Patrick Zweifel

@PkZweifel

Followers

13K

Following

4K

Statuses

4K

Chief economist at Pictet Asset Management. Tweeting about #GlobalMacro #EmergingMarkets #China #US. All views my own. RT=interesting

Geneva, Switzerland

Joined July 2017

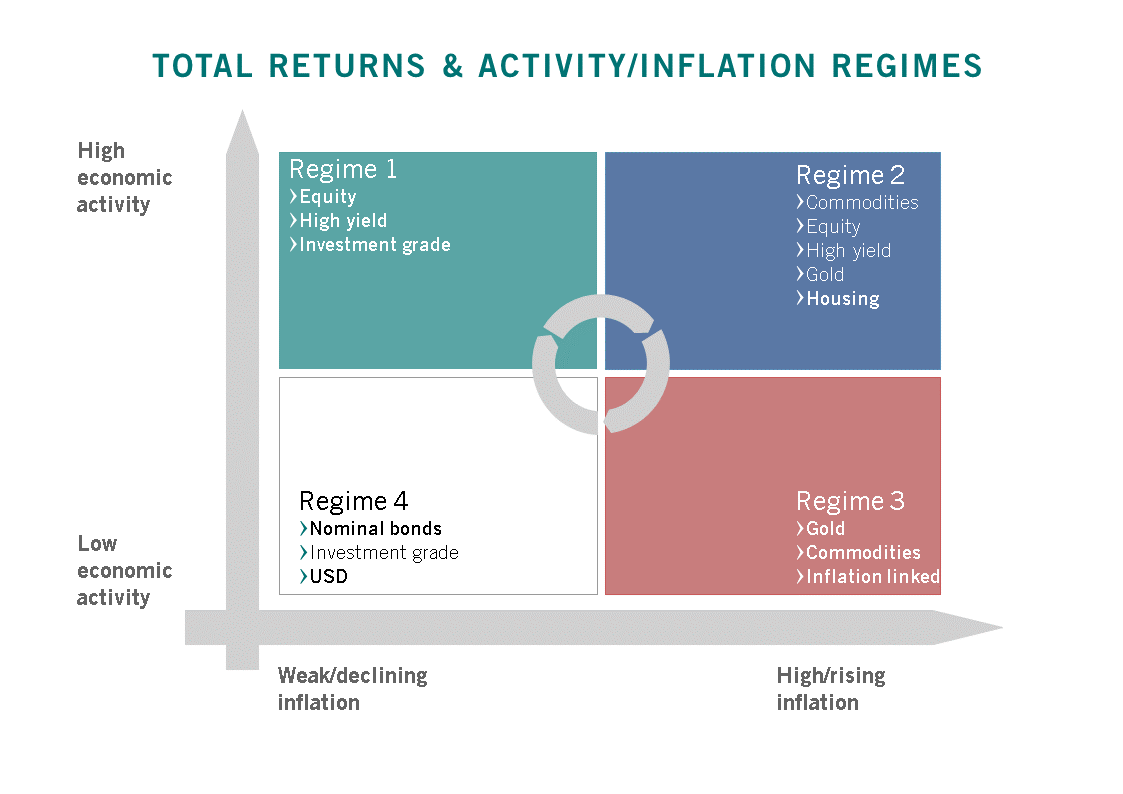

1/2 How asset classes behave when mixing inflation/activity regimes? √ Housing, commo & gold best stable hedges against inflation √ Low inflation & strong growth is best for riskier assets √ Yet, the 2nd best environment for stocks & high yield credit

9

73

216

RT @PkZweifel: 1/ Global PMIs jumped to 50 in January, the first time since September 2022 that this critical level has been reached. Both…

0

22

0

6/ Price components in DM have risen slightly to their highest level since the end of 2022, suggesting more inflationary pressure in the short term, but remain well below their long-term average consistent with inflation normalizing towards its target.

0

1

9

RT @PkZweifel: 1/ Chinese activity data for December continued to improve, beating expectations, as did GDP growth, which accelerated to 8%…

0

41

0

Yes, this is certainly part of the explanation for the recent rise in the savings rate: households have in fact been repaying part of their mortgages since 2022 Q3 (RMB1.3tn or >3% of their total debt) 👇 That said, the savings rate has been rising linearly since the early 1990s 👇, and many other factors explain both the high rate and its rise, among the most important in my view: . Precautionary savings: weak social safety nets and rising healthcare costs . Parents save heavily for their children’s education . Expensive property markets and high down payments . Aging population: the one-child policy and insufficient pensions . Limited consumer credit: historically low access to credit forces cash-based purchases . Confucian traditions and values

2

0

3

@kevinziyizhao Absolutely, Q3 growth has gone from 2% q/q ann to 3.2%, which indeed leads to a higher y/y variation for Q4 and for 2024. That said, regardless of this revision, Q4 growth is very strong compared to Q3 at 8% annualized

1

0

2

11/ The three-month rebound in total lending (TFL), thanks in particular to non-bank lending, pushed the credit impulse further away from its neutral level and to the highest since October 2202, implying GDP growth above its potential estimated at just under 5%.

0

1

18