SouthernValue

@SouthernValue95

Followers

10,726

Following

1,537

Media

651

Statuses

5,094

Infinitely curious. DMs open. “Spend each day trying to be a little wiser than you were when you woke up.” - Charlie Munger

Boston, MA

Joined June 2019

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Vance

• 1061157 Tweets

#เทควันโด

• 494787 Tweets

Iraq

• 423725 Tweets

Alberto

• 389387 Tweets

Stolen Valor

• 252685 Tweets

Kursk

• 202430 Tweets

BEST WISHES FOR SAROCHA

• 199166 Tweets

Wisconsin

• 195037 Tweets

#เทนนิสพาณิภัค

• 182399 Tweets

Trump 2024

• 159918 Tweets

GIVE VINESH SILVER

• 133328 Tweets

Tampon Tim

• 123556 Tweets

Ripple

• 119348 Tweets

ISIS

• 117357 Tweets

#erişimengelinikaldır

• 89447 Tweets

Eau Claire

• 80201 Tweets

Walthamstow

• 52979 Tweets

Brighton

• 37473 Tweets

Leverkusen

• 37211 Tweets

Vienna

• 37039 Tweets

Quincy Hall

• 33652 Tweets

Home Affairs

• 31406 Tweets

Nelly

• 31249 Tweets

Chidimma

• 27125 Tweets

Stona

• 18820 Tweets

Bon Iver

• 18178 Tweets

#الاتحاد_انتر_ميلان

• 17262 Tweets

Chamath’s “cheap insurance” 5yr short bets have lost -77% and -106% as we approach year 4.

The growing short case on $FB and $GOOG:

1. New product experiences

2. Regulation

3. Taxes

4. Anti-trust

If you have the capital/stomach for a 5yr+ bet, here’s how I’d build the short case...

196

455

3K

43

86

2K

$GOOG clearly admitted last night that they are not seeing adequate *current* ROIC on AI capex, are likely over-investing, and struggled to provide concrete examples of killer apps deployed at scale, but emphasized that adoption of new technologies takes time, and the risks from

28

85

977

“ROIC is one of the most important principles in investing, which is so utterly misunderstood, most people don’t even know how to calculate it: NOPAT / WACC,” -

@chamath

😂

38

35

522

Stanley Druckenmiller:

“I was up 42% last year and I’m up 17% this year. I’ve made those numbers bc of the Fed not in spite of them. I have 6 outside money managers who are up a lot more than me. A monkey can make money in this market.”

13

40

450

Perhaps the whole scooter thing will become a relic of this VC bubble.

Tampa decides to phase out scooters over the next 3yrs.

The timing of $BRDS SPAC and the speed at which it incinerated shareholder wealth is just incredible

21

26

364

Why do some people feel so compelled to be opinionated on things they have literally no clue abt?

22

9

364

Below is a long thread on 7 key levers that will drive growth at $ADSK for the next decade. Investors have been fixated on mgmt.’s guided $2.4bn FCF by Jan ‘22, but I believe there is vast opportunity beyond that point. First, a summary of the drivers. I will expand on each one:

10

44

331

In my immaturity as an investor I mistook my contrarian bias for being an independent thinker. Today I strive to actually be an independent thinker, even when it leads me to conclusions that are quite consensus.

8

29

257

Note & analysis from Bernstein showing that the number of titles in a streaming library don't meaningfully drive engagement - new releases do. Candidly, I overestimated the value of libraries to legacy media companies in building sustainable DTC businesses $DIS $WBD $NFLX $PARA

17

27

254

What are the best annual letters or stock pitches you’ve read / heard lately? Kindly link below.

13

16

226

Good note from Kash/Goldman software team on what's weighing on the sector and their view from here:

- $15B of AI revenue at hyperscale clouds (~2% of global software revs) bypassing normal budget scrutiny. In a no-growth budget environment, that elevates the scrutiny on

@JaredSleeper

S&P 500 margins have been in contraction for 2yrs, wage pressures persist, rates are in restrictive territory, driving widespread belt tightening. Last year cloud optimization was the low hanging fruit and I think now as companies go into software renewals post layoffs, SaaS

0

1

18

1

18

223

Last time KC won the Super Bowl the S&P500 fell 30% in the ensuing 2 months

12

20

216

So you cant buy big tech (no earnings clarity), semis (cycle/already bounced), SaaS (too much SBC), media (shrinking profit pool), gaming (cyclical), telco (competition), internet (ads), ecom (recession/margins). All TMT has become uninvestible. Have fun with Staples/Utes/Energy?

24

15

220

The following funds run by investing "legends" have underperformed the S&P since 2010, over a full cycle, w/ many different flavors of value investing:

- Sequoia

- Oakmark

- Longleaf Partners

- Davis Ventures

- Fairholme

- Fenimore

- Berkshire BV/S

- Markel BV/S

The game is hard

17

22

206

Buffett, Malone, Diller all long in the tooth. Who are some great dealmakers still under 60?

- Andy Florence, CoStar

- Neil Hunn, Roper

- Jensen Huang, Nvidia

Dark Horses

- Josh Silverman, Etsy

- Larry Culp, GE

- Jeff Lawson, Twilio

Zuck’s likely done doing deals

Who else?

48

12

205

Day 1 Bezos vibes from Andy Jassy today on CNBC.

This is exactly how you want your CEO to look - zero vanity and all business. Balding (didn’t get the power shave or Elon plugs), blue collar shirt & modest loose-fitting suit, healthy but not jacked.

12

9

201

The near-term bear case for software is below, expressed in a CIO anecdote shared by UBS analyst Karl Keirstead on software bloat and vendor pricing aggression. The bull case is that extrapolating the current digestion period is too punitive. $MSFT $CRM $NOW

"Our focus right now

4

18

198

Terry Smith causally labeled $FTNT as a duopoly w/ $PANW in firewalls. Each has ~20% share in firewall, and far less in SASE and Cloud which are their respective growth markets... duopoly rly? C'mon

Sold $AMZN bc of 1 comment on grocery and took credit for them not doing it yet?

25

11

193

I’m late to this but the

@BillAckman

recount of his comeback story on

@lexfridman

podcast is truly remarkable. Lost $4B on Valeant, public short campaign turned disaster in $HLF, faced redemptions, facing litigation, Paul Singer was going activist on his public activist business,

8

11

185

$AMZN is changing the way they purchase servers, and this will have a material impact on FCF for the next few years. But its nothing to worry about.

3

18

179

A bad short: Trades 30x consensus estimates, but it’s actually 25x bc they both manage expectations and execute exceptionally … re-rates to 35x as everyone recognizes they’ll continue to beat AND consensus moves up so you lose 2x (fundamentals and multiple)

A decent funding

4

16

180

$2TN market cap, and the WORST looking slide deck in corporate America. Still Day 1 at $AMZN

22

14

169

Uber has gotten so bad in tier II/III cities. Prices and wait times have skyrocketed generally to make it no longer a “no brainer,” and I’ve now been stranded at both Tampa, San Diego airports and downtown Richmond. Did COVID break ridesharing or just transitory?

25

9

165

It cost $25k to have a baby with no complications + 2 nights in the hospital

Among the charges is $4.3k for room and board... I slept on a couch and ate cafeteria food - I can assure it was no St Regis 😂

No refund for the processing error which delayed meds to my wife 5hrs 😬

42

4

169

Investing legend Jeff Vinik in recent interview:

- Spending more time on stocks (less on Lightning/RE), read 8hr/day

- Key to investing is to be bullish long term but avoid bubbles

- Expects light recession then 5-10yrs of prosperity

- Expects rent to stabilize from new supply

2

13

170

$PLTR: “We have a good chance at becoming the most important software company in the world,” CEO Alex Karp told BBG during an interview Monday. “Demand is unprecedented for Palantir’s AI,” he said.

They reported … 13% growth? Do they know what the word “unprecedented” means?

17

2

156

Distribution of U.S. sports rights in order of annual value (by distributor and by league) from MS

6

28

148

$FB will generate ~$158 this year per US sub, nearly identical to $NFLX, but with over twice the gross margin, and 4x the users.

FB has grown US ARPU ~30% for 8 years, while growth has stalled recently.

I think $FB is cheap relative to its long term opportunity set. But (ctd)

8

21

141

41% move in $GOOG since November but you were too smart and had better ideas

14

9

141

Who was your favorite guest star on Friends? Mine was Howard Marks

8

7

139

Not that anyone cares but $MKL just crushed earnings… grew TBV/share >25% in ‘21. Insurance biz growing 17% while underwriting at 90% CR. 80% of mkt cap covered by equities, excess cash, & ventures (if worth 15x FCF). Implies insurance trading ~3x. Embedded rate hedge to boot.

12

9

135

$ADSK isn’t cheap.

Nor should a quasi-monopoly growing 18%, with 92% Gross margins, enormous embedded income statement investment, and which likely grow substantially >GDP w/ high contribution margins until my 1yr old has a college diploma, be.

9

11

135

AWS outage demonstrates the potential resiliency of an intelligently architected cloud network. $NFLX operates in the impacted AWS US East 1 region, but is up and running. NFLX can move from one AWS region to another in a few min - often w/o impacting video streams due to its CDN

2

20

135

Broken clocks are right twice a day and Jeremy Granthams perma bear calls are right once a cycle. A timeline and cautionary lesson for investors:

2010: Grantham sells stocks out of the financial crisis, saying stocks are now overvalued:

6

14

135

$SNOW's Slootman: customers foray into AI has been experimental, it's expensive, there's no clear business model yet to pay for it

"We cant unleash AI & have no business model to pay for it. People will get tired of that really quick. GPUs aren't cheap, as powerful as they are."

6

23

134

This is why it gets the premium multiple. This is effectively a recurring revenue business w/ a price insensitive core customer. Long live $CMG

6

2

119

Feels like you’re stealing businesses @ current prices in Telco/media ( $WBD $CHTR $DIS ), home/construction ( $FERG $FND $LOW $HD ), semiconductors ( $ON $LRCX $KLAC $TSM ). Software companies I never thought I’d own I can now get to hurdle IRRs w/ reasonable assumptions.

16

4

116

Surprised but not shocked to see Warren Buffett at MS TMT this year, on the front row to hear Colette Kress explain how early we are in the shift to accelerated computing. It’s now clear that $NVDA is in fact his secret 4Q stock addition.

8

5

118

Giverny capital flies under the radar, but this is one of the most impressive modern records I've seen. Very difficult to find managers who can last 28 years, let alone put up these absolute and relative numbers. Winning in multiple market environments. Hats off.

10

14

114

"Lemonade will acquire Metromile in an all-stock transaction that implies a fully diluted equity value of approximately $500 million, or just over $200 million net of cash"

Buffett had Geico.

I pick

@Metromile

.

The company announced today that it is going public via a SPAC ($INAQ) and I led the PIPE.

This is an incredible company disrupting car insurance and giving customers a best in class experience.

My one pager is attached. 🙏🏽

326

300

4K

10

8

113

$CHTR share price decline of -68% since '21 peak almost exactly mirrors the decline in its '24 FCF estimates.

9

8

113

What are the best financial history books? Just for open exploration of major financial events, not opinion pieces abt the direction of inflation or gold or rates.

@jfc_3_

?

40

16

106

End of quarters - that magical time of year folks on FinTwit will compare their performance excluding cash drag to the index excluding dividends

8

5

104

FinTwit will idolize Thoma Bravo while passing on buying good SaaS cos down -50-70% themselves, despite the advantage of no takeout premium, bc of trailing GAAP profits (& pivoting into oil bulls as WTI hits cycle highs). Always investing based on what is vs what is likely to be.

9

2

104

Monish Pabrai looks like someone pretending to be Monish Pabrai

2

2

103

What is your best investment idea that has little or nothing to do with AI, GLP-1, or your macro view on rates/inflation?

59

4

102

Not surprised $TGT beat on the topline based on the credit card data.

That is, my wife’s credit card data…

3

0

99

Hard not to be excited abt U.S. housing setup for next several years, and many companies levered to these themes trade at double digit near-term earnings/FCF yields and are aggressively buying back shares

Awesome setup to buy $ORLY $AZO in '18 setup by GFC auto sales cohort and "cash for clunkers". Ideal auto aftermarket customer group declined LSD for 5yrs before inflecting.

Anything like this today in a different industry where trend is set to reverse or data blurs real trend?

9

1

67

9

6

103

Einhorn: "We're not in a bubble. We don't have any basket shorts on at the moment."

5

5

101

A little known & poorly followed company called Amazon Dot Com just reported operating income that was 40% higher than consensus estimates. Sometimes pays to look in the forsaken corners of the market where inefficiencies still exist. $AMZN

4

3

102

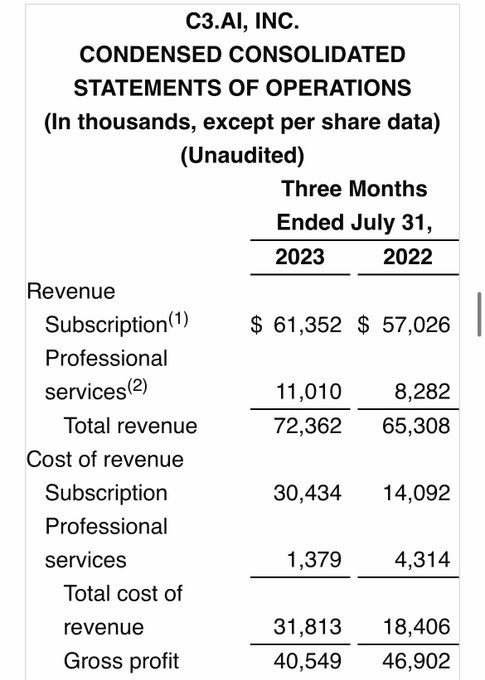

$AI grew subscription revenue $4M yoy, or 7%, during an AI bubble.

More impressively it only took an incremental $16M COGS to deliver that revenue, for an incremental gross margin of -300%. Real impressive.

Definitely an AI winner and definitely a software company.

11

2

98

BREAKING: "Roaring Kitty" is set to be a billionaire as GameStop stock, $GME, surges to $67.50/share in after hours trading.

If $GME opens at or above current levels tomorrow, his shares will be worth ~$325 million and options worth ~$700 million for a combined ~$1 billion.

675

3K

23K

3

6

99

“Father Orlando, who art in Miami, hallowed by thy capital. Thy monthly buyouts come, thy will be done, in the rest of TMT as it is in SaaS. Amen”

2

12

96

Not everyday you see Jim Cramer murder a CEO on public television

14

9

96

They are right, “Liberty Media has blood on their hands!” But it’s not the blood of puppies, it’s active value investors.

$CHTR $LBRDA $QRTEA $LXSMA $SIRI $TRIP

14

11

93

The biggest obstacle I've had to overcome in life is starting my professional career as a telecom and media analyst.

14

2

94

"Q: Are you building ahead of capacity this year? A: The risk of under investing is greater than the risk of over investing."

3

4

93

ROIC matters. $INTC announcement is much better r/r for semicap than Intel. Why? $INTC takes the risk, Semicap has certainty of high-ROIC, aa'l installed base to drive services, gets paid on front end. INTCs ultimate result will be delayed and could be low ROI or even big losses.

3

8

89

Recall that this transaction was contested by shareholders at the time. Kudos to management who defended the sale by saying 1) this is the second most expensive PE SaaS (edtech?) buyout ever and 2) we suck and are failing. $PS

7

7

91

What are the most hated stocks in the market right now not in any sort of financial distress, growing, profitable, and trading at reasonable valuations? $PYPL $ZI $EXPE $DIS $ETSY $DG what else?

28

4

89

Concise summary of the $DISCK / $WBD bull case by BofA:

3

12

89

When you were bearish all year into a face ripping market and your team is the worst in the league

Looks like Panthers owner David Tepper threw a drink into the crowd…

1K

2K

22K

5

1

89

Excited for these Super Bowl commercials to stock up on new short ideas

Last years crop of 43 public companies who advertised underperformed the S&P by -15.5% through today. (not counting private mkt flops like FTX). An evenly distributed portfolio returned -23% vs -7% for SPY

3

9

87

Application software trading well below pre-pandemic mults (from Gugg's Ostrie). Rest of the pack, not as much.

5

2

87

$ADSK price increases since '19 continue at 5%/year like clockwork:

4

5

85

Bunch of high quality biz with reasonable stated multiples, poor technicals & consensus too high, but also under-earning so actual multiples are OK. They also seem to be the names everyone is too scared to own while foolishly trying to time the bottom. These are called longs.

5

1

84

$MU $KMX forced to turn off capital returns right when returning capital is most enticing.

12

1

83

The S&P 600 index is:

- -22% below 2021 highs

- -2% YTD

- Never entered a new bull mkt w/ S&P500/NASDAQ this year

- 5.4% 10yr CAGR

- Flat for 5yrs back to Sept’18

5

12

84

🚩Narrative violation alert 🚩

Cleveland on weak SSS trends, cannibalization, and potential slowing of store growth for $FND

6

5

82

If you’re uncomfortable owning a bureau through cycle at ANY price I’ll gladly provide liquidity

$TRU isn’t $VRSK / $FICO qual. but God isn’t making more bureaus & they’ve competed rationally for 60yrs. India asset = 💎. 14x depressed EPS (prob <10x ‘25/‘26) is simply too cheap

8

0

79

Wifey doing her best to help $AMZN beat on this 3Q guide. Record Prime Day for SV fam by factor of 2-3x.

8

0

77

What is the cheapest stock you know of on 2024 or 2025 PE/FCF that you think with >80% probability will grow organic Earnings/FCF above nominal GDP for the next decade?

A few $ZI $MKL $LOW $APG $GOOG $CHTR $BRK $PYPL $TSM $SPLK $ARMK $FERG $AMZN

16

6

77

“$ADSK is so critical to the sectors it serves that most burgeoning engineers, architects or contractors are trained on its programs in college. In a field where coordination between different professions is required, the work mandates a de facto industry standard: that's $ADSK.”

2

12

73

HBO Max starting out the year on a strong note:

$DISCK $T $DIS $NFLX $VIAC

3

9

71

Love coming to Omaha, always unexpected and fortuitous conversations had and relationships made that make it worth it. Usually come away with 2-3 good stock ideas to mine. And of course special to be in presence of the undisputed 🐐for as long as he’s able to stay at it.

7

1

75

When a company on your watchlist is inching towards your buy price, then suddenly gets acquired

3

2

73

"Sure its a bad industry w/ LSD growth & increasing competition, but they're better operators, emerging from an investment cycle, will buy gobs of stock for yrs. Yes its levered but incumbents are acting rational & they wont need a major network upgrade for a while."

$CHTR

$TMUS

7

3

72

Oh no, Sheri is screwing over $PARA shareholders and riding into the sunset? She's getting the M&A premium and common shareholders are actually getting more dilution to by SkyDance? Apollo "$26B offer" wasn't rly ironclad? Shocked. I'm just shocked.

8

2

71

Hey friend

@Ross__Hendricks

, just reminding you (as requested) that your negative post on $AMZN marked THE bottom $AMZN in May. It is +36% since. The stock crushed estimates and is +7% AH. TTYL

5

1

71

I personally disagree with this and I think it may be why Buffett missed out on so much of tech. Spreading the data is useful for getting to unit economics, operating leverage, seeing how something in reinvestment mode can be very cheap. Good example would be AMZN for a long time

One of the most underrated WEB quotes:

'If you need to use a computer or calculator to figure it out, you shouldn't buy"

1

9

60

9

2

72

Tom Russo still talking abt Nestle which has compounded at 6% over the last 9 years, trades at a 33% premium to SPY multiple, and has negative volumes but he’s convinced is invincible vs. PL

4

3

71

$CHTR now <200mm FDSO… they bought back 25mm shares last year at prices much higher than the current $560

If they keep attacking the stock at this pace, we will be looking at $100 FCF/share in 4-5 years from sharecount reduction alone

& FCF will grow a lot

2

5

68

$FERG well run, wide perceived moat, crowded hedge fund hotel, trades 16x fwd PE

Organic revenue is declining slightly for the 2nd year as they burn off pandemic resi excess. Leader in fragmented industry where alternatives are abundant and pricing power is extremely limited.

5

3

69

Seeing a company publicly mock a shareholder for believing LT performance targets, which were in numerous investor materials and filings for years, and which mgmt repeatedly used to divert attention from mediocre operating results, is a first for me in this business. $RBA

4

1

66

Awesome setup to buy $ORLY $AZO in '18 setup by GFC auto sales cohort and "cash for clunkers". Ideal auto aftermarket customer group declined LSD for 5yrs before inflecting.

Anything like this today in a different industry where trend is set to reverse or data blurs real trend?

9

1

67

$INTU with 43% trailing Adj. EBITDA margins just let go of 10% of its workforce

4

3

65