Colarion

@colarion

Followers

4,187

Following

37

Media

517

Statuses

2,401

Investment advisor focused on the financial sector. Posts are not advice. Personal bank writings:

Joined November 2019

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Covid

• 886713 Tweets

Leyen

• 205047 Tweets

梅雨明け

• 190759 Tweets

Raila

• 99549 Tweets

黒人奴隷

• 98723 Tweets

#BRANDSbraincampxFourth

• 80524 Tweets

BRANDS AI TALK x FOURTH

• 76329 Tweets

パワプロ

• 41051 Tweets

Halal

• 39280 Tweets

カルストンライトオ

• 32933 Tweets

Yunan

• 26877 Tweets

Maitlis

• 21278 Tweets

#EnflasyonMuhasebesi

• 21007 Tweets

Haas

• 18219 Tweets

Colabo

• 15195 Tweets

DONNY X UNIQLO

• 13404 Tweets

#TheBoysFinale

• 13035 Tweets

エビデンス

• 12983 Tweets

BarengPRABOWO MakinOPTIMIS

• 12636 Tweets

SEMANGATbaru EKONOMItumbuh

• 12221 Tweets

#WeMakeSKZStay

• 11725 Tweets

暇空敗訴

• 11045 Tweets

Pinned Tweet

This account is not here to grow 100,000 followers, but to give & get constructive ideas and feedback.

Investing well with banks requires gathering datapoints and details from all corners.

Value nerds reading 10Qs and CRE rags are welcome here!

4

2

69

Good WSJ article this morning on what a joke the BNPL ecosystem is until it’s required to report to the credit bureaus.

17

19

196

I am thinking of starting a credit union specifically for bank investors.

We will acquire banks and pay nice dividends to members.

Like this tweet if interested in being a member.

I’m at least 50% serious.

18

2

186

A new way to post guidance:

Instead of saying 5-8% decline in your principal business, say “92-95%” and then “of 2023 levels” in fine print.

$SOFI is guiding for 50%+ revenue growth in the Tech Platform. This is huge!

26

50

447

6

10

94

Senator Warren penned a WSJ opinion this morning suggesting Capital One might charge merchants a 10% swipe fee.

This should not have been published.

14

3

64

For the 8 months since SIVB, a small and devoted crew of bank nerds has tried to educate the bearish masses about differences among CRE loans between investor cre, and cre attached to a business.

Finally the data is out and we can rest:

3

4

58

Why are small banks not failing?

I read on here that there would be lots of failures.

16

2

58

He’s one of the sharpest publicly-traded bank CEOs in the country and he’s probably spoken to 5 institutional investors in a 20+ year career.

Can you name him?

5

1

54

He always does this. He sells control of his banks when everything is fine and he shovels in with both hands when everyone is running for the hills.

It's why he owns the banks himself.

5

3

55

My Twitter feed:

"Kyiv is surrounded, WW3 close, global food shortages, plus fiat system upended."

My email:

"All the banks we spoke with at our conference expect rising margins and loan growth. Taking advantage of any weakness to repurchase. "

3

4

48

Everyone enjoy. Hingham fans will appreciate this one.

5

7

49

Blackstone $BX picking up free money off the ground at 12% sub 40% ltv. PE also typically finances a big chunk of these deals.

Why don’t banks do this? $OZK does and it scares the hell out of the market.

9

3

46

It’s recently become popular to mark bank loan and securities books to market.

Now try the holdings of private equity, BDCs and REITs.

The BDC ETF (BIZD) and PE ETF (PEX) are both around flat on the year but their assets are not interest rate agnostic.

6

7

46

What’s the most interesting business you’ve found embedded inside a financial company?

Extra credit if poorly understood but nicely profitable.

For example mineral management at $FFIN, special needs trusts at $OBT or servicing right loans at $MBIN.

18

4

44

Kudos to

@MaxfieldOnBanks

for hosting a fantastic bank “symposium” in Philadelphia the last 36 hours.

A unique chance to sit and listen to 5-6 of the country’s best bankers talk about the how and why of their cultures, among other highlights.

3

3

45

A lot of banks are including 2Q statements like "we feel confident for the remainder of 2022" and when you dig into the details the real story is closer to: loans are now over floors, NIM is going to blow out and barring a credit turn they will spew profits like a firehose.

4

6

45

52 banks are trading under 6x their most recent quarter earnings.

Those results don't have mortgage gains or reserve releases so are largely clean.

10

4

44

Don't forget that bank stocks are subordinate ownership of portfolios of levered, illiquid junk-grade notes.

In this context & today's market it's important to understand credit culture and underwriting standards.

Many banks are very cheap today but culture matters.

2

6

44

Bert Hodges from the 7-12 minute marks of the '22 $THVB annual meeting is probably boring his audience to tears but he is giving a synopsis of how to run a top 1% of 1% bank.

4

4

42

Bank investors should just accept that deposit costs are going to settle close to 3% at most spots.

Those where it doesn't are risking customer losses, or have special verticals / heavy non-interest bearing.

The real evil is the 5yr fixed CRE loan made in 21.

1

1

42

A lot of folks did not want to hear all the negative things

@Seawolfcap

had to say about $SOFI, but they are coming to find he was performing a public service.

I personally didn’t want to deal with all the aggravation of hundreds of random people being angry at me.

5

1

43

If there were a Guinness record for lowest dividend payout ratio, it might go to Northeast Bank $NBN paying $0.01 on $1.61.

They are saving their capital to pick off Synovus, Capital One and others selling office portfolios in part so those banks can go to investor conferences

0

2

40

Amazing email from Mozilo in August 2005 about how the game was up.

Market turns can take time.

The full email from Angelo Mozilo that was quoted in the government settlement with Bank of America. It's a good one:

http://t.co/GSDpdW77Qk

8

37

64

2

4

41

This lawyer Mike Bell is the OG of arranging credit union deals to buy banks.

He expects 2024 to be a record year for activity:

6

4

36

Western Alliance still has 33% non-interest bearing deposits.

Not bad after the shots they absorbed.

2

1

38

In honor of

@MaxfieldOnBanks

while he’s with family, let’s touch on a favorite topic of his - low ego bankers.

After some recent run ins with nasty levels of ego I am reminded the value of long-term partnerships with bankers who think like partners…

3

0

37

People call $NYCB a panic but it's a conservative reset to new $0.60 - $0.80 range estimates and slender credit disclosure.

Also the OCC "regulator" who drove this might check in with colleagues regulating $USB on how to best manage capital transitions.

4

7

37

A reminder today from Green Street about CLO market. CLO funded commercial mortgage reits that lent billions on bridge include $RC, $ABR

5

10

36

The concern over bank bond marks is ironically improving bank bond marks.

1

6

37

People wonder if COF / DFS will be approved.

There are 80+ credit card issuers in the US and no barriers to entry.

There are 4 networks in the US, one of them runt sized. Maybe never another.

It should not be a question.

10

1

35

The Truxton $TRUX parking lot is empty for the holiday, but interest and fee income did not take the day off.

3

2

35

PNC CEO Bill Demchak came to speak to the local Rotary today.

He was on point on most topics, from the bureaucracy of Teams meetings to why branches still have value.

And he clearly wants to scale up several hundred billion in assets. He doesn’t think regulators would block

7

6

34

Alabama Credit Union is probably killing it on net promoter score:

2

1

35

People look at Wells Fargo and think “WFC yields 3.30%”, but they are missing the steady stream of class action settlement payouts they can take advantage of if they have full time administrative help.

3

2

34

While private equity will have interest, several superregionals would likely want to take $SIVB at a distressed price and without the regulatory politics typical of mergers.

Waiting out their underwater mortgage backed portfolio is not a complicated thesis.

2

2

34

Apparently the $915mln $OZK loan is $555mln funded due to TI holdbacks per Sandler, with about $900mln cash invested subordinate.

That’s a fair amount of cash.

3

1

34

There may be no US company, I certainly believe no US bank, with a larger disconnect between current multiple and takeout multiple than BayFirst $BAFN.

57% of tangible book with 12 locations across Tampa, St Pete and Sarasota.

Marine $MBOf just sold for 150% or 2x including

5

3

35

Market: We like insurance companies.

Insurance companies: we buy unsecured paper from Camden Property Trust, an apartment REIT, at 112 over SOFR

3

3

31

Thomasville $THVB releases a few sentences for 1Q saying:

- Made 25% ROE

- Grew loans

- Grew dividend, which is meant for local shareholders.

I will have to arrive to the annual meeting in turkey hunting attire to disguise myself as a local.

7

1

32

The analyst died so UMB could buy Heartland.

Not so some cable company with 30 subs and a 2 page cap stack could make an international acquisition, but two vanilla midwestern banks.

What a terrible culture.

Bank of America IB Analysts and Associates are organizing a strike for tomorrow

140

997

12K

3

4

32

$NYCB analyst: “What do you think about FDIC acquisitions?”

NYCB CEO: we would like to avoid becoming one.

2

3

31

Credit union update:

A credit union attorney says that in order to create a non-taxed financial engineering and acquisition engine, one must get a nonprofit to donate $5-$6 mln to capitalize the entity.

My focus shifts to a possible CU rescue

3

0

31

$SOFI carries reserves of 0.53% against a hyper growth $9bn loan book of internet-originated consumer loans yielding 11.26%.

Perhaps they share the same regulator as $SIVB.

1

3

30

Good public service announcement from

@TimyanBankAlert

around banks that are not earning cost of capital…

4

5

31

5 Points May: Colarion’s take on bond market shrapnel hitting banks & preserving capital

1

6

31

Bank CEOs with 8x forward multiple shares looking at $SOFI's 2x tangible, NM P/E with 200% loans / deposits both sides of the book wholesale, and getting analysts to buy into adjusted EBITDA as their primary metric:

4

0

31

So, what other banks would now like to cross the $100bn threshold?

3

0

31

I appreciate that only 18 people have seen this masterclass. Thanks to Travillian. I won't publicize this situation any more than I already have, as a favor to Steve.

5

1

31

Warburg Pincus priced their $400mln $BANC infusion at $12.30, a bit less than 7x earnings power. Now available to everyone else after a bit of waiting…

3

1

31

On Schwab, it takes an advisor 19 clicks to allocate a trade.

Between the interface, the clunky trading vs IB, the interest rates, and the balance sheet gambling, I sometimes wonder why they are still popular.

6

0

31

Several higher quality banks are 7-8x 2023.

If rates rise less than expected, margins will lag but credit should do well.

If rates rise to 3%, CRE / construction will suffer but core deposit banks will feast.

Valuations are not challenging.

3

1

29

(1/3) Moving on from the 18 $SIVB analyses in my TL from twitter popup gurus, two improvements we need moving forward:

1) Increasing FDIC insurance by 50-100% per account reduces risk for both banks and FDIC by disincentivizing overnight wires out.

2

1

29

Paper-hands selling hundreds of millions worth of Affirm $AFRM.

A few casuals, including (checks notes), the company's CFO and Singapore's sovereign wealth fund, are missing the growth picture in this popular stock.

How did Singapore get involved here anyway?

3

1

28

Arbor $ABR is a REIT with aggressive standards for multifamily lending. NPA “ticked higher” in 2q from $8mln to $122mln.

4

1

27

This month - FCNCA, MCB, PACW, fragile CRE and proactive bank management...

1

2

28

It was a close call but

@Aureliusltd28

wins the “bank twitter poster of the last 3 months or so” award over a strong field including:

-

@OurBank3

- 🍩 posting

@thebankzhar

and

- cynical credit watcher

@CorpusCol

Points given for prolific datapoint sharing.

Congratulations to

6

3

28

Too bad you can't short credit unions.

They are the ones taking fixed rate auto loan share from Ally.

The ones signing up long-term for Jack Henry.

The ones overpaying for mergers.

9

2

27

The reason $BANC is motivated to close $PACW is not because they believe in fairies / are oblivious of loan marks.

It’s because of the value creation from

removing certain toxic executives who had a Yellen-level talent for capital misallocation combined with the petty greed of a

5

3

27

Would anyone like to share anything about where Jim Simons donated money?

No they just want to talk about his returns.

Colarion is here to fill the void - he granted billions to awesome technical projects to make the world better in a scalable way…

1

1

27

I’m looking for people who haven’t done any work to forward me graphs and articles about commercial real estate.

Ideally take a single chart from someone who has done work, and ignore that work and just use the chart.

Thanks in advance

1

1

26

Banks casually trading back to lowest levels in 14 months as generalists remember that the sector can be hard to analyze when rates move, and favorites $FRC and $SIVB have retraced 53% and 77% from highs, respectively.

3

2

27

Capitol Federal (CFFN) and Hingham (HIFS) have similar low cost models with long-term fixed rate assets and now severely crimped margins.

Market is burying Capitol for it while Hingham enjoys benefit of the doubt.

2

3

27

FICOs will become less meaningful by the day until this is addressed.

The card issuers likely are trying some fixes but I’m not sure how they can optimize without a look into checking accounts.

6

0

27

Apparently the Signature rent stabilized book is going for a 30% haircut despite funding help.

So the market pivots to $NYCB and studies this slide.

3

1

26

I find it interesting that Northeast Bank $NBN buys diverse CRE loans in secondary market at 8-9% but all other banks through the cycle originate at 2/3 that interest rate because of ReLaTioNsHiPs.

4

2

26

Latest 5 Points is out (open version). A look at First Citizens, Third Federal, loan growth, Green Dot, and the recent tendency for banks to bottom intra-quarter:

3

1

26

Quasi insider trading going well among bank officers...I could not screenshot further but this is about half the community bank insider buying tally for today thus far.

4

5

26

@MaxfieldOnBanks

make a poster at your next conference: “If your CFO is writing puts days before a 60% drawdown, move that person into marketing where they can do less damage.” and attribute quote to some old banker dude.

2

0

26

Truxton Trust $TRUX is the only bank I know that reports non-interest income above net interest income.

It seems inconsequential but it tells you everything.

3

3

26

Two interesting anecdotes -

He races motorcycles, and he trades crypto in his PA despite considering it worthless.

4

0

25

Twitter is ideal for “drive-by analysis.”

CRE is a problem in this rate environment but should be broken down by recourse, category (office vs apt vs small strip, own occ etc).

I’ll probably write this up in 5pts because it’s a primary 2024 topic and blanket shorting won’t work

Commercial Real Estate is a BIG ongoing problem for the non-SIB banks...

50% of people haven't gone back to office...and as leases come up for renewal they will just not be renewed, leaving a long-tail of non-performing loans on the books of the regional banks.

There are

193

435

2K

5

2

26

It’s tempting to think of a credit cycle like a mamba that comes out and kills you quickly.

But constrictor may be a better analogy.

2008 seemed fast but it took from feb 2008 to around 2012.

Or 2022 at Signature Bank of Georgia which took a patient approach.

7

1

25

Legacy bank core processors showing off their latest innovations…$FIS $FISV $JKHY

2

1

26

Look at Santa's basket of toys the children threw away.

What do we see for 2023 among these worst performing banks? Several still look like shorts but 4-5 are reasonably managed and are suffering from January effect. I know where

@thebankzhar

is leaning!

8

4

26

Excellent thread

Frens, I would like to tell you a tale that might teach us all a lesson or two about what’s coming. As many of you know 70s were characterized by deeply negative real interest rates as well as rampant inflation rates. Borrowing boomed, both public and private.

1/N

156

958

4K

0

1

26

Interesting story about goings on at Western Alliance during the panic.

It's a wild world out there and the premarket and options market can fuel a fire.

To their credit Western Alliance was ready to communicate their story.

1

1

25

If you ever see a research report valuing a bank on sales...I'm trying to be diplomatic here, but that analyst may be writing for the company as an audience rather than the bank investing community...

3

3

25

People are interested in bank failures. Here is one.

Conn’s isn’t really a retailer, mgmt just uses furniture as collateral to make consumer loans, like a bank.

People have bought less furniture post covid and higher rates and tighter terms hurt.

Watch the shadow banks.

2

2

30

All the small bank sellside notes I get describe business development opportunities.

All the regional bank sellside notes describe what the banks are doing for regulators.

If I were a regional bank I might allocate capital away from spread, yet banks like M&T and Truist are

1

3

25

I like $CFST sitting on OTC out of the Russell, no street coverage, only sector nerds 🤓 understanding the value proposition.

A typical Colarion situation (don't take this as advice).

3

2

25

Live Oak Bank $LOB

"We are replacing core processing"

boring

"We are replacing core processing and will be building a customized quickbooks inside your bank account"

Not boring.

The golden age of bank innovation is coming.

2

3

23

We just published a 5 points at

Covers Puerto Rican banks, $FFBB, fintech waste, and asset quality trends among others

1

2

24

I don't believe it's legal to speculate / encourage bank runs, but will say, with no position in $SI either way, that the bank and regulators had thought about this in advance.

$SI loans / deposits ratio is 4%, which may be the lowest of any bank in America.

4

2

24

Regional bank index coming back near its highs.

However, to quote a colleague in depository investment banking, for me-too vanilla banks, "2022 is going to suck." (mortgage, no PPP, spread compression etc)

Have to think differently to prosper.

3

3

24

Does a community bank want to sell? Use this proxy season to learn the secrets.

3

6

24

Oriental $OFG used to be one of the lowest quality banks in America, they printed a 99bp margin a few decades back when they were just a bond carry trade.

Today they are walking around like Frost Bank in its heyday.

Viva the Puerto Rican oligopoly!

4

1

24

The S&P ticker search algorithm nails it every time. This is life when you buy a software company and then just milk it for cash.

2

1

24

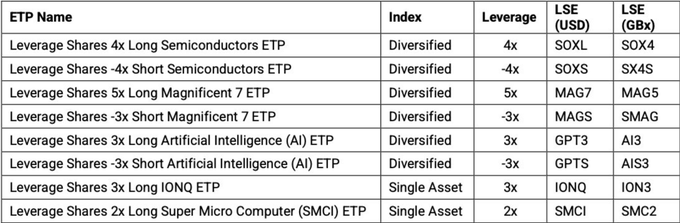

Waiting patiently for a 3x levered sustainable 15% ROE OTC bank etf.

They launched a bunch of seriously leveraged ETPs today in Europe incl 5x Magnificent 7, 4x Semiconductors, 3x Artificial Intelligence and 2x Super Micro Computer

97

103

740

2

1

22

So $NYCB has $18bn of loans at the mercy of a board that capriciously sets rents.

2 on the board are landlords

2 are tenants.

5 are appointed by the mayor.

Hey Mayor Adams, you can skip your next fundraiser, the new $NYCB ownership has some ideas to take care of you.

1

4

23

Why own boring banks? A holiday gift of moneyball math.

1

1

22

5 Points August, by

@colarion

A bit about JPM, SOFI, PNFP, BKU, tangible book values, and the bank catalyst ladder, among other topics

4

5

22

A lesson from 99 is once the story stocks are busted, most never return.

This is because they are dependent on capital markets to fund ongoing growth, and capital markets don't reward favors post a 50% drawdown.

4

1

23

We chuckle at Link Bancorp $LNKB, whose predicament was foreseeable from the day the mgmt comp plan was unveiled, but they will get credit for listing on nasdaq and now qualifying for Russell pro forma.

Increasingly, getting blind etfs to buy your stock is the game.

2

0

23

Everyone: Urban office requires 15% reserve if you underwrote well.

Eagle Bank: We are closer to 3% and will get there in time.

4

0

23

There are a few banks that benefit from higher rates and which should be trading to the moon like homebuilders.

Conversely there are some banks being lowered into the coffin by FOMC policy.

But they move in tandem.

4

0

22

If you have $1 of equity and you add 12% to it each year for a decade, you have $3.10 of equity.

This is all we really need to do and its why conservative, efficient operations appeal more than story stocks, rollups and ego-heavy management.

1

1

23

Bank Investors of the World Unite! Creating a “union” to drive outperformance

3

3

23