Leveraged Loans

@lcdnews

Followers

22,239

Following

1,020

Media

5,656

Statuses

68,437

Part of PitchBook Data, LCD is news and analysis on leveraged loans/private credit, high-yield bonds, distressed debt. Check out free news & analysis below.

Seattle, London, NYC, SF, SG

Joined April 2009

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Garbage

• 2165962 Tweets

ハロウィン

• 1226776 Tweets

Valencia

• 1037933 Tweets

DANA

• 816757 Tweets

الاتفاق

• 694650 Tweets

Happy Halloween

• 286917 Tweets

Virginia

• 224243 Tweets

ポケポケ

• 166262 Tweets

Trick or Treat

• 133545 Tweets

RTVE

• 122832 Tweets

#週刊ナイナイミュージック

• 120248 Tweets

イタズラ

• 74017 Tweets

Arnold

• 60203 Tweets

SCOTUS

• 55849 Tweets

SÃO PAULO TODAY

• 43100 Tweets

トリックオアトリート

• 32381 Tweets

Jerez

• 31309 Tweets

OVER THE MOON TEASER 1

• 26723 Tweets

ミュウツー

• 26142 Tweets

Rotten

• 23341 Tweets

Rishi

• 22427 Tweets

GALA EN LA MEJOR

• 21993 Tweets

Sunak

• 21194 Tweets

Buzz Aldrin

• 20179 Tweets

해피 할로윈

• 19403 Tweets

横浜優勝

• 17488 Tweets

La Palma

• 15880 Tweets

ミュージカル組

• 13345 Tweets

Corporate defaults worldwide are emerging at their fastest pace since 2009, with 15 in February alone, S&P says. The Retail sector is the biggest culprit, accounting for more than 30% of the 2023 global default tally

#leveragedloan

#highyield

4

73

154

The number of US

#leveragedloan

issues trading in the secondary below 80 cents on the dollar - a common measure of distress in the asset class - continues to climb

2

49

101

A move into June allows pandemic-only look at US

#leveragedloan

mart. Those downgrades all are talking about? They've outnumbered upgrades by a surreal 43:1 over past 3 months. In Great Financial Crisis this metric topped out at 8.45:1

@Kakourisr

4

52

87

About a month ago 60% of the $1.2T in outstanding US

#leveragedloan

debt was priced at 100 or better. A week ago it was 38%. After today just 10% of that debt is priced at par

#COVID19US

#economy

4

37

86

"Bankruptcies among private companies with at least $10 million in assets had jumped to an average of 7.8 each week by late February, a stark increase from the pandemic peak of 4.5 in June 2020 ..." via BBG

#defaults

4

24

83

Nearly 77% of all outstanding US

#leveragedloan

debt is covenant-lite. That's (yet another record)

2

56

74

A new record: 79.6% of the $1.8 trillion in US

#leveragedloan

outstandings is cov-lite. That's about $940B. The bulk of that ls riskier debt, from issuers rated B and B-

2

45

73

Maturity wall update: The amount of

#leveragedloan

debt due in the next 2 years is larger than ever, and roughly half of that are riskier, B-minus rated credits (better-quality borrowers have refinanced already)

@Kakourisr

@PitchBook

3

25

71

Coranavirus fallout: $672B of $1.2T US

#leveragedloan

mart is now categorized as distressed debt. Easily the most ever by amount, but significantly less in share than in '08. "Distressed" here = trading market price of less than 80 cents on dollar

2

60

68

More on debt coverage: Moody's says better than half of riskier, B3 (B-minus) rated corporates will have interest coverage of less than 1x in 2023-24. That's a ratio many analysts say indicates weak financial health

#leveragedloan

#highyield

@PitchBook

1

24

67

That's 18 bankruptcies among private equity portfolio companies so far in 2023, the fastest pace since 2020. One reason: The Fed has been raising rates (making debt more expensive), from near zero in March 2022 to 5.25% today

@PitchBook

#leveragedloan

1

18

64

1Q earnings growth for US loan issuers was negative; that hasn't happened since the recession (free)

3

55

66

27 US

#leveragedloan

defaults in 2Q20, totaling $23B, the most since 2009. Default rate now stands at 3.23%. That's a five-year high, and up from 1.84% at end of 1Q

@Kakourisr

0

40

63

Banking Crisis Raises Concerns About Hidden Leverage in the System

Via BBG

#leveragedloan

#highyield

#PrivateCredit

5

28

61

Covenant-lite share of US

#leveragedloan

outstandings continue to hold at ~79%. That's roughly $950B of what's now a $1.2T market

2

34

57

S&P Global Ratings: US

#highyield

default rate expected to hit 10% over next 12 months (it was 3.1% at year-end 2019

#leveragedloan

2

28

58

After record month of downgrades, riskier, triple-C rated debt accounts for 7.48% of US

#leveragedloan

market. That's an interesting number: Most CLOs have 7.5% threshold for CCC debt. Full analysis

@millarlr

0

21

56

What with soaring stock markets and bulging private equity coffers we'll note that purchase price multiples on US LBOs hit a record 11.51x in 2019. They were 10.6x the previous year and 9.68x in 2007

#leveragedloan

#highyield

2

27

53

You knew it would be bad, but this is something: US

#leveragedloan

debt slides 2.73% today, far and away the biggest daily loss since the Financial Crisis (and nearly the largest ever). YTD: -4.48%

1

42

56

Cov-lite now accounts for 77% of all US

#leveragedloan

outstandings (in a $1T market, remember). That's yet another record

7

44

51

The riskiest US

#leveragedloan

issuers (B-minus) now account for the largest share of the $1.425 trillion asset class, the first time that's ever been the case. Full analysis:

@Kakourisr

#highyield

5

18

55

Ouch. Investors yank $3.3B from US

#leveragedloan

funds over the past week. That's yet another record withdrawal. The past two weeks: -$5.8B

4

41

50

With seven US

#leveragedloan

defaults in May (so far), that's nearly $10B in defaulted debt, the most for a month since TXU/Energy Future Holdings' massive $20B event in 2014

@Kakourisr

1

27

52

S&P expects US

#highyield

default rate to hit 12.5% by next March. That would mean 233 speculative-grade issuers would have defaulted. At the end of April the rate was 4.1%

3

23

49

Retail investor cash flood into US

#highyield

funds (cont'd): +$5.7B over past week, +$41.3B since April 1. The US

#leveragedloan

market, which did not see meaningful Fed support: -$15.6B YTD $HYG $JNK $BKLN

3

16

53

Purchase price multiples YTD on US LBOs now stands at 11.5x, topping pre-crisis levels. Private equity shops have been digging deeper for equity, however, keeping overall leverage on these deals relatively in check. Full analysis:

#leveragedloan

1

29

50

The number of "Weakest Links" - US

#leveragedloan

issuers rated B- or lower and on negative outlook per S&P Global - easily hit an all-time high in 4Q19. The biggest reason for the latest increase: Downgrades

1

19

49

US banks held roughly $99B in CLOs at the end of 2020's first quarter, with JPM, Wells, Citi carrying the bulk of that amount

#leveragedloan

@ajsaeedy

3

22

47

Coronavirus uncertainly has levels of distressed debt in Europe's

#leveragedloan

market at highest point since 2008. The rate of increase was record-breaking

@IsabellWitt1

0

28

48

Btw, the amount of outstanding US

#leveragedloan

paper rated triple-C topped $100B in April, thanks in large part to a torrent of credit downgrades. CLOs, of course, have limits on how much CCC debt they want to hold

#Covid_19

1

23

45

That's 18 bankruptcies among private equity portfolio companies so far in 2023, the fastest pace since 2020. One reason: The Fed has been raising rates (making debt more expensive), from near zero in March 2022 to 5.25% today

@PitchBook

#leveragedloan

1

14

43

Some $37B in US

#highyield

issuance last month, one of the busiest Aprils ever, as Fed's safety net to catch fallen angels bolsters market sentiment

1

30

42

S&P: Despite a relatively innocuous July the global corporate default tally has hit 91, more than double the amount at this point last year and well above the 10-year average.

#leveragedloan

1

18

43

Before the coronavirus, the probability of default for a US restaurant was 5%. Today, after lockdowns and a shuttered economy, it's nearly 25% per

@SPGMarketIntel

0

22

40

There were 11 defaults in US

#leveragedloan

market in April. That's the most ever. The default rate remains below historical norm, but with ongoing flood of credit downgrades and

#COVID__19

, investors are buckling up $

0

26

43

Today's 3.08% slide in US

#leveragedloan

asset class is largest ever, topping 2.9% loss in Oct. 2008. YTD: -7.76%

#Covid_19

0

21

43

Lower-rated deals (and covenant-lite transactions) are driving the loan market right now: (free)

2

33

40

Nearly three out of every four US leveraged loans are 'covenant-lite' (that's a new record)

5

37

40

Huge retail retreat from risk as US

#highyield

funds see $5.1B withdrawal (largest since 2/18, when market thought Fed might raise rates due to inflation); $2.3B redemption from US

#leveragedloan

funds (most since 1/2/19) $HYG $JNK $BKLN

1

23

41

A 3.65% loss for US

#leveragedloan

asset class today. That would be a record, if not for 3.74% slide yesterday. YTD: -17.9% $

1

31

38

Recent-vintage

#leveragedloan

defaults are indeed seeing lower recovery levels, as market bears had suggested, what with the prominence of cov-lite and other borrower-friendly deal structures during recent credit cycle

#highyield

0

20

39

Another huge drop in US

#leveragedloan

returns yesterday (0.47%), contrary to surge in equities. YTD the loan asset class is down more than 2% (again, most of that decline is from this month). Triple-C debt continues to outperform, somewhat.

2

15

38

Downgrade: Twitter, from BB+ to B-. S&P notes Twitter's leverage will spike due to acquisition and that advertising revenue is exposed to slowing economic environment and "modifications in content moderation"

#highyield

#leveragedloan

2

7

39

Lots of cov-light and EBITDA adjustment talk in US

#leveragedloan

mart but also of note is ever-shrinking debt cushion. A record 35% of loan issuers last year did so sans sub debt, helping bring debt cushion of all outstanding loans down to 20%. It was 29% in 2007.

0

20

40

S&P analysis: "When The Cycle Turns: The Continued Attack Of The EBITDA Add-Back" in front of paywall now. Check it out

#leveragedloan

#highyield

0

11

37

This year, covenant-lite loan issuance has exceeded high-yield activity by 41%, illustrating just how pervasive cov-lite has become: (free)

1

34

39

The ever-expanding U.S.

#leveragedloan

universe has stopped expanding. In fact, it shrank by $10B in July, the biggest drop in 10 years. Institutional outstandings (loans sold to CLOs/other non-bank investors) now = $1.19T

1

23

38

That's 223 corporate defaults globally YTD, led by US entities (143) and Oil & Gas concerns (50 worldwide, 35 in US). "If debt grows faster and income recovers more slowly than we expect, the surge in leverage would be harder to manage," says S&P Global

1

13

37

Maturities in $1.2T US

#leveragedloan

market are relatively light until 2024, when some $264B of term debt will come due (unless it's refinanced, of course). Full analysis:

0

9

34

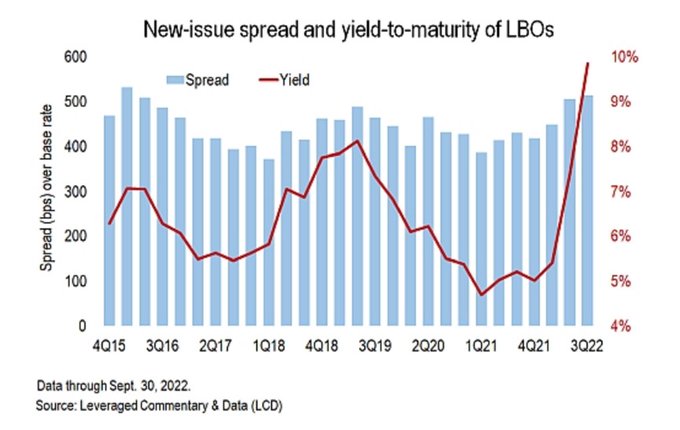

How deep are U.S.

#leveragedloan

issuers having to dig to complete credits in a market that remains wary of risk? Very. Yields on single-B rated new-issue loans now top 10%, more than double what they were one year ago

#highyield

1

17

35

As investors/CLOs worry about downgrades, 58% of the $1.2 trillion in outstanding US

#leveragedloan

debt is now rated single-B or lower. That's the most ever. And over past 2 years the share rated B-minus has doubled, to 14.75% (another record)

0

26

37

A Chapter 11 filing by McDermott Int'l sends US

#leveragedloan

default rate to 15-month high of 1.64% (from 1.39%). With $3.6B of sec'd debt outstanding McDermott is largest bankruptcy in loan mart since iHeart in 2018

2

12

36

More from LCD's 'Weakest Links' analysis: With help of recent credit downgrades, the share of $1.2T US

#leveragedloan

market with riskier, B-minus issuer rating soared in March, to record levels (triple-C debt spiked, too)

0

8

37

A new record: 79.6% of the $1.8 trillion in US

#leveragedloan

outstandings is cov-lite. That's about $940B. The bulk of that ls riskier debt, from issuers rated B and B-

5

26

36

With seven US

#leveragedloan

defaults in May (so far), that's nearly $10B in defaulted debt, the most for a month since TXU/Energy Future Holdings' massive $20B event in 2014

0

13

35

With LIBOR rising, cos. with lots of floating-rate debt lag behind broader stock market

#leveragedloan

0

33

32

US corporate debt now totals close to 50% of GDP, per the Fed and Commerce Dept. That's a record.

@WSJ

@RachelEnsignWSJ

2

27

33

With four defaults in January, US

#leveragedloan

default rate is now 1.83%. That's the highest it's been in 15 months. Again, the historical average is 2.9%, so ...

1

19

33

US

#leveragedloan

default rate increases to 1.48% in November, highest it's been in 9 mos. Though - altogether now - it's still well below the historical average (2.9%)

2

14

33

Still riding

#Fed

tailwind, US

#highyield

bond market just wrapped its busiest May ever (and busiest month since 2013): $43.8B of issuance. YTD that's $153B, a tidy 48% increase from 2019 pace

@JakemaLewis

2

15

33

Commodities default rate, from S&P Global's 2Q European Corporate Credit Outlook

0

33

33

August is usually a sleepy month for the US

#highyield

bond market. Usually ...

@JakemaLewis

0

13

31

A grim 2Q US

#leveragedloan

market, in 6 Charts:

1) Worries over inflation, war in Ukraine has many investors fleeing risk, driving loan trading prices to lowest levels in nearly 2 years …

3

10

31

US

#leveragedloan

default rate increases to 1.48% in November, highest it's been in 9 mos. Though - altogether now - it's still well below the historical average (2.9%)

1

15

31

Retail investors withdraw $3.53B from US

#leveragedloan

funds. That's yet another record, and helps wipe out gains seen throughout the year (the final 2018 number: a $3.1B net outflow)

0

19

30

There were 44 Potential Fallen Angels in January, per S&P Global Ratings. There are record 126 today. No surprise: The bulk of these entail "sectors most exposed to COVID-19-related social distancing measures." And oil & gas. $

0

17

31

What with private credit cutting an increasingly wide swath in the US

#leveragedloan

space, the share of non-syndicated credits in BDC portfolios is surging. Most private credits are unrated, as opposed to broadly syndicated deals.

1

12

28

2

20

30

The share of US LBOs leveraged at 6x - a magic number, per the Fed -

just hit its highest level since the financial crisis

0

25

30

The 4Q US

#leveragedloan

market, in six charts ...

What was a frigid 3Q syndicated loan segment thawed enough to allow some opportunistic activity (refinancings in this case. Dividends still weren't a thing in 4Q) ...

1/6

2

3

30

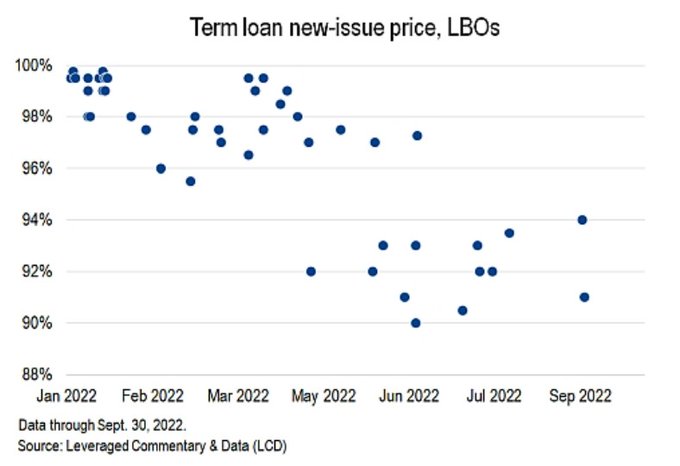

An eye-popping aspect of the recent US

#leveragedloan

market: New deals clearing market are doing so at serious discounts, sending borrowers' all-in rates soaring. Single-B new issues priced at an average of 92.75 in July, after plunging from 99.5 in January

0

9

28

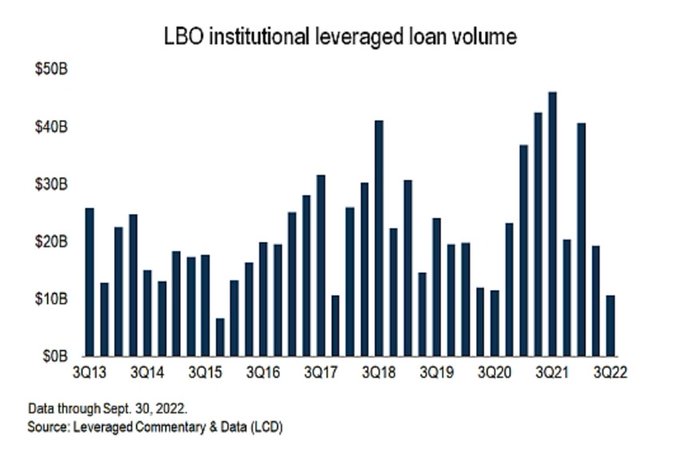

Leveraged loans backing LBOs dried up in 3Q as investor appetite for risk disappeared. Indeed, the cost of LBO financing skyrocketed in terms of interest rates (

#leveragedloans

are floating rate) and re deep discounts on the debt. Much more:

@PitchBook

1

10

28

The Distress Level - the share of $1.2T in outstanding US

#leveragedloan

debt priced at less than 80 cents on dollar - has decreased to 20%, from high of 57% on March 23 $

0

24

29

Here's the full analysis:

#leveragedloan

downgrades are mounting, and CLOs are keeping a watchful eye, as they are limited in how much triple-C paper they can hold

@apark_

1

16

28

The 3Q US

#leveragedloan

market, in six charts …

In a risk-off market it was a new-issue desert, with volume plummeting, borrowing costs soaring and terms tightening

1/6

1

8

30

The default rate among private credits continues to tick higher, reaching 4.5% in Q1, from 4.2% a quarter previous, says Lincoln. Defaulting most frequently: businesses in the Consumer segment

#leveragedloan

1

12

29

So. Over the past 7 days, the US

#leveragedloan

market is down 1.1%. That's the steepest one-week drop since 2011 (per the S&P/LSTA Leveraged Loan Index)

3

19

28

Relax . . . CLOs are nothing like as menacing as CDOs

@FT

@BondHack

#leveragedloan

... And for the record, we're at €27.8B of European issuance YTD, the most ever, per LCD

1

7

30

The

#highyield

segment of US leveraged finance market continues to see momentum, with investors pouring record $7.7B into funds/ETFs last week. YTD: +$238M $HYG

1

21

29

One thing about the Fed's Main Street lending programs: Many issuers comprising the $1.2T US

#leveragedloan

market carry too much debt to qualify for it

1

17

29

Cov-Lite Deals Account for Record High 85% of Single-B Issuance YTD: (free)

0

27

27

Yesterday's 2.73% slide in US

#leveragedloan

market was epic indeed, far outpacing any loss since Financial Crisis, including during US sovereign debt downgrade/debt ceiling days

#COVID

ー19

0

23

28

The $2.53B withdrawal from US

#leveragedloan

funds this week? The largest on record. YTD: +$3.7B

2

30

28

For the record: The covenant-lite share of the $1.193 trillion US

#leveragedloan

market hit 80.8% in January, the most ever.

0

15

29

The share of triple-C debt in $1.18T US

#leveragedloan

mart now stands at 7.34%, the most since May 2017. This is of key interest to CLO investor base, which historically has had limited capacity for CCC risk

0

16

29

The US

#leveragedloan

default rate crept to 1.75% in July after Juice Plus and its lenders agreed to scrap principal amortization payments for 1 year and fruit grower Prima Wawona skipped interest payments. Over the past 12 months there has been $24.7B in loan defaults

@kakourisr

1

7

28

How hard has pandemic hit US

#leveragedloan

market? Through May roughly 1/3 of $1.2T in outstandings have been downgraded. That means lots, lots more triple-C debt. Full analysis:

@Kakourisr

0

11

28

Retail investors pull $4.2B from US

#highyield

funds this week. Biggest redemption since Oct. 2018. YTD: $1.9B net withdrawal $HYG $JNK

#COVID2019

0

13

28

Covenant-lite issuance in US leveraged loan market hits (another) record high in 3Q 2017

0

19

28

Btw, the amount of outstanding US

#leveragedloan

paper rated triple-C topped $100B in April, thanks in large part to a torrent of credit downgrades. CLOs, of course, have limits on how much CCC debt they want to hold

#Covid_19

0

18

26

Triple-B debt - the lowest rung of investment grade - now totals some $3T.2, more than 2.5x size of entire speculative-grade market, says S&P GFIR ($)

1

22

26

Lots of attn on plunging US

#leveragedloan

market now, so some context (some will see these numbers as problem, others as opportunity) -

Per the S&P/LSTA Index

-Share of issues priced at 80 or lower (a common measure of 'distress') is ~2.27%

2

15

24

Triple-B issuers - which are loading up on debt - make up nearly half the investment grade bond market

0

25

27

The distress level in US

#leveragedloan

market is easing. It's still elevated, but way down from 54% only two weeks ago $ Distress = loans priced at less than 80, per S&P/LSTA Loan Index

@Kakourisr

0

13

26

Another month, another record-high amount of covenant-lite loans in US leveraged market

2

21

25

For the record: The covenant-lite share of the $1.2T US

#leveragedloan

market is holding at 79%. That's about $950B

1

19

26

That's 133 global corporate defaults so far in 2016. There were 113 in all of 2015 (free)

0

36

25