Mikro Kap David

@david_katunaric

Followers

8,682

Following

423

Media

1,029

Statuses

5,489

turning over micro rocks and sharing my discoveries || there's always a cheap market somewhere || not investment advice

🇭🇷

Joined April 2021

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

North Carolina

• 934113 Tweets

Hurricane Helene

• 770830 Tweets

FEMA

• 406051 Tweets

Starlink

• 186857 Tweets

Dikembe Mutombo

• 165501 Tweets

Mets

• 140415 Tweets

Verizon

• 100299 Tweets

Game 2

• 88269 Tweets

Diaz

• 86499 Tweets

Lübnan

• 84637 Tweets

#النصر_الريان

• 73536 Tweets

Braves

• 70933 Tweets

Kemp

• 56223 Tweets

Franklin Graham

• 52509 Tweets

#KızılGoncalar

• 44843 Tweets

MANTRA IS COMING

• 33719 Tweets

Lindor

• 27745 Tweets

رونالدو

• 24364 Tweets

Zeynep

• 23392 Tweets

İsrail

• 22287 Tweets

الجيش اللبناني

• 21949 Tweets

Lorenzo

• 18031 Tweets

Gavin Creel

• 15911 Tweets

#الاجتياح_البري

• 15770 Tweets

Southampton

• 14424 Tweets

Bournemouth

• 14193 Tweets

تاليسكا

• 10911 Tweets

Ozzie

• 10530 Tweets

Cüneyd

• 10387 Tweets

Pinned Tweet

If you're interested in going outside of Wall Street, here are 15 indicators I frequently use to detect illiquidity and obscureness

1) low free-float adjusted market-cap

I prefer market caps of below 100M. However, a 350M company like $RCS.MI, which is 75% owned...

9

25

156

Is there a better investing resource than the class notes from Greenblatt’s Special Situations Class at Columbia

No, I don't think there is

16

43

579

~19 years ago, Priceline acquired Booking for 135M in cash

Priceline is now called Booking Holdings and generates vast majority of its 21B in sales and 4B in net income from bookingcom

Probably top 3 acquisitions of the 21st century, yet it's not talked about often enough

$BKNG

9

43

482

Greenblatt grading student papers in '05

"To take 12 x EBIT you would want to be pretty certain of the business and the growth. I wouldn’t throw those numbers around so lightly."

Imagine saying this to a compounder bro today, who thinks 20x EBIT is the opportunity of a lifetime

12

24

307

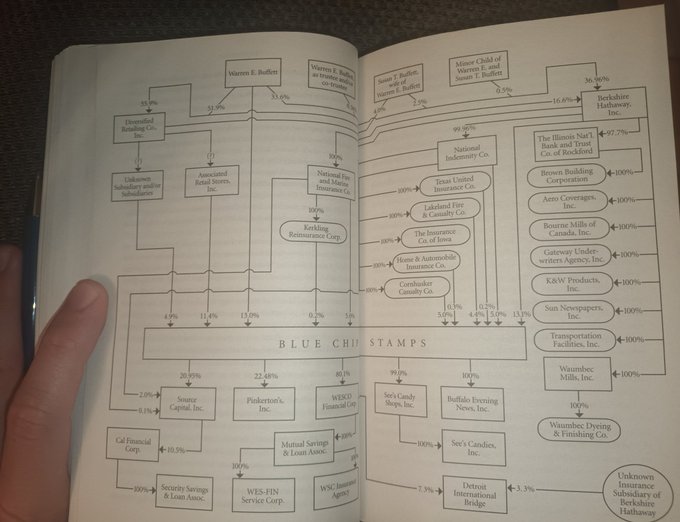

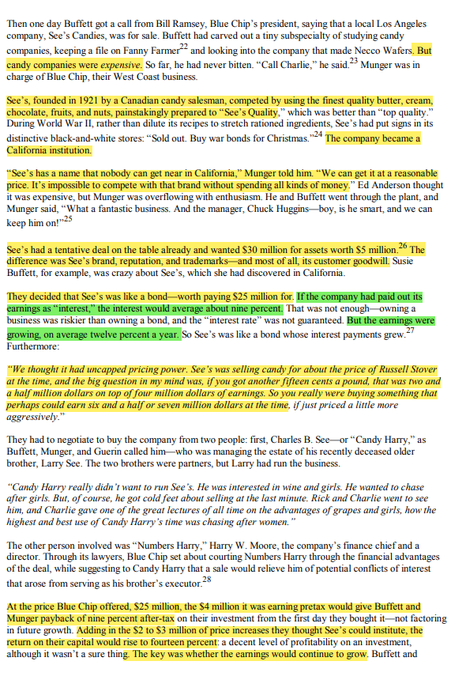

Tb 1975, when Buffett and Munger were running a Ponzi😉

18

17

264

No-brainer idea alert🚨

1/ $RCS.MI is a close-to-wonderful business at a wonderful price.

With an EV of 300M, 130 M in TTM free cash flow, a dividend yield of 9.5%, and valuable intangible assets, this is an opportunity that value investors shouldn't overlook.

18

26

212

I don't know (I do) who needs to hear this,

but this is what Buffett meant by buying a wonderful business at a fair price

11xP/E, 12% historical grower, and most growth is capex-free

3.5-4x PBT after anticipated price-increases

Beautiful.

11

20

209

🧵I always get a little irritated when investors quote Buffett’s “It's far better to buy a wonderful company at a fair price than a fair company at a wonderful price” as an excuse to buy $NFLX at 40x earnings or $MSFT at 12x revenue

In his most successful days, young Buffett...

19

26

199

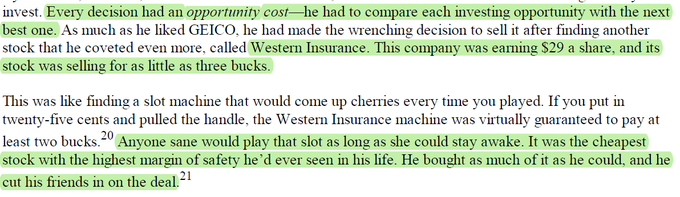

Funny how GEICO, one of Buffett's greatest investments ever, was actually a gamble

And could not be pulled off without much luck or activism

11

20

181

🧵Alibaba brain dump

As much as my stance on Chinese companies has gotten increasingly more bearish over the years and the e-commerce market there has gotten more competitive. I still got to hand it to $BABA’s management team.

I’ve been following the story for a while now and..

5

27

178

Just finished Capital returns, and my Top 3 needed to be updated

1. Columbia Class Notes

2. Capital Returns

3. Gannon Compilation

These will be my re-reading friends for a long, long time

10

12

176

According to comments, here are 8 micro-cap CEOs who receive little notice yet should be admired

Thank you for pointing it out🫡

13

8

158

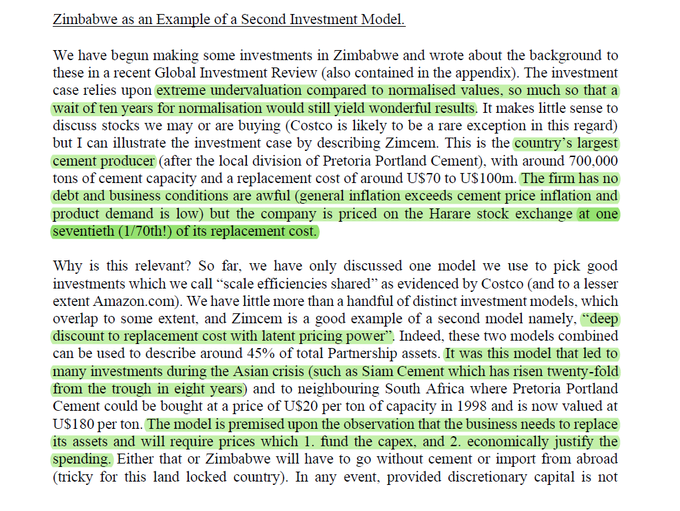

What is today's example of Nick Sleep buying a cement producer at 1/70 of its replacement cost?

Examples of "deep discount to replacement cost with latent pricing power"🏢

18

21

144

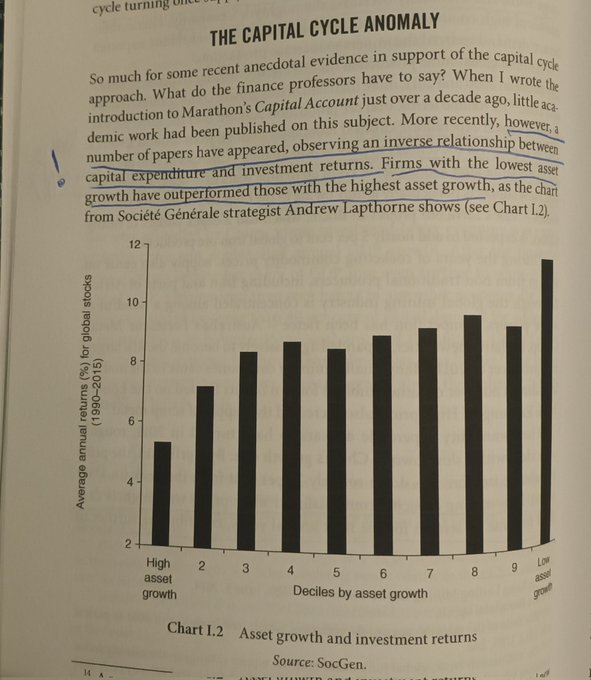

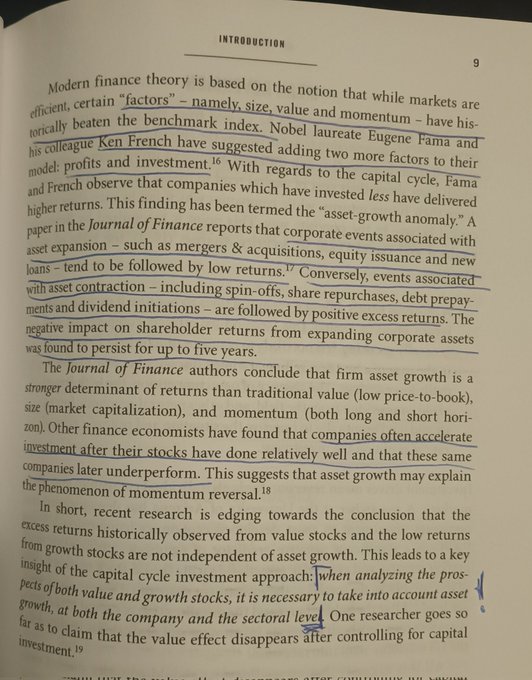

Reasons why high asset growth underperforms

via Capital Returns

15

15

142

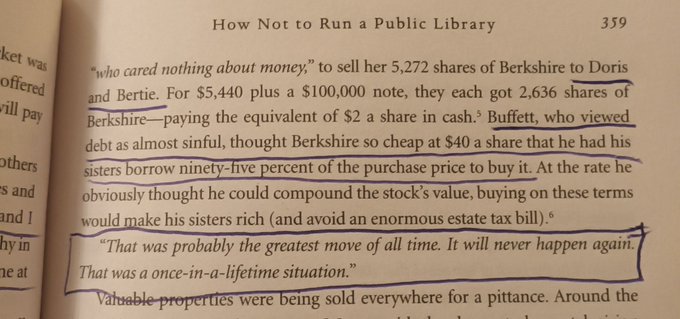

Atm, what's one stock that is so attractive that you'd make your two sisters lever up 95% just to buy as much of it as they can❓️

A 1974 Berkshire equivalent

13

7

130

I'm not a fan of deep dives or lengthy investment write-ups, however,

@JonCukierwar

's $DNP.WA research is one of the most impressive things I've read in a long time

It got me very biased. Not gonna lie

8

11

125

You thought it was a boring Sunday. You were wrong!

Today marks the anniversary of $FINTWITDARLINGS portfolio🥳

If you have no idea what I'm talking about, here's the long story short:

For curiosity's sake, I've started tracking the performance of fintwit favorites (based on

33

11

119

I have never seen so many red flags in a 2-minute video before

🚩.

Birkenstock CEO Oliver Reichert discusses how he plans to keep the brand relevant after it begins trading Wednesday.

@SquawkStreet

10

7

36

16

5

113

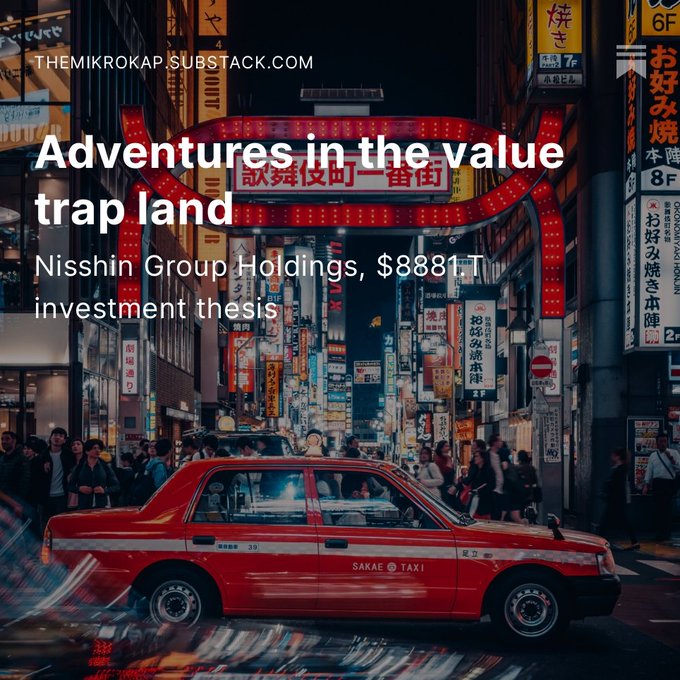

🧵If anyone's looking for ideas in the value trap land called Japan. Here's one non-value trap called Nisshin Group🇯🇵

$8881.T is a Japanese net net that's actually a stable value-creating business with improving capital allocation at play, selling for 0.45x P/NCAV and 0.35x P/B

5

13

115

Hey, Warren. What are you buying today?

Well, I found this company that is selling for 0,1x P/E. Seems like a decent setup

11

11

109

A detailed piece outlining the risk-reward of my new 12% position in $ALCO has just hit your inboxes

12

8

108

Even in the MID-cap land, 20–30 cent bills can sometimes yield a dollar

My latest piece on $PARA is out!

Be sure to check spam or go to the website version because this is a lengthy one

12

12

105

Once you read all the classic investing/biz books and built a habit of reading 10K-s every day

What's the best return on invested time? How can one continue to improve as an investor aside from the obvious repetition of the same old practices?

Would love to hear your thoughts

49

5

99

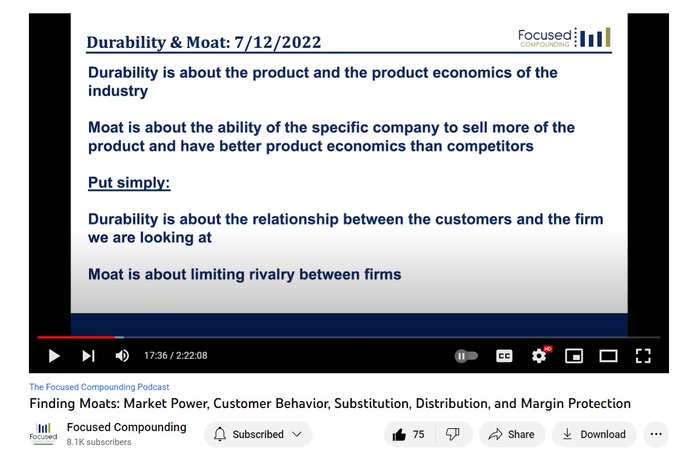

1/ Every now and then, you get lucky and stumble upon evergreen content🌲

The "Finding Moats" episode by

@FocusedCompound

precisely that. It makes you see business through a different lens🔍

There is probably no better way to spend two hours learning about...

2

13

90

For curiosity's sake, I've decided to start tracking the performance of fintwit favorites (based on my feed experience)

Here are 20 darlings that I will equally weigh at 5% and then check their performance over a one and three-year timeframe

Feel free to give me some

37

3

87

Easy

Apparently, all men have a favorite historic battle. Spill it, gents.

738

14

425

2

8

85

1/ IMO most investing books are just a form of mental masturbation

We all lead busy lives, and once we've read "the classics", our time is far better spent by actually reading the 10Ks and Qs. Turning over rocks, applying the knowledge, playing the game & learning from mistakes.

12

4

87

Never expected I'd receive such a wonderful comment as this one♥️

Makes me want to either tear up or frame it on the wall above my bed

0

0

86

$BIG is a high-risk, higher-reward idea that I believe will appeal to diversified investors looking for bets where the odds are in their favor

🧵🧵

10

9

81

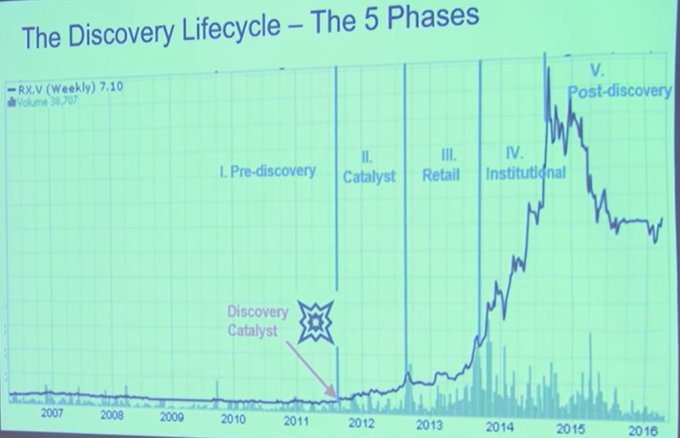

1/In 2016,

@Moatology

and

@PaulAndreola

gave a presentation that every investor operating in the microcap space should watch

If I had to sum up their presentation in one line, it would be

"You Can Be a Stock Market Genius - Microcap edition."🧵

1

18

85

The nice thing about this bloodbath is that we probably won't be seeing any more of "YTD brag tweets" from accounts who only choose to "disclose" performance when it suits them and who sweep their bad years under the rug

And there are so many, and they have so many 💩 years

4

3

81

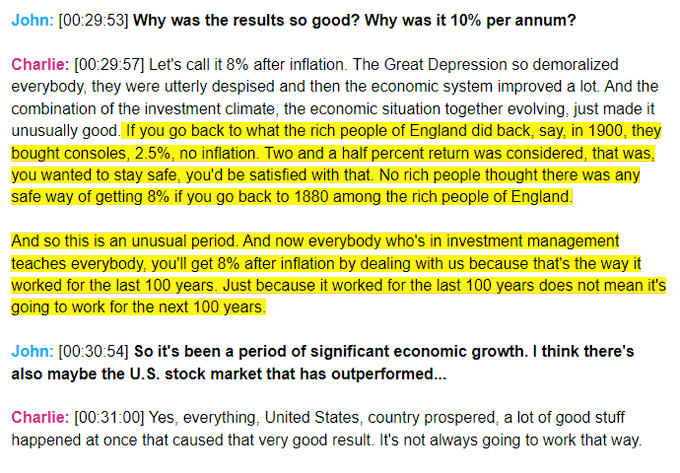

Also, one of the final things Munger has said publicly

Expecting 10% as a given is more than dangerous

2

8

78

Is Poland a fertile ground for new ideas?🇵🇱

Please give me some interesting micro names🙏

(a 1-2 sentence pitch would be ideal)

30

8

79

Nov 2008

A clip of Alice Schroeder discussing Buffett's rationale for his private investment in Midcontinent Tab Card Company

One of the few times he had the opportunity to buy a "Phil Fisher-type growth company at a Ben Graham-like price"

Result? 33% CAGR over 18 years😴

4

9

80

1/ Industrial bros, take a look at this

$HYDRA.AS is an industrial holding company that trades at ~3X LTM FCF

Insiders own nearly 80% and have a strong M&A track record

Otherwise, the business is stable, its gross margins are high and growing, and it appears to be insulated..

7

5

78

Hello

I spent the day weighing in the probabilities and determined $PARA is still a worthwhile bet

However, I'm not as comfortable with the risk-reward as I was just two days ago

I sized it smaller this time and bought back half the position I sold yesterday, so 8% of my total

14

1

75

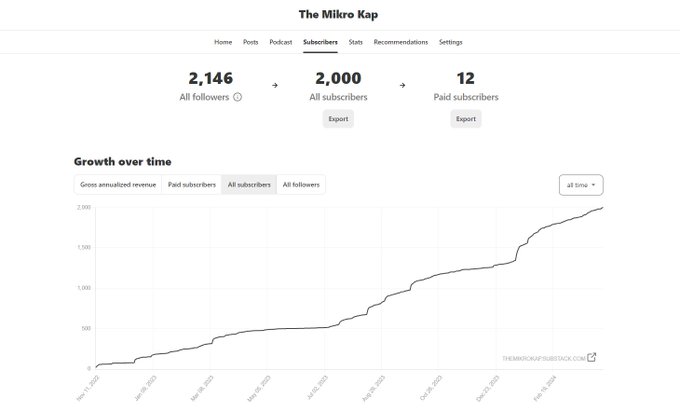

Wow❗️

18 months of casual writing for my blog has attracted an audience of over 2000 readers

I'd like to thank every single one of you! It is truly an honor to have such a large network of like-minded investors providing excellent feedback, both in the comments and in the DMs

12

3

73

Thanks to the feedback I’ve received from one of my followers, I sold my $CARD.L position

Card Factory’s accounting for reporting discounted leases on the balance sheet is super aggressive, and I should have taken the approach of calculating annual lease cash costs instead of

13

1

72

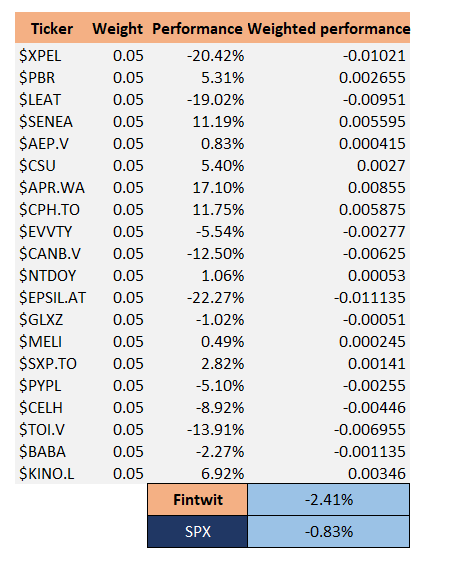

Following the $XPEL plunge today, I've decided to check how the fintwit favorites portfolio has been performing since my tweet on Aug 25

$SPY -0.83%

$FINTWITDARLINGS -2.41%

I expected worse, but I expect worse going forward

...quietly hoping fintwit proves my arrogance

18

8

70

With "markets in turmoil" and everyone posting timely content on Fintwit

I figured, why not be the one to post something timeless for the team today. Something evergreen

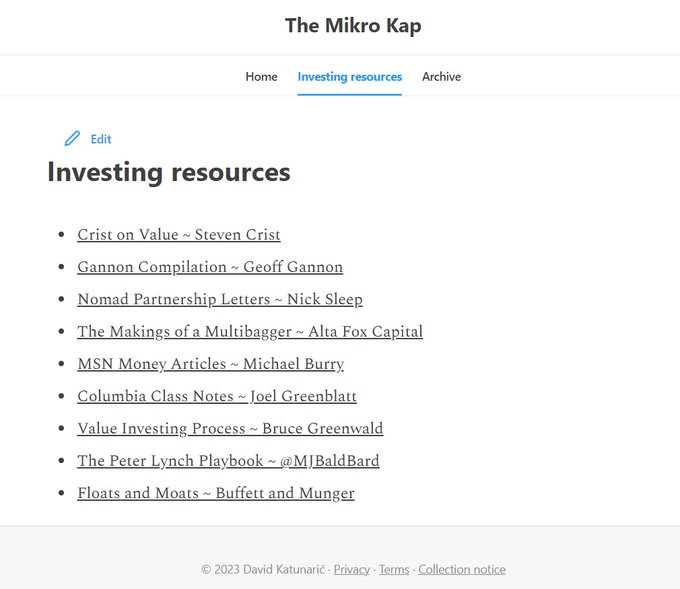

Here are, IMO, 13 of the best free investing resources you can find online at one place

Check them out❗️

3

11

70

Heading into Easter weekend with 0 cash and a bunch of deep-value

8

2

69

Today I learned that L'Occitane is listed in Hong Kong because they thought they could get a higher multiple there back in 2010

Fast forward to 2023; fintwit is pitching me P/Es of 4-5 in HK on a regular basis

How times have changed

7

1

66

Now that none other than Will Thorndike, author of The Outsiders, is involved with Lindbergh $LDB.MI, perhaps it's time to remind people that Lindbergh's CEO Michele Corradi gave an interview for The Mikro Kap this October

So if you want to learn more about him or the company he

5

7

63

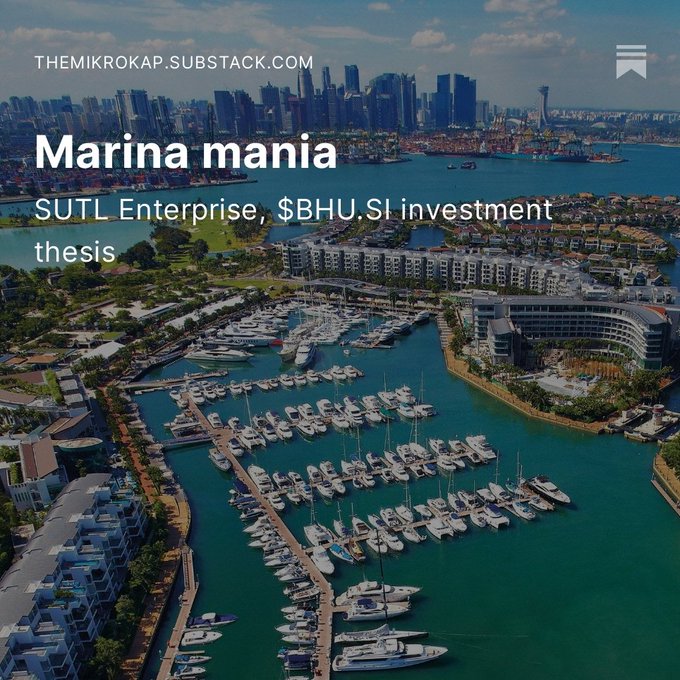

A piece on my new 20% position has just hit your inboxes🇸🇬

$BHU.SI

8

4

63

A piece on my No.1 Japanese Net-Net has just hit your inboxes🇯🇵

$8881.T

1

4

63

I don't want to interrupt your peaceful Saturday

But a new piece, diving deep into $MSV.AX transformation, is out at the usual place

2

4

63

Guys, I was trying really hard not to look

But Mag7 baffles me.

How does a company add >500B in market cap in a month while doing only 27B in revenue LTM?

It would take f*cking 19 years of revenue in order to cover that YTD market cap gains

$NVDA

13

4

62

Exceptional newsletters written by great investors

Hunting for asymmetric risk-rewards and putting in the extra effort that others aren't willing to

Thank you, fellas. Cannot recommend enough❗️

6

7

61

There's something so liberating when 99% of micro-cap Fintwit couldn't care less about your picks, but the 1% that does care has actually done impressive, or dare I say autistic, level of due diligence

To the 1%, I salute you

0

0

59

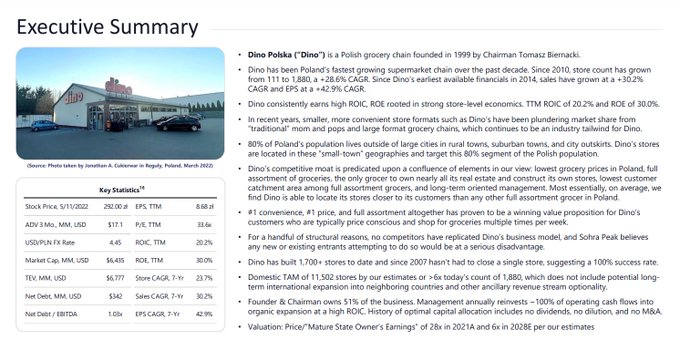

beautiful Croatia, beautiful balance sheet

(for a 48M market cap)

7

1

60

Seeing so many complaints surrounding $PARA in the last couple of weeks, it truly feels like a "darkest before dawn" scenario

Glad I can handle volatility and am young enough to own it in size

Earnings tommorow. Will delete if I'm wrong🦧😉

7

0

56

Disc:

I am taking a loss and will sell my $PARA stake when the market opens today.

Bronfman is out of the race, the go-shop period is over, and the "dilution under Ellison" scenario is now a certainty.

I don't want to wait for this deal to close or read any more headlines.

12

1

55

One of the best to ever do it

RIP to the 🐐 and thanks for all the wit and wisdom

You will be missed.

0

2

55

Looks like Florida's top citrus grower pushed me over a new milestone🍊🥳

Thank you guys for taking the time to read my writings and supporting what I do in my spare time🧡

Regardless of what you see in the financial news, micro-cap value ain't going anywhere! At least, I'm not

3

0

54

I compiled a list of publicly available investing resources that I find insightful and enjoyable (link in bio)📚

Lmk if there is anything else I should include🙏

1

7

50

So many weak hands holding $PARA, I should do a blog update

8

0

53

What people think they need to read in order to improve as investors (left)

vs. what they actually need to read (right)

10

8

52

Next hedge fund idea:

a strategy based on exploiting manic-depressive episodes of fintwit accounts with too many cult-like followers

$SBSW

5

0

51

13.5% YTD

Not great, not terrible

Volatile.

disc: earlier this week, I built a position in $ALCO and my write-up will be published as soon as I speak with the management

3

0

49

Of course it is up 40% since

Unpopularity wins!

In case you were wondering how popular CRE is rn

In all of the US and Europe, there is only a single ETF that tracks that market segment

And, so far, this ETF has attracted less than $1M worth of assets🤣

1

0

10

6

2

50

A new article with updates on my highest-conviction ideas for 2024 has just hit your inbox

🇮🇹🇸🇬🇬🇧🇺🇸🇯🇵

9

6

50

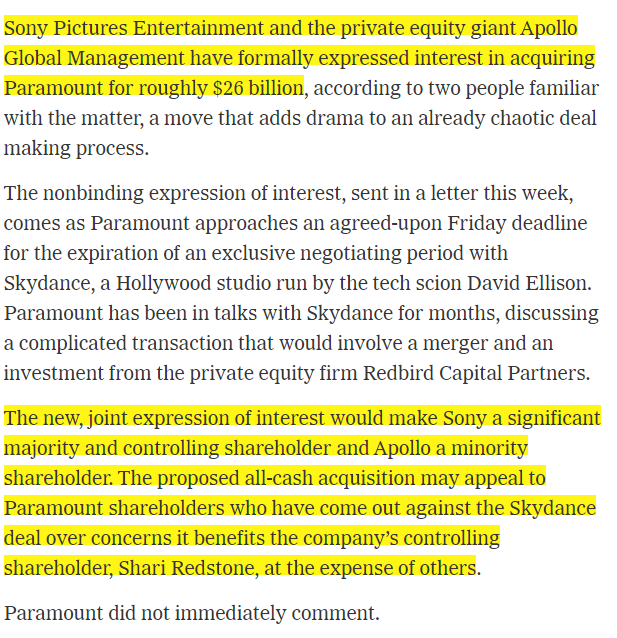

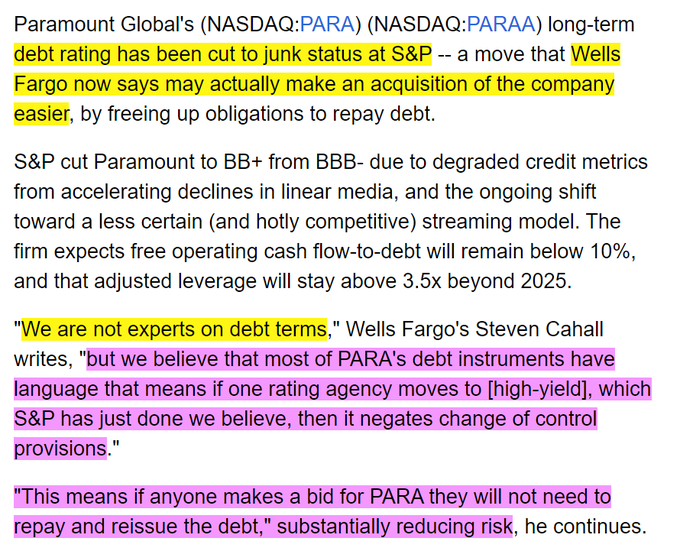

We think any party interested in all or pieces of PARA, including studios, IP, CBS and real estate, are more likely to emerge now that the debt CoC is void," Cahall said, noting that creates more sum-of-the-parts upside potential

$PARA

Things are moving fast. I like my junk

1

4

49

I wrote up Redbubble $ATG.AX

Once a Fintwit darling, is now down 93% from its highs and completely forgotten by the market

I believe it provides a good risk-reward here since it trades at a forward multiple of 3xEV/FCF

1

6

48

A new write-up has just hit your inboxes❗️

Cardonomics at 4-6x normalized earnings

5

4

47

@Tintincapital

"I like buying stocks that are down 90% because you can only lose 10%. That's psychics" ~Albert Einstein

6

0

48

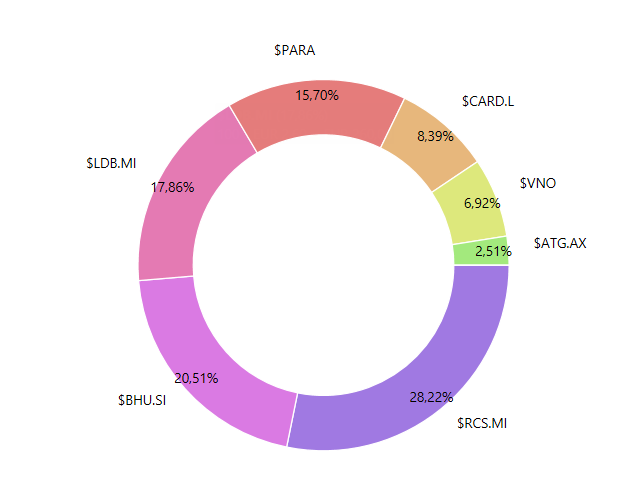

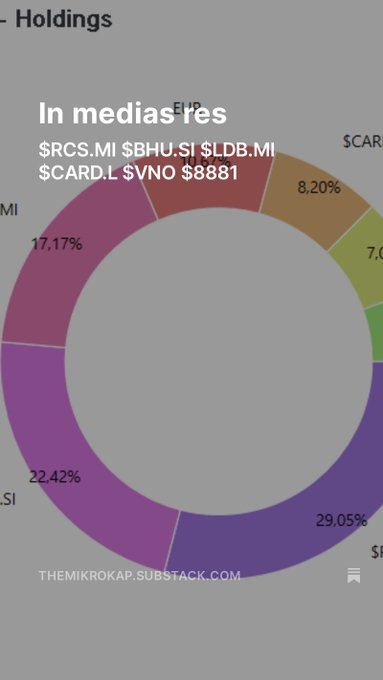

It's been a while, my sweet summer child

$LDB.MI $RCS.MI $BHU.SI $ALCO $PARA $VNO $ATG.AX $CARD.L $8881.T

Out at the usual place❗️

2

2

46

"Fish where the fish are"

3

6

46

Another HVAC-related acquisition coming from $LDB.MI ❗️

4x EV/EBITDA for ENERGY PRO SYSTEM SRL

4.8x 3-yr average EBITDA

This is how they structured it:

1/ initial cash payment of 120K

2/ 780K at the closing which is expected by the end of July split into:

-50K shares ~192K

4

4

45

On micro-cap fintwit we've quickly come from:

1. hey, check my YTD performance🥳

to

2. there's a big opportunity in non-US smalls❗️

to

3. all I feel is pain📉

I'll likely diversify into some GARP names that I'm following closely, when this G is free and when 4. happens

9

0

44

Sold half of my $VNO position for a 88% gain

I believe the RE market segment, especially CRE, has morphed into pure speculation on the movement of long-term treasury yields

Also, the fact that the same insider who has been buying shares this spring has now sold his holdings

10

2

46

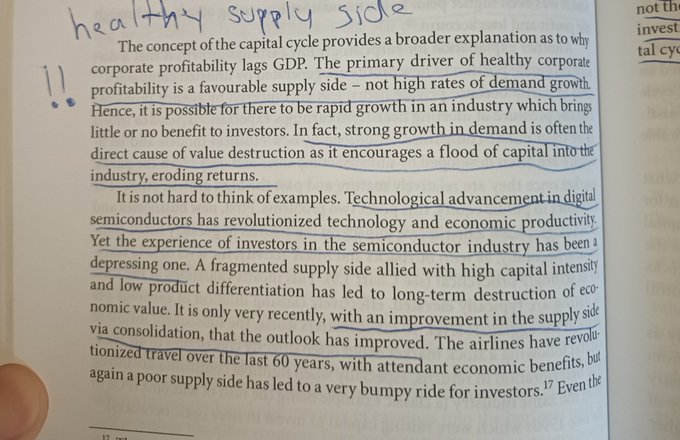

Focus on the supply trends, not the demand growth

Healthy supply side = healthy earnings power

Reasons why high asset growth underperforms

via Capital Returns

15

15

142

3

4

43

@CDInewsletter

Why? You're already at a ~80% payout ratio, revenue fell in the 10-yr period while the earnings grew at a 1% CAGR. Both not beating inflation over that period. Meanwhile, you have US treasuries yielding you close to, or above 5%, depending on the duration

I don't get the

5

0

46

These two points appear the most frequently in the notes:

1. Do good valuation work. Plug in estimates for earnings in a normal year. Look at things through EV/EBIT basis. Know what something is worth

2. Think simply and little bit differently. It is the context in which you...

Is there a better investing resource than the class notes from Greenblatt’s Special Situations Class at Columbia

No, I don't think there is

16

43

579

3

0

45

"Diligence is the mother of good luck"

Perfectly sound P/Es of 1 seem like a decent strategy, don't you think🙃?

2

3

45

I like the level of portfolio concentration where I *want* to read every filing for each of my positions

It feels good to be on top of things, even if it means reading useless 8-Ks

3

1

44

Do all passive investors have such high hopes?

I have over a million bucks in the stock market in $VOO and $QQQ.

That will average 12% annual returns

I’ll make $120k a year for doing nothing

Fibonacci that

222

51

1K

15

2

42

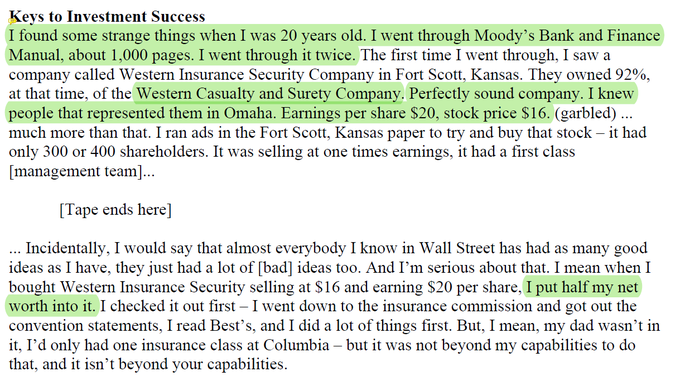

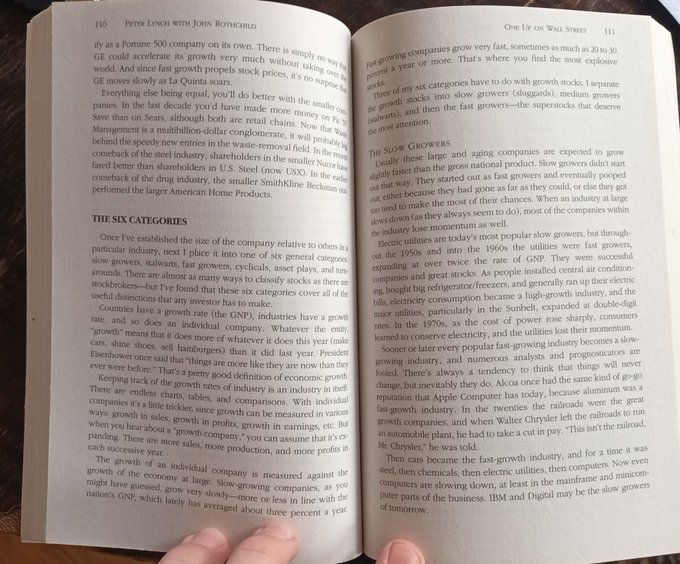

Vividly remember the first time I read this chapter. Felt like an unexplored gold mine, just waiting for my pickaxe.

It doesn't get better than One Up on Wall Street when you're first starting out

5

2

43

When you write up an obscure microcap and unintentionally turn it into a Fintwit favorite😔

5

0

42