Shehzad Qazi

@shehzadhqazi

Followers

6,156

Following

4,474

Media

863

Statuses

16,338

Managing Director, @ChinaBeigeBook . Tweet on economic, geopolitical, and policy issues driving financial markets. Views my own. RTs & Likes ≠ endorsement.

New York City

Joined October 2010

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Valencia

• 443067 Tweets

#nicetwoMeatuxLingOrm

• 428919 Tweets

LINGORM N2U LIVE

• 415440 Tweets

River

• 389177 Tweets

DANA

• 362088 Tweets

MOMENTS OF LIFE FREEN BECKY

• 136230 Tweets

ポケポケ

• 98832 Tweets

Mazón

• 54195 Tweets

フレンド

• 37498 Tweets

ピカチュウ

• 32719 Tweets

AEMET

• 29718 Tweets

Ahmet Özer

• 28638 Tweets

Turia

• 28615 Tweets

Esenyurt Belediye Başkanı

• 25079 Tweets

Albacete

• 22491 Tweets

ポケモンカード

• 19551 Tweets

KAIRAIN TWOBILLION VIEWS

• 16803 Tweets

会派入り要請

• 16002 Tweets

Fokus Bekerja Untuk Rakyat

• 15906 Tweets

橋本環奈

• 14105 Tweets

ポケカのアプリ

• 12464 Tweets

中川大志

• 12254 Tweets

#刀剣乱舞ONLINEもうすぐ十周年

• 11960 Tweets

ミュウツー

• 11263 Tweets

#うちの本丸の厨番長

• 10874 Tweets

#FII8

• 10148 Tweets

![[[Exclusive]] FBI: Most Wanted TV SERIES](https://pbs.twimg.com/profile_images/1214174250195505152/WqGXZRVV.jpg)

Pinned Tweet

Great chat this evening w/ Tyler Mathisen,

@timseymour

@GuyAdami

,

@CourtneyDoming

, and

@RiskReversal

for

@CNBCFastMoney

.

Is China gearing up for the next big trade war with the U.S.?

@ChinaBeigeBook

's

@shehzadhqazi

gives his read on China's economy and the likely impact on business relations:

5

10

50

1

3

13

"China is now well past its peak “demographic dividend”—ratio of working-age pop to young+old dependents...this is occurring at much lower income level than elsewhere...share of pop 65+ is ~12% even though🇨🇳PC income is 1/2🇯🇵's when it hit this milestone."

9

86

228

“The report said that top Biden officials continually changed guidance even as the operation was under way, adding to pressure on American personnel on the ground who were working in dangerous and traumatic conditions.”

4

88

171

How quickly we’ve gone from the “we need more Muslims to condemn terrorism” trope to “we need more Muslims to condemn China.”

12

35

154

Folks, don’t make the Lehman comparison. You don’t get a Lehman moment in a non-commercial financial system.

Folks, don’t miss the potential implosion of China’s giant property developer

#Evergrande

under $300 billion in debt. This is of Lehman proportions with big economic and political dangers.

60

327

1K

7

21

150

“China’s property mkt has fallen back into a deep slump, developers are having more cash-flow problems & 🇨🇳authorities are trying more ways to revive🏠demand. Potential🏠buyers are expec prices to fall & think better deals will emerge if they sit & wait.”

8

53

152

The "China is back" narrative has become gospel truth. But China’s own numbers as well as independently collected data don't tell the story of a blockbuster rebound. Instead, they show a full-year recession hiding in plain sight.

@barronsonline

THREAD

4

51

110

Trillion or so added to Chinese equities this week purely on rumors, which were rubbished in today’s meeting.

13

14

113

“Nasdaq Golden Dragon China index had its worst day in history. Amazingly, it is now no higher than it was in December 2006”

@johnauthers

2

46

114

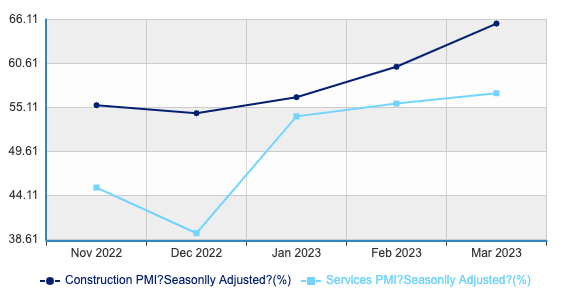

China's non-manufacturing PMI sub-components:

- Construction: 60.2 (Feb) to 65.6 (Mar): +5.4 (m/m)

- Services: 55.6 (Feb) to 56.9 (Mar): +1.3 (m/m)

Construction and govt spending is supercharging this PMI, not surging household/consumer spending.

6

41

114

China's official data lack credibility because of the NBS's questionable statistical methods, including cherry-picking what data to publish. Its Q3 GDP release brought back concerns about accuracy and manipulation.

THREAD...

@ATFinancial_

@ChinaBeigeBook

4

32

105

Over $43 billion in value lost for Tencent overnight.

How many times have we heard i-bank strategists tell us the regulatory crackdown was over?

They’ve been wrong over and over again.

“New draft guidelines released by China’s top gaming regulator require owners of online games to abstain from providing or condoning high-value or expensive transactions in virtual entities whether by auction or speculative activity, among other things.”

2

5

17

10

17

101

People who can barely predict next quarter’s GDP are predicting where the world will be in 50 years. 😅

A three-horse race 🐎

Goldman Sachs predicts China 🇨🇳, India 🇮🇳, and the US 🇺🇸 will be the world’s three largest economies in 2075, and in that order.

No European 🇪🇺 country is close (1/2)

Cc:

@Rajeev_GoI

@USAmbKeshap

@KanchanGupta

@Noahpinion

@ElbridgeColby

82

161

617

9

15

98

We have been -- both privately and publicly -- arguing strongly against the idea that Chinese households would plough their savings into experiences and purchases as soon as zero-COVID was over. The market consensus was wrong, we warned. The numbers speak for themselves...

Chinese households are still saving at a faster rate than last year. New deposits rose 27% in the first quarter from a year ago, even after Covid Zero was scrapped and the property market began to stabilize. New savings rose a massive 80% in 2022. Chart by

@yujingliu_

9

33

204

12

18

88

Pakistani decisionmakers are increasingly panicked about their debt servicing requirements to China and the severe repercussions of an eventual default. Back in the 2010s CPEC was all the rage. Now it’s yet another source of stress on Pakistan’s dismal financial condition.

5

28

78

It is hard to overstate how badly prices crashed across the various property sub-sectors in China in December.

Residential and commercial construction are in a deep contraction.

@ChinaBeigeBook

data have been capturing this bloodbath in real-time.

December another bad month for China's property market.

From

@ChinaBeigeBook

's December flash data: "Prices tumbled hard this month. Both home builders and residential realtors reported outright declines in sales prices, as did commercial construction firms."

1

6

19

4

25

78

“Local governments in China have asked several companies to pay tax bills dating back as far as the 1990s, underscoring their need for funding due to the uneven economic recovery and persistent housing slump.”

1

41

75

I can't stress how important it is to watch China's massive downward revisions to 2019 data rn. Markets are either ignorant of this or ignoring it. Either way too many investors drinking the YoY growth coolaid. Sorry folks, but China is not "back."

China's FAI release today indicated further downwards revisions to historic series from Nov 2019 (by Rmb4.68trn), based on historic data from last month. This following the removal of Rmb3.6trn worth of historic investment in October. Without, Jan-Nov FAI wouldve been -6.4% yoy

3

19

32

2

23

68

“1. Iron ore futures continue to sink due to China’s falling demand for steel.”

Chart via

@SoberLook

1

12

65

"Chinese traders are willing to pay as much as 40% more than the value of the underlying assets in some exchange-traded funds in order to obtain exposure to foreign stocks. That’s triggering trading halts in a number of ETFs as well as purchase limits."

4

17

61

Property took a beating in May and it bodes poorly for growth overall in Q2. Will have more to say on rebound prospects for housing specifically and the Chinese real estate sector broadly soon.

@ChinaBeigeBook

@markets

4

11

62

Overnight official stats confirm what

@ChinaBeigeBook

data showed us weeks ago: the idea of surging consumer spending was oversold.

There's hardly evidence of revenge spending as yet. As we explained: weak labor market + overhang frm property downturn=consumers being cautious.

"The pickup in retail sales was driven by spending on medicine, petroleum products and catering, while automobile purchases slumped, according to the official data."

2

4

13

2

19

57

This Chinese downturn is different because the China economic playbook is different. Those who understood this knew the economy wasn't getting a shot in the arm, while those who didn't are still arguing between downgrading GDP to 4.2% vs 4.3%.

2

12

53

"Traffic from China’s ports has slowed significantly, empty containers are stacked six high and trucks w/ no cargo dot the highway leading to the major terminals. The world’s largest box-ship op plans to return dozens of chartered vessels to their owners."

1

17

55

No press conference would’ve been better for markets

Live: China rally loses steam as authorities disappoint markets; Hong Kong stocks plunge more than 6%

@CNBC

3

10

54

The mega bulls have been overstating the China consumer rebound case for 2023 and way too loudly. As

@ChinaBeigeBook

’s feb data showed, the Jan surge in spending lost steam into Feb and was down y/y too. The comeback story is far from cemented as yet.

“Consumption, a priority for Xi, has yet to see any major stimulus during the National People’s Congress this week. While there’s been a rebound in consumer spending since the end of Covid restrictions, the recovery so far has been uneven.”

2

9

23

3

18

51

China Fixed Asset Investment (accumulated) grew by 3% in 2023 per the NBS. But it also fell by 12%...per the NBS!

WHAT?

NBS again massively revised its 2022 data to get y/y growth, this time wiping out >8 trillion yuan worth of investment activity from 2022.

4

11

53

The bull-case for China has popped. It was built on disastrously bad forecasts. Why? Bc Wall Street won't recognize that today's Chinese economy no longer operates on the same principles they've been accustomed. My latest for

@barronsonline

@ChinaBeigeBook

2

15

50

Why US dependence on China for pharmaceutical supplies is a serious national security threat.

"10 Chinese cos producing everything from Ibuprofen to Covid-19 testing kits, have in recent days issued statements or confirmed in interviews that all of their production would be sent to government groups rather than fulfilling private orders."

2

20

45

0

17

51

The recent rally was fueled purely by hope, not by data showing monetary stimulus or an economic rebound or evidence of zero-COVID being dialed back or regulatory easing. There was no China bull case and it’s plainly obvious now.

0

15

49

Details confirm the policies are meant to support already strong developers, including protecting them from becoming targets of Beijing's "clean up" of the sector, and paving the way for greater industry consolidation. This isn't a property bailout.

1/4

3

19

48

“China’s bank loans to the real economy contracted for the first time in 19 years, a grim milestone that underscores why weak domestic demand has emerged as a major hurdle to the economy’s growth and recovery.”

4

19

50

“Under the deal (still being finalized) China would go after chemical companies to stem the flow of fentanyl and source material.. In return Biden admin would lift restrictions on China’s forensic police institute, an entity the US alleges is responsible for human-rights abuses.”

7

20

48

Wall Street’s bullish bets on China were predicated on 3 expectations: end of zero-Covid in 2022, regulatory crackdowns easing & policy stimulus finally getting implemented. Each of these has proven disastrously wrong. New

@barronsonline

op-ed.

@mattbpete

2

19

47

Pretending to be inside Xi's head has led to monumental losses for several years now. The common prosperity bet backfire is just one example.

"Investors who bought into the idea two years ago that China’s consumer and green energy stocks stand to win big from President Xi Jinping’s renewed economic agenda would have seen their holdings pummeled in 2023."

0

6

17

4

11

47

"10 Chinese cos producing everything from Ibuprofen to Covid-19 testing kits, have in recent days issued statements or confirmed in interviews that all of their production would be sent to government groups rather than fulfilling private orders."

2

20

45

"China has a bigger problem lurking behind all those empty apartments: even more homes that developers already sold but have not finished building. By one conservative estimate, that figure is around 10 million apartments."

@jotted

6

23

44

The China equities rally in early 2023 was divorced from economic fundamentals. Now Chinese stocks are in free-fall, again divorced from economic fundamentals. Sentiment alone has been in the driver's seat all year.

4

13

45

The thing about COVID cases is they're pretty strongly correlated with testing😬

4

6

45

So China's industrial capacity utilization *fell* ~2% y/y but manufacturing component of GDP grew 2.8% y/y (and construction grew 6.7% y/y)?

What am I missing?

"The industrial capacity utilization rate in China fell to 74.3 percent in the first quarter of 2023 from 75.8 percent in the same period a year earlier. This was the lowest level since the March quarter of 2020" via

@tEconomics

0

7

20

8

9

46

This can’t be stressed enough. The whole China saving the world economy thesis becomes a lot more shaky when you start looking at what’s driving Chinese recovery: NOT 🇨🇳 consumers but factories meeting EXTERNAL demand and a construction boom.

Consumer spending in China officially contributed 1.7 percentage points to Q3's 4.9% GDP growth, or 35% of GDP growth for the quarter. This is better than in the first two quarters, but belies any claim that consumption is powering Chinese growth.

6

32

75

3

15

46

We spent all of 2023 warning markets that the "China manufacturing collapse" thesis was very wrong. Today this sounds consensus, but last year this was about as contrarian as we could be.

Here's what we said at the time...

Astonishing how many folks got this one wrong. And it's a big, big thing to get wrong.

0

6

33

4

7

45

"Death sentences were handed to Fu Zhenghua, fmr justice min, Sun Lijun, fmr dep min public security, fmr top Jiangsu official Wang Like...While sentences were mostly fr corruption authorities noted cases were related to a “political gang” disloyal to Xi."

2

24

42

Moreover, unrevised data show aggregate total retail sales contracted 4.8% y/y or ~1.97 trillion yuan in 2020. (Even based on revised data they fell by 3.9%.)

No matter how you slice the official numbers China is not seeing a broad-based recovery that includes Chinese consumers.

2

14

41

Lastly, and most importantly, however, China’s old economic model has run out of road, and the economy is inexorably headed toward much slower growth. The new bull case for China will be much more subdued than markets have been prepared for.

/END

21

4

43

"Most credit in China is directed thru businesses, state-owned enterprises, local governments, and Beijing to investment in infrastructure, property, manufacturing, or extractive industries. A much smaller share is directed to households"

@michaelxpettis

7

8

44

China worries are back in the headlines since Apr retail sales, FAI, industrial production data missed expectations on top of falling PMIs and CPI.

This is a big sentiment reversal from March. So what's actually going on?

Here's what key

@ChinaBeigeBook

data say.

3

11

42

There will be stimulus but Beijing isn’t interested in bailing out the stock market. Instead stimulus will be focused on stabling the property market and putting a floor under China’s economic growth.

Latest w/

@SeanaNSmith

&

@thebradsmith

for

@YahooFinance

@ChinaBeigeBook

China's disappointing economic recovery has come to an end, according to China Beige Book managing director

@shehzadhqazi

: "Markets are seeing this and markets are panicking."

9

25

67

5

12

43

"CCP propaganda is spinning stories abt youth making decent living deliv meals,recycling...fishing/farming.. trying to deflect accountability frm econ-crushing policies eg pvt sector crackdown, unnecess harsh Covid restrictions,isolating trading partners."

3

12

38

“Any notion of 5.5% growth in 2022 died the moment big cities started their descent into Covid Zero lockdown, writes Leland Miller, CEO of the authoritative

@ChinaBeigeBook

advisory, in an email.”

@barronsonline

2

11

40

"Brazil has raised tariffs on steel alongside Chile while S. Africa imposed 10% levy on solar panels, Indonesia extended duties on cheap textiles & Thailand has inc VAT on low-value imported goods. All these industries are grappling w/ Chinese competition"

3

12

42

If you believed my i-bank friends who said zero-COVID was going to be eased this year you lost money.

3

6

37

Pakistani man carrying bouquet screams “I’ll f🌺ck you right here, motherf🌺cker.”

Very romantic, indeed.

If you think Iranians are passionate, wait until you meet Pakistanis.

81

73

666

2

2

40

Not only do China's own Q2 operational capacity numbers belie claims of YoY expansion,

@ChinaBeigeBook

data collected from 3,000+ firms show 55% capacity on avg. How could an economy operating at half-cap expand quicker than year ago levels?

3

30

38

Loan rejections spiking may be the single most important China credit to watch right now.

Credit slowing was old news for us.

@ChinaBeigeBook

's May release: "Corporate borrowing continued to slide as loan rejections shot up amidst rising applications. Bond issuance fell too."

BUT among firms that borrowed new lending (rather than rollovers/credit extensions) did ⬆️.

1

3

7

3

18

41

“Still Apple is moving carefully. Its leadership is concerned that China might retaliate if it moves too much capacity to other countries, or transitions too rapidly. Customers in China could turn against US-designed products amid heightened nationalism.”

1

11

39

"Since Feb global investors have unloaded $27b in yuan-denominated CN policy-bank bonds, or ~1/6th of total holdings of such debt...outflow is part of $61b exodus from yuan bonds spurred in part by Yuan weakness & shrinking yield advantage over US debt."

4

14

41

Let's see how this looks in about 9 months!

#China

2023 GDP growth forecast:

Citi: 5.7% → 6.1%;

J.P. Morgan: 6.0% → 6.4%;

Goldman Sachs: 6.0% → 6.0%.

15

69

295

3

3

41

The record shows that Wall Street’s views on China are filtered through Beijing’s political calculus and subject to its redlines, preventing it from honestly discussing China’s economic and political challenges or the prospects of its companies.

China Beige Book's Shehzad Qazi tells the US House Select Committee that China's economic data can't be trusted and Wall Street has to answer for its role in propagating propaganda.

@willkoulouris

@ShehzadQazi

#China

@USHouseNews

3

11

31

2

14

40

"This was supposed to be the yr to buy🇨🇳stocks as investors counted on Beijing to supercharge the economy &revive property mkt aftr yrs of Covid restrictions. Such certainty has instead been replaced by weak sentiment that’s proving partic hard to reverse"

4

11

41

OK, folks

@ChinaBeigeBook

's note on today's China stimulus announcements is out to clients now.

Key point: In no way are the policy measures we got today a “bazooka” of any kind.

4

9

41

"cash from Evergrande is being used to finish projects for homebuyers at expense of bond & equity holders. The rule of law is the rule of Xi & he is pragmatic. He deems the well-being & happiness of homebuyers more important than a few upset bondholders."

@JohnFMauldin

3

7

38

Buy Chinese tech stocks, they said. The regulatory crackdown and Covid-zero policies are being eased, they said.

2

5

39

What good is sellside research if it tells you exactly what the Chinese government tells you, except 4 months late and after a massive market sell-off?

Wall Street Cuts 2023 China GDP forecasts yet again!

Morgan Stanley reduced its estimate from 5.7%➡️5%

JPMorgan trimmed its forecast from 5.5%➡️5%

Citi economists lowered their forecast from 5.5%➡️5%

Nomura held its forecast for 2023 at 5.1%

@markets

0

6

15

1

8

38

The official December China PMIs show the economy contracted for a third consecutive month. Importantly, more firms reported contractions this month vs Nov. Why I said this morning it was way too premature to call the bottom.

@tEconomics

@markets

@ChinaBeigeBook

If COVID hasn't peaked as yet--and it hasn't--then decisively calling a bottom in December is incredibly premature.

3

4

15

2

9

38

“This is just the latest example of China disappearing economic data series that don't just show weakness, but show weakness in politically sensitive parts of the economy,” said

@ChinaBeigeBook

’s Shehzad Qazi.

@barronsonline

@reshmakapadia

2

14

37

The digital renminbi is used least often by Chinese firms to receive payments from customers for online transactions. Even ApplePay is more commonly used than e-CNY. Let's begin our "internationalization of Yuan" theses with this data.

Chart from

@ChinaBeigeBook

Platform.

1

13

39

"China’s consumption recovery has lagged other major economies."

@thedailyshot

Trend also seen via falling import orders 2 wks ago. The idea that China is driving a global recovery is baseless.

Chart via

@SoberLook

1

19

36

Honored to be testifying at the Select Committee on the Chinese Communist Party's hearing: "Risky Business: Growing Peril for American Companies in China."

Watch live on Thursday, July 13 at 7:00pm ET using the link below.

@committeeonccp

@ChinaBeigeBook

1

12

37

“You can feel the momentum has shifted in favor of Chinese brands,” Dunne said. “The government is talking about self-sufficiency, nationalism, depend on ourselves. Chinese consumers say, ‘I can get pretty good car now from Chinese brands.’”

6

12

36

“The biggest glut of copper in 4 yrs has built up in Chinese warehouses.. In the four weeks since the record high copper has fallen 13%..weak mkt in🇨🇳has led copper for delivery to Shanghai to trade at discount to global benchmark price, a rare occurrence”

3

17

38

"Fear of breaching ambiguous redlines means increasing vol of research is so slow & vague it’s of questionable utility said ppl [anonymously] fr fear of career ramifications. A global money mgr said even internal reports & data at their firm are impacted."

3

20

37

"Global investors wanting to profit from China’s economic recovery are...loading up on shares of Euro, US & Japanese cos instead of🇨🇳stocks, as high geopolitical tensions b/w🇨🇳&🇺🇸have made it unpalatable for some int'l money managers to invest in🇨🇳firms."

2

9

36

1/ This

@MorganStanley

graphic is a good example of

faulty analysis resulting from monthly PMIs, which are exaggerating economic strength currently (many at multi-year highs). PMIs are not magnitude measures, just directional...

Data:

@IHSMarkitPMI

. Chart:

@SoberLook

Good insight by

@shehzadhqazi

on some of the pitfalls of business surveys (we've been hearing predictions of V-shaped recoveries since March!) and why survey methodologies can use improvement. Geopolitical and climate disrupters to the economy further cloud these outlooks.

1

1

6

1

6

36

"Coal output in China surged 9% to 4.5 billion tons last year, more than half the world's total, and continued to rise this year, government data showed, with coal plants under pressure to offset a 22.9% decline in hydropower generation during 1H-23."

2

18

35

"Beijing cut the down-payment ratio for 2nd🏠to 40%/50% vs prev threshold of 60%/80%...also lowered down-payment ratio for 1st🏠to 30% from 35%/40% + allowed more🏠to qualify for lower mortgage thresholds by relaxing definition of 'non-luxury homes'..."

4

10

37

"Consumption in China “has been weak, is weak and will be weak going forward,” said Leland Miller, chief executive officer of

@ChinaBeigeBook

."

1

11

36

Proprietary data from

@ChinaBeigeBook

showed a pretty big jump in steel production over 2023.

Issue isn't Beijing lying about its steel production data. Real question is, with property in the doldrums, where is the final demand coming from?

"There are other indications that what seems too good to be true often is. Steel analysts..point to conflicting data: iron ore imports that hit a record in 2023 w/out disturbing inventory levels, rising rebar stockpiles, and inc output of steel products."

0

0

8

12

12

36

“More than 130 US companies use these same Chinese auditors for significant parts of their audits, according to research by 3 accounting profs. Their research shows that companies audited by these Chinese firms face higher risks of accounting problems.”

1

15

35

“Beijing will never announce a second-quarter contraction, Li Keqiang made that very clear,”

@ChinaBeigeBook

's Leland Miller told

@BloombergTV

. “We think that they are going to throw a number in the 2% range out. It's not justified by the data.”

1

6

34

Seems like folks writing about China’s economy are feeling more stimulus pressure than those running China’s economy.

2

5

36

"ordinary Chinese are discovering how quickly fortunes can turn in the housing market. Creeping price declines & plummeting sales have called into question the way freewheeling property developers have financed, built and marketed homes to masses."

@markets

4

16

36

It's clear across

@ChinaBeigeBook

's multiple indicators of business performance that the Retail sector has not returned to its pre-covid growth levels. There was never a consumer spending bounceback.

This point is now becoming consensus but a few months ago it was heretical.

END

1

12

33

How I feel about international relations as a discipline

Political science isn’t a real intellectual endeavor. It should be ended at all universities and turned into either history or politcal philosophy.

26

33

264

1

9

33

“full reopening may lead to 5.8m people being admitted to ICUs overwhelming a health system w/ <4 ICU beds/100K. In first 6mnth of omicron ~1/4 🇺🇸+EU were infected. A similar caseload in🇨🇳would lead to 32K daily ICU admissions or 2x beds🇨🇳has.”

@SamFazeli8

3

11

33

“moves will mark complete exit frm 🇨🇳for (VGR) which once saw sign potential there…reversal stands as cautionary tale for global peers incl BlackRock & Fidelity that are racing to build up local ops as🇨🇳recovery & new pension reform brighten prospects.”

0

14

35

“2 months into 2023 this reopening trade is stalling. Hedge funds who piled into the rally late last year are rapidly trimming risk. Key stock benchmarks in Hong Kong have fallen more than 10% from their Jan peaks. Bond outflows have resumed.”

@SofiaHCBBG

3

10

33

"provinces are selling new special bonds at the slowest pace since 2021, falling well short of quotas amid a dearth of suitable projects now that China is saturated w/infrastructure..Meanwhile they’re running short of cash [for] needs like paying salaries"

4

8

35

Here's a fun NBS math problem. Fixed Asset Investment:

Jan-Jul 2020: 32,921.4b

Jan-Jul 2021: 30,253.3b

YY growth rate? -8.82%

But for NBS, YY growth: +10.3%

Press releases:

2020:

2021:

3

11

34

Evergrande's implosion is happening within the backdrop of a property downturn. We know a Lehman moment is essentially impossible in China. But while investors don't have reason to panic, they do have multiple reasons to worry.

@barronsonline

THREAD

3

18

35

“ Xi’an will use lockdowns and school and business closures as part of its plan to contain influenza outbreaks, sparking concern among citizens about a return to the country’s economically-crippling Covid restrictions.”

1

13

33

If China's inflation numbers overnight and trade numbers earlier this week tell us one thing, it's that year-on-year comparisons have been absolutely torturous, misleading, and pretty useless this year for China watchers.

1

8

34

“Nearly 37 million people in China may have been infected with Covid-19 on a single day this week, according to estimates from the government’s top health authority, making the country’s outbreak by far the world’s largest.”

6

14

33

"The China reopening trade for commodities is showing signs of flagging, as weak demand offsets speculative bets that the end of Covid Zero will reignite growth...questions over the timing and degree are capping prices from copper to coal and crude oil."

0

13

33

“When Evergrande’s auditor, PwC HK, signed off on its 2020 financial statements, it didn’t include a so-called going-concern warning. These red flags from an auditor show it has doubts about the company’s ability to stay afloat for at least 12 months.”

2

11

31

China’s economy is in the toughest place it’s been in 2 yrs. Monetary stimulus is a myth. Fiscal stimulus hasn’t kicked in, and labor mkt is weaker than 2021.

Great convo w/

@MartinSoong

on

@CNBC

@asiasquawkbox

.

@ChinaBeigeBook

0

8

32

China's retail sales were a big storyline this week. Lots of focus on y/y growth slowing in May (12.7%) from Apr (18.4%).

No mention whatsoever that Apr 2023 looked strong b/c Apr 2022 was so poor: it had the worst nominal retail sales & the largest y/y contraction of the year.

Markets are paying too much attention to headlines about

#China

economic data & not enough attention to actual 🇨🇳 economic data.

A deep dive into retail sales, industrial production & fixed asset investment in May tells a more...interesting...story.

1

6

27

3

7

32

To put things in perspective, Hang Seng is still down ~30% y/y.

Worse yet, it's also still at the worst level seen since January 2009.

We're going to need a lot more biggest two-day rallies to climb out of this deep hole.

Chinese stocks in Hong Kong post biggest two-day rally since late 2022. Late surge came after the PBOC surprised markets by announcing a cut to banks reserve ratio requirements

11

30

156

4

8

33