Andy Mychkovsky

@healthcareandy

Followers

19K

Following

5K

Statuses

4K

Tweets about the $4.5 trillion U.S. healthcare system | Join 7,000 newsletter readers here: https://t.co/4uotjdkYc4

👇Join 7k Healthcare Readers

Joined August 2018

81 million jobs pay under $20/hr. They can’t afford Tesla’s, Pelotons, or Sweetgreen salads. They can’t convert conference calls to walking calls. And they can’t afford housing or healthcare. We need startup ideas for all Americans, not just the top quartile.

77

292

2K

Just a reminder, you don't have to post a "hot take" about a tragedy for clicks. It's okay to let the families and friends involved mourn in peace.

1

3

16

@chrissyfarr VC is a high risk, high reward game. It should be solely up to the founders discretion whether to continue on or give up. Those are the only people spending 7 days a week trying to make everything work.

0

0

2

Those celebrating RJK Jr.'s appointment to HHS Secretary must realize vaccines are a small part of the FDA, which is a small part of HHS, and food is governed by USDA, which falls under the Secretary of Agriculture. He'll be buried in the minutiae of Medicare & Medicaid funding.

9

5

52

The buyer of HLTH is reportedly Hyve Group, an international events company now owned by private equity. The deal terms were not reported, so we’re not sure if I was right about the $100M+ exit valuation or not. But I bet I was… We do know Hyve purchased a much smaller conference (POSSIBLE) that had 3,600 attendees in July for a rumored $40M. By all accounts HLTH + ViVE is significantly larger and more global. One important fact about Hyve is that in June 2023, Providence Equity and Searchlight Capital Partners agreed to buy Hyve at £524 million ($660.24m). This is a events roll-up platform strategy to increase multiple arbitrage, streamline back-office, and increase vendor negotiation leverage. Before acquiring POSSIBLE and HLTH, Hyve was estimated to have generated £165.4 million revenue in 2023. Regardless, this was all inevitable in my mind. Just good business sense. If I was in the events business, I'd try to do the same. Just my two cents.

HLTH is being acquired, just like I predicted in 2023. They followed the “sell picks and shovels during a gold rush”strategy, except it’s selling a well executed conference to a growing health tech industry that loves conferences. Will be curious if deal terms are released.

0

4

9

HLTH is being acquired, just like I predicted in 2023. They followed the “sell picks and shovels during a gold rush”strategy, except it’s selling a well executed conference to a growing health tech industry that loves conferences. Will be curious if deal terms are released.

The HLTH / ViVE conference business could probably sell for $100M+. It’s an absolute masterclass of how to grow a conference/trade show. 1. VCs actually invest in HLTH 2. VCs recruit startups to attend 3. Startup founders get to speak 4. FOMO drives attendance 5. Bigger speakers are announced 6. Attendance drives sponsors 7. HLTH puts on great event 8. HLTH increase from 1 event to 2 per year by adding ViVE. The only thing missing would be a parallel strategy that is purely digital and driving high margin subscription or advertising fees.

3

7

36

Over the next 12-18 months, I’m watching who gets acquired / merges. And when that happens, who makes the money between early stage investors, late stage investors, and founders? Liquidation preferences are going to become very important, since preferred shares get paid before the common stock (aka: founders and employees) on the cap table. There are plenty of companies that are unprofitable, have under 20% growth rates, and have already raised 8-9 figures of funding. I’m sure plenty of those private conversations are occurring at #HLTH this week. Will be interesting to see how this all evolves.

2

4

9

With Elevance Health’s announced acquisition of CareBridge, I predict home based care will be the hottest M&A market over the next 5 years. Big deals are coming. One important nuance, but I believe only the home based companies that serve Medicare patients will yield the highest valuations. Cash pay organizations have smaller upside because majority of aging Americans have limited resources and capital. The challenge for entrepreneurs is that these types of organizations are challenging to scale and require immense regulatory expertise. Also, the unit economics are not SAAS-like, so you have to thread the needle on sustainable growth and unit economics. If you’re building, just keep going. Many of the existing players offer a subpar patient experience that can be improved upon. It just takes time for the physician and patient community to notice. p.s. Brad Smith is quietly (or maybe not) becoming one of U.S. healthcare’s top entrepreneurs. First Aspire, now CareBridge. - - - - - Image credit: Forbes

5

10

35

On August 5, 2015, Walgreens’ stock peaked at $96.68. Today, that same stock hovers around $10 per share. This occurred during a 9-yr period where U.S. healthcare expenditure rose by $1.5 trillion. Expensive real estate, soft retail sales, labor shortages/high turnover, increased shoplifting, no true PBM/health plan partner, and low drug reimbursement are all issues to be addressed. Walgreens does hope to cut $1 billion in cost (which includes closing 1,200 stores), but that’s not really a long-term growth solution. I’m afraid that Walgreens has entered the retail pharmacy endgame and we’ll see if they have their own Iron Man.

5

4

8

Oura ring generates nearly $500M revenue. As a non-user, I was surprised to hear of their scale. Whenever I research how large niche, health-related devices, products, or services can become, I’m reminded how shockingly large the world actually is. The interesting tailwind for these types of companies in today’s world is shift towards “personalized health” and “longevity”. I haven’t researched these tracker devices, but I know people love them. When it comes to other regimens, it’s hard to say if any of it works because no one that professes a certain health regimen is actually elderly. I encourage people to experiment, but cautious about being devout at this time. I for one try to practice the 80-20 of normal, balanced stuff. Try to eat healthy, exercise, sleep, and reduce stress. Maybe I won’t live as long as humanely and scientifically possible, but I’m alright with the that trade off. Regardless, I do believe mortality and morbidity will be the focus of many entrepreneurs in the next decade. And I hope we make some incredible breakthroughs that deliver scientifically proven better results.

0

5

14

Unfortunately, I think many DTC virtual clinics + cash-pay, mail-order pharmacies have a tough road ahead. This is all about the mismatch between the VC investment thesis (5-10x valuation increase from latest round) and what is likely a realistic exit outcome for this archetype right now. We know what best-in-class looks like for a DTC virtual clinic + cash-pay, mail order pharmacy: Hims & Hers Health worth $4.6B. They've seen strong investor interest lately, especially related to their GLP-1 compounding initiative. Hims' full year 2024 guidance is $1.20-1.24B in revenue. That represents a 3.7x forward revenue multiple. The challenge is that many smaller DTC virtual clinic + cash pay, mail-order pharmacies raised significant funding in 2020-2022 and now have high exit expectations. Once you raise significant VC funding (series a and beyond) and dilute the cap table, it's really hard to pivot to a sustainable, cash-flowing business. For example, after an angel, pre-seed, seed, and series a round, the founders may own ~50% or less of the company. By this time, there's already a formalized board in place with $1B+ exit expectations. Now if we were talking about DTC skin care, frozen food, or clothing, there's a tried and true pathway to exit the business to a $100B+ conglomerate CPG brand for 8-9 figures like Unilever, P&G, PepsiCo, Nestle, LVMH, or Coca Cola to name a few. The problem is that unlike traditional CPG, DTC health is much smaller and younger. Instead of P&G (worth $398B) or Unilever (worth $143B), the largest acquirer may be Hims at $4.6B. And now that Hims is publicly traded, they may prefer an acquisition that is net income accretive at a reasonably low multiple (1-2x revenue). And they also would have to believe it's not a product/service they could do internally. The $100B+ players in healthcare like UnitedHealth Group, CVS, McKesson, or HCA don't appear to be interested in acquiring niche DTC virtual clinics + cash pay, mail-order pharmacies at this time. Especially hard when their cash yields 5% risk free and the market optimizes for earnings per share. DTC is not their core business and given their mature revenue scale, adding 8 figures of revenue does little. Now the holy grail for these DTC virtual clinics + cash pay, mail-order pharmacies is either a) go public; or b) get bought by a consumer juggernaut that likes healthcare (aka: Amazon). The only issue with Amazon is given the recent dept consolidation news, seems like they're still digesting PillPack and One Medical. The other option of IPO'ing is hard because bankers want to see a $1B+ valuations. If we use Him's 3.7x forward revenue multiple, another DTC virtual clinic + cash pay, mail-order pharmacy needs ~$270M annualized revenue w/ similar margins. That's brutally hard to achieve that scale when growth-stage private funding has dried up for DTC. But this is just my two cents. And I could be wrong, wouldn't be the first or the last time. Thoughts?

5

8

32

I know someone hiring a contractor for market research / competitive intel for a top digital health company. If it's you, email your resume to Andy@healthcareandy[dot]com If it's not you, like this post so more people see it and refer your friends. Hours are ~20 per week and hourly pay is competitive (i.e., $60-90/hr depending on experience). You will work with the person who leads competitive intelligence to inform sales, marketing, and product. Must be comfortable researching, summarizing, and presenting information to a wide range of stakeholders. Perfect for someone not looking for a full-time commitment, but wants to work with high performing team members. You can work remote and working hours are flexible for all you night owls. Also, don’t be shy about applying. You don’t necessarily need a lot of years of experience. Just be smart and work hard. As you all know, I rarely recommend jobs to people. Also, I’m not being paid any referral commission, just helping out the community during this tough job market. Last reminder, please don’t LinkedIn message me your resume. Send to my email. :) I expect this one to go quickly. Good luck to all the candidates!

1

4

10

Now 2 medical schools have received $1B donations to make tuition free. 1. Albert Einstein College of Medicine 2. Johns Hopkins University Michael Bloomberg just donated $1B to his Alma mater, making that a total of $4.55B. Surprised it’s not called Johns Bloomberg University at this point. Johns Hopkins was already ranked No. 2 in Best Medical Schools. I can only imagine the flood of qualified applicants for 2026 when $300k of debt is actually $0. Now to be clear, this is incredibly generous and I hope those future doctors can focus on lower-paying specialties if they want. But given the incredible strength of JHU on the sub-specialties, not sure what will happen. One random observation is that there are ~160 accredited medical schools in America and 240 billionaires who signed the giving pledge. It feels like this type of legacy donation is going to pickup momentum. So if you’re considering school, maybe take that gap year until more billionaires follow suit. 😀

3

5

24

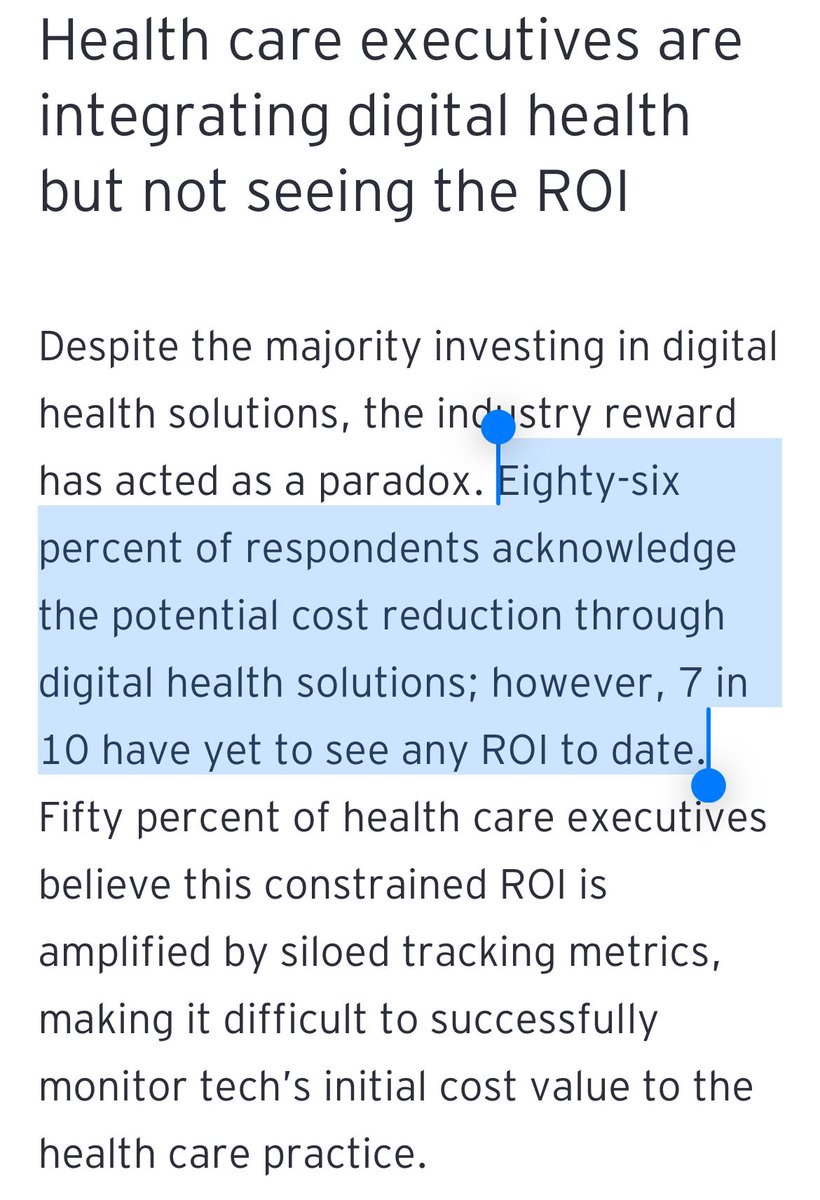

70% of healthcare execs haven’t noticed true cost reductions/ROI when implementing digital health solutions. These results comes from an EY Health Pulse Survey, where 100+ payer and provider execs were asked about the state of digital health. I’m not going to sugarcoat it, these are not great results at face value. In order for digital health to persevere over the long-term, we need bulletproof ROI, net of the digital health fees. Super hard to measure when ROI includes "productivity" or even "ER visit reductions" because there's a million reasons someone goes to the hospital for chronic and acute issues. Now to be clear, I'm not a digital health hater. We’re still “early-ish”. We can’t forever use that excuse, but the industry is objectively young relative to the size and complexity. And like I've said in the past, optimism is the only pathway because pessimism leaves us with the status quo. For me, I continue to believe site of care savings is the most predictable and reliable strategy to focus on. That’s why I believe home-based care for certain services is the correct approach. The problem with home is that unit economics can be challenging, logistics are very complex, and not every patient treatment should be done at home. But others have different opinions (investments or companies they work for). What do you think?

16

14

56

@halletecco Despite commentary I post online, the only way to proceed is blind optimism. Otherwise we’re forever stuck with the status quo.

1

0

5

@dawallach @bgurley True. But that’s seems like a risky exit strategy to build a company. Only so many will get the “goodwill” bump after all the post-M&A impairment issues.

1

0

0

@RojaGarimella I misunderstood. Yes, for lower market brick and mortar medicine (specialists, ASCs, home health), I agree the investor class views them as commodities (as crude as that sounds).

1

0

0

@RojaGarimella I still think investor appetite is higher for care delivery because healthcare acquirers are willing to buy companies at higher multiples for strategic value (not only financial metrics).

1

0

2

@anthonychu_do Ha, concerned about the viability of the sector, not worried about investors putting food on the table.

0

1

2