Stocks & Stones | Mathieu Martin

@Stocks_Stones

Followers

7K

Following

8K

Statuses

6K

MicroCap Expert | I help you invest in small public companies 💵Portfolio Manager @ Rivemont MicroCap Fund 🖊️Newsletter Writer (Subscribe for free | Link 👇)

Montréal, Québec

Joined January 2014

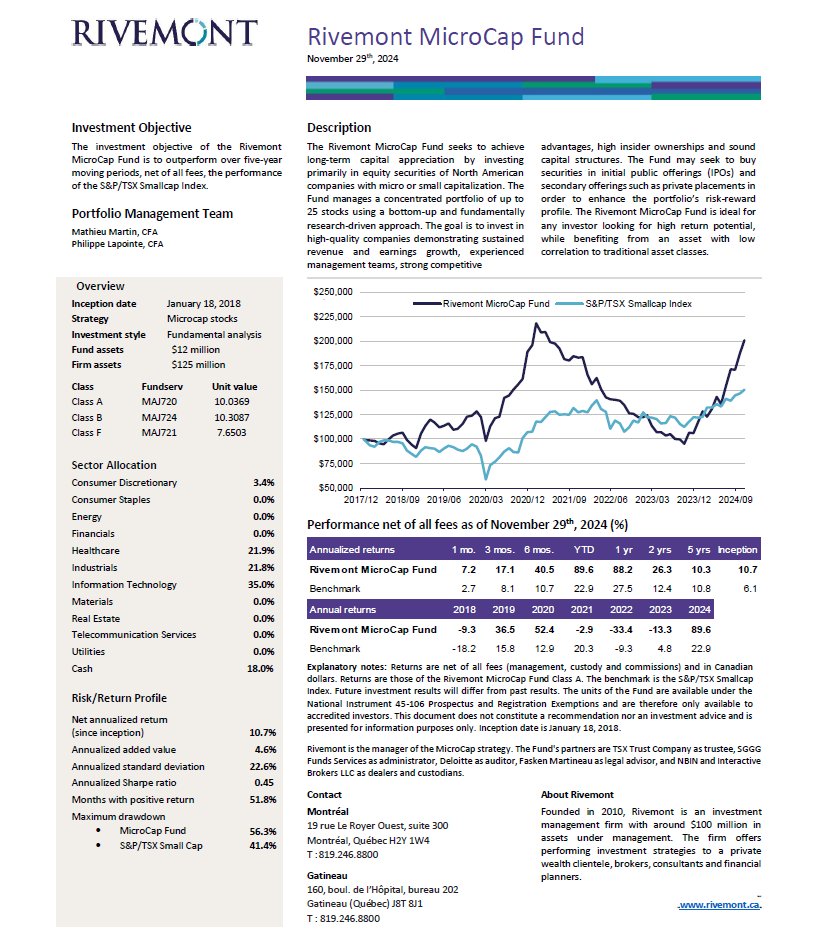

I'm pleased to share that fundamental research still works! The Rivemont MicroCap Fund (Series A) I manage gained 7.2% in November, reaching + 89.6% year-to-date! In 2024, the fund held between 15 and 20 names and had: ✅ One stock up over 300% ➡️ $PNG.V ✅ Two stocks up over 200% ➡️ $COV.V & $BRM.V ✅ Three stocks up over 150% ➡️ $HASH.V, $CNO.V & $RW.V The largest loser was a detractor to the fund's performance by less than 1%. What a fantastic year it's been 🤯 And you know what the best part is? Trading and financing volumes on the TSX Venture are still 25% below historical averages. We haven't even crept up to an average level of liquidity and access to capital yet. Plenty of quality growth stocks still trade between 10 and 15 times cash flows (compared to 5-8x at the beginning of the year). Am I the only one who feels this bull market is only getting started?

15

19

183

SAVE THE DATE! Our next Rivemont MicroCap cocktail will take place on March 26 in Montreal. 🥂 We have a fantastic schedule for this Value Investing special: ➡️ Keynote speech by @BenjContra (Benj Gallander - Contra the Heard) ➡️ Supremex $SXP.TO ➡️ DATA Communications Management $DCM.TO Registration is now open on Eventbrite! 👇

0

0

0

Five Key Questions ❓❔❓❔❓ I’m a big believer in simplicity. Investing is complex, but a microcap idea usually boils down to a handful of key drivers, catalysts, and risks. You can improve your research process tremendously by focusing on what matters. Here are five crucial questions you should ask yourself when looking at a new investment idea: 1⃣ Is This a Company I Can Understand? It’s fair to assume that the market is generally efficient in large caps. So many professionals and experts are looking at these companies, and the vast majority of the relevant information is already priced in. If the market tells you a company is worth $50 billion, you can, at the very least, assume it’s legit with an actual product and real customers. On the other hand, very few professionals look at microcaps. Companies can pay (egregiously) for marketing and promotion to inflate their stock price. Excellent businesses can go unnoticed for years. The market is highly inefficient the smaller you go. You must do the research yourself because nobody will spoon-feed it to you. If you can’t understand the business or the industry, it’s a very challenging start. Of course, you can’t know everything. You must keep an open mind and look at stuff you know nothing about. Hopefully, you can learn and develop a better understanding in some cases. That said, if I spend a few hours on a new file and feel like I don’t understand it any better, that usually goes in the ‘‘Too Hard Pile’’ for me. That’s it – I’m done. And I don’t care if the stock rips 100% in my face the following month as long as I passed for the right reason. 2⃣ Is This a Company With Competitive Advantages? The laws of economics make running a business a very competitive endeavour. To generate better-than-average returns over the long term, you need to own companies that compound their fundamental value at a higher-than-average rate. To make that possible, companies need a ‘‘moat’’ that insulates them from the competition. Don’t get me wrong, you won’t find terribly strong moats in microcaps. No microcap that I know of benefits from network effects like a Meta or has the scale advantage of a Costco. What you should look for is an emerging moat. Is the company dominating a small niche? Is the niche growing? Can they expand to adjacent areas over time? You’ll save yourself a lot of trouble by avoiding completely commoditized industries or companies with no pricing power. 3⃣ Can I Trust The Management Team? On average, I think the governance at most microcaps is very subpar. Boards are either incompetent, don’t care, or fail to hold management accountable when results disappoint. While I certainly like a strong board and pay a lot of attention to governance, I’m not looking to play an activist role and kick CEOs out of their companies. If I find a company where the CEO has a solid track record, has shown he can deliver results, is non-promotional and focused on the long term, my odds of a successful outcome skyrocket. Study management’s track record. Watch webinars and interviews they’ve conducted. Pay attention to what they discuss (long-term vs. short-term goals) and how they discuss it (promotional or not). Schedule a call with them. Ask them the tough questions. My most significant positions tend to be in the companies where I trust the management team the most. 4⃣ Does The Market Misunderstand The Opportunity? So you’ve found a company you can understand. It has a moat. The management team is fantastic. It’s probably not trading at a cheap price, right? For something to be cheap, it must have some hair on it. Something must look wrong to the market. Maybe the company had some hiccups in their last quarterly report. Maybe the outlook for their industry has deteriorated. Maybe insiders are selling. Whatever it is, you must be able to identify what is the consensus and why the consensus is wrong. What do people misunderstand? How much research have you done to build your case and be confident in your assessment of the situation? If you can’t explain why something is mispriced and how the market’s perception will change over time, you don’t have a strong enough thesis yet. 5⃣ Can I Buy It Substantially Below Intrinsic Value? Now, we’re talking about valuation. So far, it’s been all about the qualitative (management, moat, story). The last question is about the quantitative. You need to examine the numbers and the business trajectory closely and make assumptions about the future. How much is this business worth? Can you buy it at a discount? Dozens of books have been written on the topic of valuation. To become a successful investor, you must understand accounting and valuation. It’s too complex of a topic for me to elaborate on here, but I highly encourage you to educate yourself if needed. I’m an outsider to the finance industry, a self-taught investor who learned to invest successfully ten years ago without going to college. You can learn it too. ''Few things are as costly as paying for potential that turns out to have been overrated.'' - Howard Marks, Mastering the Market Cycle You can do the best qualitative research in the world, but overpaying for something will hurt your returns. Valuation matters. Don’t skip this crucial step. Use these five questions to guide you and spend your time where it has the greatest impact. Most importantly, I think these questions will highlight some of the weak spots in your analysis and likely prevent you from making costly mistakes. At least, that’s my hope! Investing profitably in microcaps requires significant effort and time. It’s absolutely possible to succeed if you commit to it. However, if you’re too busy, there is another option. You can opt for a professionally managed microcap strategy. I'm the portfolio manager of the Rivemont MicroCap Fund. To learn more, please visit: You can use the same link to subscribe to my free newsletter and ensure you don't miss the following posts. Thank you for reading! 🙏

1

2

17

TSX VENTURE FINANCING STATISTICS: **January 2025 vs 2024 (YoY)** Issuers Listed -79 Number of Financings -14% Total Financings Raised (in $) +52% **January 2025 vs December 2024 (MoM)** Issuers Listed -7 Number of Financings -11% Total Financings Raised (in $) +9% The total financings raised ($) on the TSX-V continue to improve sequentially and year over year. Fewer financings were done, but the amount raised was higher, meaning larger deals are being completed. I've seen way more financings get oversubscribed lately, which we had not seen at all over the last two to three years. Onward and upward! Link to the data:

0

1

2

The replay of the Covalon Technologies $COV.V presentation at our last Rivemont MicroCap cocktail is now on YouTube! We highlighted Covalon as one of our 2025 top picks in the Rivemont MicroCap Fund.

0

5

24

TSX-V Trading Statistics **January 2025 vs 2024 (YoY)** Volume +18% Value traded ($) +37% **January 2025 vs December 2024 (MoM)** Volume +4% Value Traded ($) +18% The TMX Group posted robust trading data on the TSX Venture exchange for a fourth consecutive month. The bullish trend is intact! Link to the data:

0

3

8

RT @evfcfaddict: Finding cheap stocks in small- and microcaps isn’t really difficult. The harder and way more important part lies in find…

0

6

0

@PaulAndreola $LOVE.V is right around $100m market cap, growing and profitable. It trades at a discount to the value of its real estate. It's gaining market share and can triple its revenues within its existing facilities. The stock is starting to get discovered, but it's still early days!

0

1

18

The replay of illumin Holdings' presentation at our last Rivemont MicroCap cocktail is now on YouTube! We highlighted $ILLM.TO as one of our 2025 top picks in the Rivemont MicroCap Fund. The stock just hit a new 52w high today. Great time to look at it!

1

0

8

@ffournier5 I was very close to including it! They're making long-term investments that are hurting short-term profitability. However, even though the market reaction to the financial results was brutal, I don't think there's anything wrong with the business.

1

0

0

I came back from vacation yesterday and found this in my inbox. I'm super flattered by the kind words from Rick Peterson at @PetersonCapital in his excellent newsletter to wealth advisors and portfolio managers. Thanks for the shoutout! Check out the link in my bio to subscribe to my free newsletter.

4

3

35

RT @evfcfaddict: We are back! @iancassel (founder MicroCapClub) and me talking to @SebKrog (investor, writer) @Stocks_Stones (fund manage…

0

19

0

I recently did two interviews, and both times, I was asked for my favourite book recommendations. During the last couple of years, I became very interested in moats, or competitive advantages, so I answered with three books I enjoyed on this topic. Instead of doing book reviews, I thought I’d highlight a few of my favourite quotes to give you a flavour of each book and maybe entice you to pick one! 📙 The Little Book That Builds Wealth - Pat Dorsey 1) It’s easy to get caught up in fat profit margins and fast growth, but the duration of those fat profits is what really matters. Moats give us a framework for separating the here-today-and-gone-tomorrow stocks from the companies with real sticking power. 2) Although there are times when smart strategies can create a competitive advantage in a tough industry (think Dell or Southwest Airlines), the cold, hard fact is that some businesses are structurally just better positioned than others. 3) In my experience, the most common “mistaken moats” are great products, strong market share, great execution, and great management. These four traps can lure you into thinking that a company has a moat when the odds are good that it actually doesn’t. 4) The four sources of structural competitive advantage are intangible assets, customer switching costs, the network effect, and cost advantages. If you can find a company with solid returns on capital and one of these characteristics, you’ve likely found a company with a moat. 5) A brand creates an economic moat only if it increases the consumer’s willingness to pay or increases customer captivity. After all, brands cost money to build and sustain, and if that investment doesn’t generate a return via some pricing power or repeat business, then it’s not creating a competitive advantage. 6) The only time patents constitute a truly sustainable competitive advantage is when the firm has a demonstrated track record of innovation that you’re confident can continue, as well as a wide variety of patented products. 7) Companies whose futures hinge on a single patented product often promise future returns that sound too good to be true—and oftentimes, that’s exactly what they are. 8) You’ll notice I haven’t mentioned many consumer-oriented firms, such as retailers, restaurants, packaged-goods companies, and the like. That’s because low switching costs are the main weakness of these kinds of companies. You can walk from one clothing store to another, or choose a different brand of toothpaste at the grocery store, with almost no effort whatsoever. That makes it very hard for retailers and restaurants to create moats around their businesses. 9) Switching costs come in many flavors—tight integration with a customer’s business, monetary costs, and retraining costs, to name just a few. 10) Cost advantages can stem from four sources: cheaper processes, better locations, unique assets, and greater scale. 11) A final type of scale advantage is domination of a niche market. Even if a company is not big in an absolute sense, being relatively larger than the competition in a specific market segment can confer huge advantages. In fact, companies can build near-monopolies in markets that are only large enough to support one company profitably, because it makes no economic sense for a new entrant to spend the capital necessary to enter the market. 12) Companies that provide services to businesses are in many ways the polar opposite of the restaurants and retailers. This sector has one of the highest percentages of wide-moat companies in Morningstar’s coverage universe, and that’s largely because these firms are often able to integrate themselves so tightly into their clients’ business processes that they create very high switching costs, giving them pricing power and excellent returns on capital. 13) Bet on the horse, not the jockey. Management matters, but far less than moats. 📘 7 Powers: The Foundations of Business Strategy - Hamilton Helmer 1) Scale Economies: A business in which per unit cost declines as production volume increases. 2) Network Economies occur when the value of a product to a customer is increased by the use of the product by others. 3) Counter-Positioning: A newcomer adopts a new, superior business model which the incumbent does not mimic due to anticipated damage to their existing business. 4) Switching Costs arise when a consumer values compatibility across multiple purchases from a specific firm over time. These can include repeat purchases of the same product or purchases of complementary goods. 5) Branding is an asset that communicates information and evokes positive emotions in the customer, leading to an increased willingness to pay for the product. 6) Cornered Resource: Preferential access at attractive terms to a coveted asset that can independently enhance value. 7) Process Power: Embedded company organization and activity sets which enable lower costs and/or superior product, and which can be matched only by an extended commitment. 8) Power comes on the heels of invention, be it in products, processes, brands or business models. However, most invention is merely a manifestation of operational excellence and thus not immune to the arbitraging actions of competition. 9) Good managers can rarely reverse the course of a bad business, i.e. one without Power. Over and over, I have witnessed Buffett’s axiom play out in the press, with business leaders castigated for poor management ability in the face of seemingly impossible circumstances. Yahoo, Twitter and Zynga come to mind here. That said, when it comes to establishing Power in the first place, make no mistake: leadership is fundamental. 📗 Quality Investing: Owning The Best Companies For The Long Term - Lawrence Cunningham, Torkell Eide & Patrick Hargreaves 1) In our view, three characteristics indicate quality. These are strong, predictable cash generation; sustainably high returns on capital; and attractive growth opportunities. Each of these financial traits is attractive in its own right, but combined, they are particularly powerful, enabling a virtuous circle of cash generation, which can be reinvested at high rates of return, begetting more cash, which can be reinvested again. 2) One way of assessing the durability of a competitive advantage is to invert the analysis. Instead of looking at what supports a competitive advantage, we analyze what it would take for a newcomer to replicate the business and remove the advantage. Such analysis often reveals idiosyncrasies that can be instructive in assessing a business's quality. 3) Sustained high gross profit margins relative to industry peers tends to indicate durable competitive advantage. Zeroing in on gross margins, as opposed to bottom line net income, also helps distinguish competitive advantage from managerial ability: bloated but short-term cost structures can reduce net income and disguise real long-term competitive advantages. High gross margins also confer other advantages: they can expand the scope for operating leverage, provide a buffer against rising raw material prices and provide the flexibility to drive growth through R&D or advertising and promotion. 4) When the argument for holding a position starts with a "yes, but", it often means both that a mistake has been identified and that someone is unwilling to admit that. If a company has highlighted a problem, the market knows about it; and its price-earnings multiple will have accordingly contracted (‘’the stock is cheap now’’). Many investment mistakes of retention follow such special pleading: if a position is maintained as a result of "yes, buts" it is probably a mistake. 5) For many fallen angels, overall deterioration generally begins with small things not going according to plan: growth not materializing, unexplained pressure on margins, more discussion of competitive pressures, or gradual increases in capital expenditure. Each disappointment is small in isolation; management provides a good explanation for each and dismisses them as non-recurring. But a string of setbacks often signals a larger set of problems, which emerge or crystallize after it is too late for the business to make corrections or for the investor to mitigate losses. Thus even small setbacks warrant rigorous evaluation. 6) A business that is solely linked to customers' capital expenditure makes for a much more complicated investment than one linked to their operating costs. In most cyclical industries, capital equipment is purchased amid periods of capacity expansion. On the other hand, for a company whose profits tie to customers' operating costs, cyclicality poses less risk of disruption and remains relatively predictable. That’s all I have for you today! I’m leaving for Mexico on vacation tomorrow. It will be good to disconnect for a week. I hope to be able to do some reading and thinking, which will be no easy feat with two young kids! My Good, Bad, and Ugly - January edition should be out upon my return late next week. Make sure you don't miss it by subscribing to my free newsletter (link in bio)! See you on the other side ✌️

0

2

14

RT @BenonJacob: I might be biased, but this is perfect weekend reading for all valuehunters out there! Mathieu was not only incredibly shar…

0

2

0