of post today for our Client Memo

3

2

34

If you have a lump sum to invest, what should you do?

It's tough because we know that an enduring investing truth is that it will NEVER feel like a good time to invest.

But the data doesn't agree with this perspective since 77% of all market years are positive.

Nonetheless, it

0

5

33

12 Visuals for Successful Investing:

1: The correct way to build a portfolio is to first, identify the purpose for the money. Next, develop a plan built around that purpose. Finally, build a portfolio in service of said plan and purpose. Most everyone else does this in reverse.

2

13

34

Bear markets, bubbles, and volatility…

That's what has defined the 2020s so far.

Care to guess what the annualized return has been this decade?

About 10% per year. All you had to do to earn it was own it.

Never allow headlines to dictate your actions; it's almost always a

3

2

33

“In every age everybody knows that up to his own time, progressive improvement has been taking place; nobody seems to reckon on any improvement in the next generation.

We cannot absolutely prove that those are in error who say society has reached a turning point – that we have

0

6

32

Anyone who thinks they can earn equity returns without experiencing volatility has simply not looked at market history.

Volatility is part of the deal.

And while it's uncomfortable at times, it has historically been worth the discomfort 100% of the time.

1

7

32

This was true 50 years ago.

It's true today.

It'll be true 50 years from now.

Get the big things right and the little things won't matter.

0

5

32

There's a great saying that, "The people who made the most money in the 80s and 90s dollar-cost-averaged through the 70s."

As we close in on two years of flat and frustrating markets, don't let the pundits convince you to move to the sidelines to wait for clearer skies.

The

1

3

32

"Taking a fixed-income into a rising cost world is death on the installment plan."

-Nick Murray

3

4

32

“The first rule of compounding: Never interrupt it unnecessarily.”

- Charlie Munger

1

5

29

One of my favorite visuals I've seen for helping clients overcome future market volatility came today in the Humans Under Management email from

@MavenAdviser

-- I'd encourage you to subscribe. It's one of my favorite emails all month long.

2

4

30

Patience has historically ALWAYS been rewarded.

This time is NOT different.

0

4

27

I'm really excited to have this article come out! I hope it inspires every advisor to start their own private client newsletter.

Check it out!

And much appreciation to the entire Kitces team! They were so thorough and helpful throughout the entire writing and editing process.

For clients, more frequent communication can be a source of behavioral coaching and helpful information. In this guest post, Ashby Daniels

@MVMoneyVisuals

, discusses how a 'private' newsletter can help reinforce the value that advisors provide.

#advicers

1

1

16

1

4

29

Is volatility REALLY what you want to avoid?

Without it, there is no return. History has shown us this.

And yet the average investor does all they can to avoid it. This is why we are here.

1

6

30

Imagine that you decide to meet a friend for dinner at a restaurant that's walking distance from your home and on the walk to the restaurant, you witness all of the following:

1. a car crash

2. a house fire

3. a kid stuck in a tree

4. panhandlers

5. and people fighting in the

0

4

29

How to Lose Money (By Trying to Seem Smart):

1) Take big, unnecessary bets.

2) Buy complex investments.

3) Leverage.

How to Compound Your Money (By Not Being Stupid):

1) Buy low-cost, diversified investments.

2) Be patient.

"It is remarkable how much long-term advantage

1

6

29

To quote the 🐐, Nick Murray, the objective of diversification is:

"You never own enough of one idea to make a killing, therefore you will never own enough of one idea that you might be killed by it."

It's the latter part--the ability to stay in the game--that makes all the

1

1

28

The revised version of yesterday's visual thanks to

@jbrendanfrazier

Plus, I like the alliteration better.

3

4

26

Despite evidence that even the most "expert" forecasts are generally less reliable than a coin flip, the charade continues.

In this way, many investors appear to prefer heeding forecasts AND being wrong to simply dealing with unavoidable uncertainty.

The irony is that the

1

1

27

You can beat the market but never achieve your goals.

You can achieve your goals but never beat the market.

Ironically, trying to beat the market increases the chances of not achieving your goals

Few understand this.

2

5

26

Pessimism about the long term does not align in any way with a historic worldview.

You can choose to believe that right now is the beginning of the end, but that is a bet against all of human history and against human nature itself.

As has always been the case, progress

1

7

27

"When the time comes to buy, you won't want to."

-Walter Deemer

2

4

28

Investors are always trying to establish some level of certainty in the market so they can know what to do with their portfolio.

But we know that the only certainty in the market is uncertainty.

Think back over just the last three years regarding the Fed:

Investors thought the

0

3

26

Could not agree more.

Believe it or not, it is in fact possible to be cognizant of the problems we face today and yet still be WILDLY optimistic about what the future holds.

This is the kind of stuff we need more of. Positivity. Optimism. Understanding how lucky we are.

119

603

3K

0

1

23

The compounded return for the S&P since Jan 1, 2020 (pre-COVID) is about 9%.

My guess is that if investors were offered ~2.5 years of 9% compounding on NYE 2019, they would have gleefully accepted.

That's what they've gotten, but nobody is happy. This is why investing is hard.

0

1

26

Here's an enduring market truth for you:

It NEVER feels like a good time to buy.

Think about it…

Ten months ago, the market was hitting its bear market bottom at 3,577.

Few were lining up to buy (though they definitely should have been).

As I write this, the market stands

1

4

27

The media's job isn't to help our clients become great investors.

Their sole function is to sell more advertising. Never let your clients forget this.

1

2

26

We are hardwired to avoid anything that is painful in the short term.

But most things in life that offer long-term benefits require some sort of short-term discomfort.

“No pain, no gain.” as they say.

Naval Ravikant said it this way, "Simple heuristic: If you're evenly split

0

5

27

Just about everyone says their equity holdings are for the long-term.

But, then in the next breath, they ask what our thoughts are on the market right now.

It's unhelpful at best or detrimental at worst to have a short-term opinion on a long-term asset.

0

2

25

If you are starting off your prospect meetings by reviewing their current portfolio, you are doing it wrong.

1

2

26

The ultimate irony is that the more time you spend watching financial news, the worse your financial decisions become.

1

3

26

No advisor knows exactly when their advice will be worth multiples of a lifetime of their fees, but it's very likely that every advisor will earn their keep multiple times over every single time.

3

5

25

Don't let the pundits convince you to abandon your equities.

The ONLY way to ensure you obtain the entirety of the return equities have to offer is to own them perpetually.

Don't lose faith. The future remains bright, my friends.

0

2

25

Over the last 30 years, the S&P 500 has grown from 416 (in January 1992) to today's close at 4,132.

It should be obvious that the market is not, and never has been the problem.

It's people's proclivity to react to the catastrophe of the day that is the problem.

0

3

23

If you can master the human side of investing, you can figure out the numbers.

If you can’t master the human side of investing, the numbers don’t matter.

0

2

24

"The stock market is a giant distraction from the business of investing."

-Jack Bogle

1

8

25

What most people say:

"The market has lost investors a lot of money over the years."

What's actually true:

"Investors have lost a lot of money in the market over the years."

In a world where the market has increased by 70X (not including dividends) since 1960, anyone who is

0

4

25

James Clear offers the following example of the role of our identity in our decisions in his book Atomic Habits:

Imagine two people resisting a cigarette. When offered a smoke, the first person says, "No thanks. I'm trying to quit."

Alternatively, the second person declines by

3

3

25

Pessimists on the market are regarded as realists, well-intentioned, and high-minded prognosticators who offer prescient warnings with an exclusive focus on the actions of malevolent governments, corporations, or other destructive institutions.**

What pessimists miss is that you

3

4

24

An enduring market truth is that "The market ALWAYS feels like it's either too expensive or too risky."

In other words, it always feels risky to put money to work. But the only way to earn the full return of the market is to buy it...and then to be very patient.

1

3

24

Smart investors aren't looking for the portfolio that offers the highest potential returns...

Because they know that any portfolio that offers the highest possible return must also expose them to unacceptably poor returns as well.

The goal of effective portfolio management is

3

3

24

Anyone who professes to be a “long-term investor,” yet is worried about what has transpired in the last six months may want to rethink using the term long-term investor.

This is par for the course. This type of market event is expected, not an anomaly.

0

8

22

It's been said that the people who made the most money in the 80s and 90s were those who dollar-cost-averaged through the 70s.

This makes intuitive sense, but most people ignore this wisdom.

The same was true for investors throughout the decade of the 2000s.

And recently, many

1

2

24

"Compounding is the eighth wonder of the world.

Those who understand it, earn it. Those who don’t, pay it."

-Albert Einstein

0

5

24

If you're scared or frustrated at the market, it probably means it's a good time to invest.

0

3

22

"When the time comes to buy you won't want to."

-Walter Deemer

This is the entire experience of investing in one sentence. The very time we should buy is the time we least want to do so.

0

1

23

Everything doesn't have to be optimized/maximized for financial benefit.

I don't save in the most tax-optimized manner. I prefer optionality over tax benefits.

The most personally satisfying "giving" I do isn't eligible for a tax deduction.

And it's okay.

1

2

22

Want to know how relevant today’s news is to your long-term financial goals? Go back and read a paper from 10 years ago.

Actually, it’s worse than that…

Here are two real headlines, both from the same source less than two months apart:

Headline from July: "Dollar’s Busted

0

3

22

Given the number of people I've heard of who are now regretting their decision not to act a month ago, I'm convinced this graphic is as true as ever.

1

3

22