ConvexityMaven

@ConvexityMaven

Followers

30,340

Following

2

Media

74

Statuses

177

Creator of $MOVE Index, $PFIX & $MTBA Managing Partner at ; Publisher of a (free) Commentary

Laguna Beach & NYC

Joined October 2019

Don't wanna be here?

Send us removal request.

Explore trending content on Musk Viewer

Jack Smith

• 424526 Tweets

FEMA

• 400955 Tweets

Tigers

• 122259 Tweets

#2BTheQUEEN𖤍

• 117166 Tweets

SURPRISE FROM BECKY

• 115363 Tweets

Massa

• 113244 Tweets

Maui

• 86242 Tweets

Astros

• 80661 Tweets

Kalafina

• 67053 Tweets

Royals

• 59823 Tweets

#AEWDynamite

• 48615 Tweets

Orioles

• 43089 Tweets

Inter Miami

• 34408 Tweets

Yankees

• 30479 Tweets

#AgathaAllAlong

• 28363 Tweets

Brewers

• 28222 Tweets

GOLD RUSH

• 26547 Tweets

岡田監督

• 20133 Tweets

学園アイドルマスター

• 19829 Tweets

SMILEY OF CHARLOTTE03

• 18619 Tweets

今季限り

• 16479 Tweets

Mendoza

• 16233 Tweets

ميسي

• 15320 Tweets

Saint Dr MSG Insan

• 14450 Tweets

#今年も新作スイーツラテ飲みたーーーーい

• 13758 Tweets

藤川球児

• 11757 Tweets

梶浦さん

• 10772 Tweets

AL Central

• 10631 Tweets

Dalmau

• 10323 Tweets

The warning bell is ringing...

The Yield Curve is the BEST predictor of a recession. What is so strange is this near inversion before the FED has started hiking.

This is why investors should be nervous, what does the bond market know ?

In theory, a recession in mid-2024

36

98

524

The $MOVE is back above 140, time to send the bond market to its room for a time out.

The MOVE @ 140 implies a yield change of ~9bp a day for the next month, that is not sustainable; similar to the VIX near 50, or ~3.1% a day for a month.

@profplum99

is tossing in the towel.

19

82

426

Let's vote on "Recession"....

Bond market - "yes"

Stock market - "yes"

Credit market - "maybe"

VIX - "NOPE"

The equity options market is way too cheap. The VIX and VIX futures strip is flat at ~30.5, yet Actual (realized) Volatility is 35%.

The VIX should be near 40

40

37

417

Grab a fork, bonds are done....

Unless you want to consider Fed hikes (which I do not) we have reached equilibrium with T2s nearing 5.0%.

I suppose T10s could push back to 4.75%, but without the Fed hiking, it could be hard to touch 5% again.

This means it is time to sell

29

45

356

Launching on Nov 6th, a listed investment "strategy" that owns only newly issued MBS

As chatted with:

@EconguyRosie

@ErikTownsend

@GrantsPub

@profplum99

@biancoresearch

Yields ~100bps over similar duration Corporate (IG) bonds with NO CREDIT RISK

24

41

240

Are you kidding me...?!?

My reaction to

@JeffSnider_AIP

suggesting that TIPs offer useful insight into inflation, notwithstanding the FED has taken their ownership from 10% to 26% this past year.

@profplum99

a little help please ?

Full podcast here >>

27

24

236

The gas tank is empty on long maturity bonds....

A UChicago geek might consider GDP to be the "income" of the US while the T10yr is the "cost of capital". As such, a business will borrow when the cost of capital is less than the income it can produce.

This implies a

12

34

228

New Commentary...

Today I consider why newly-issued MBS continue to trade nearly 145bp over USTs, a distress level only exceeded in the past 20 years during the 2008/09 GFC and 2020 Covid panic; a spread nearly double the historical average near 75bp.

I

11

32

225

What we have here is a failure of imagination...

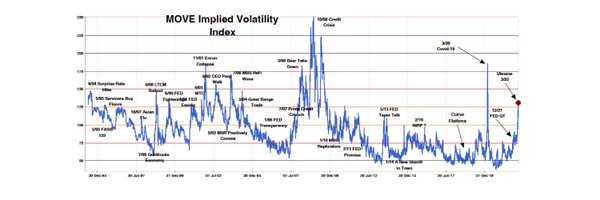

The MOVE Index (the VIX for bonds) in kissing 120, a level only exceeded for 11 days in March 2020, and during the GFC.

The MOVE at 120 implies that rates will move 7.5bp a day, everyday, for the next month.

7

51

220

BANG....UST 2s vs 30s flips positive for the first time since July 2022....MBS bonds are about to jump

As noted in the Odd Lots podcast >>>

and detailed on pages 8/9 >>

@tracyalloway

@TheStalwart

@profplum99

@biancoresearch

10

41

217

Many people are uncomfortable with the concept of Convexity since its principles are grounded in math and physics, but today I hope to offer a more practical explanation suitable for the entire family.

Click here >>

9

46

205

New Commentary

The most important topic for Professional Investors is "The Cost of Carry" - what it costs to hold a position over time.

Today I detail this concept in layman's terms for civilians.

@profplum99

@real_bill_gross

@TruthGundlach

8

31

206

I usually advise against trading the MOVE vs the VIX, but this eye-candy deserves a comment

The MOVE Index is a blend of Implied Vols across the Yield Curve, and recently the IVol for options on 2yrs has almost tripled as the FED has hinted at rate hikes

The anomaly is the VIX

7

27

189

My good friend Michael Green (

@profplum99

) and I chat about Macro-economics, Interest rates, Convexity, and their intersection on Real Vision.

Separately, my wife thinks I should shave my head and knock off ten years...thoughts ?

hb

14

30

177

Traders are pushing all their chips to the Curve Steepener

Presently: 2yr = 4.26% and 10yr = 3.82%

A spread of -44bp

The Xmas 2024 breakeven is +28bp;

So 2s at 3.54% vs unchanged 10s, or closer to nine Fed cuts

Comments:

@biancoresearch

@dampedspring

@profplum99

@hkuppy

11

29

177

Yesterday's Tsy2yr auction at 4.29% may have been the bottom for the front-end. May 2023 FFund futures closed at 4.65%, on top of the DOTS.

We will be in a full on recession by Q2-23, one year after the first T2yr vs T10yr inversion

@profplum99

was early, but he is now right

12

19

161

Simple Housing math...

Buy $500k house, 10% down ($50k) , borrow $450k @ 3.25% >>> Monthly payment = $1958

With mortgage rates at 5.50%, a $1958 monthly payment can only borrow $345k, so with same $50k down can only buy house at $395k.

Flat income >>> housing down 21%

hb

10

15

161

Shameless promotion on

@ErikTownsend

podcast

A basket of five-year Investment Grade bonds yields about 4.90%

A similar Duration recent issue Mortgage-backed Security (MBS) with no credit risk yields over 6.0%

Thanks FED

>

>

19

17

163

Stick a fork in long-term rates ?

Fed Inflation target = 2.00%

Fed rate is +50bp = 2.50% (DOTs)

Funds to 2yr (chart 1) is +50bp = 3.00%

2yr to 10yr (chart 2) is +100bp = 4.00%

Without QE, 10yr rate is fully priced at 3.89%

Comments:

@dampedspring

@biancoresearch

@profplum99

21

22

143

Do I have stand in Times Square in a thong to grab your attention ?

Newly-issued MBS: Still the best bonds on the planet

My newly-issued MBS strategy is crushing all reasonable alternatives by over 100bps YTD. And such MBS are still near a "crisis spread" of +140bp to

26

16

151

Credit Suisse: It's always negative Convexity

Back of the envelope - CS was effectively short 34mm of the VIAC $80 strike put on 3/20.

This is equivalent to asking for 20% margin with stock at $100

Option jumped from $5 to $38, or $1.122bn loss

Repeat for other positions

3

17

146

MOVE Index at 131...what this means...

This Index is an annual number describing a "normal distribution".

Divide by the square root of 252 (trading days), or 15.9 to estimate the "daily breakeven"...8.2bp.

Divide by SqRoot 12 (months), or 3.46 for the monthly range ~+/- 38bps

4

31

139

My new "MBS Strategy" launches Nov 6th and starts listed trading on Nov 7th

Details:

1)

2)

@ErikSTownsend

@MacroVoices

3)

@EconguyRosie

2023 issued MBS are at crisis spreads

cc:

@profplum99

@GrantsPub

15

12

138

Bond market missed the memo:

The ImpVol for UST 2yrs is 117nv: In plain English that indicates a 16% chance it will close above 5.85% and a 16% chance it will close below 4.05% on Election Day.

This is just plain silly, the FED is "one and done" (as detailed in my latest

9

19

138

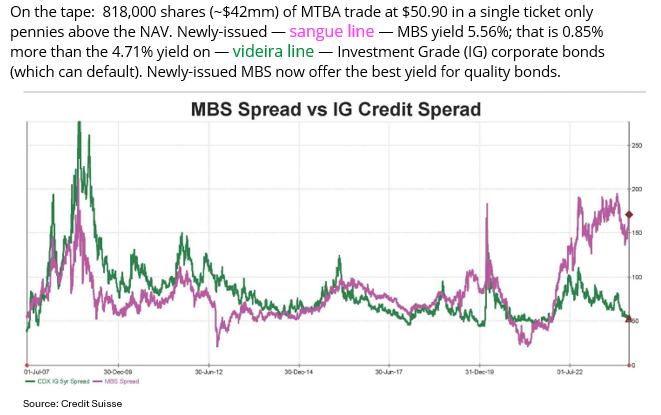

$MTBA now has AUM of $461mm, with no seed money. Crushes the MBS Index ETFs in both coupon and YTM.

Newly issued MBS are the best value in market; also a terrific way to play the Yield Curve steepener.

The Simplify MBS ETF $MTBA – liquid as water…. Jump in. Learn more about $MTBA:

2

5

21

9

11

128

Time for the infamous 2 1/2 day rule....??

I abhor market timing, but it is my experience that when $H1T happens, the market peaks and reverses 2.5 days after ignition.

Day one is shock

Day two is panic, prayer and a call from Risk

Mid-Day 3, the position is closed out

5

8

124

Time for the infamous 2 1/2 day rule....

While I generally abhor market timing, it is my experience that when $H1T happens, the market peaks and reverses 2.5 days after ignition

Day one is shock

Day two is panic, prayer and a call from Risk

Mid-day 3, the position is closed out

6

5

120

Did I suffer a TKO at the hands of

@JeffSnider_AIP

and

@profplum99

?

You be the judge:

Despite a two vs one cage match, I'm still punching.

Watch for when they predict this "non-FED induced inflation" will end...(Spoiler alert: They don't !!)

12

16

116

FED rings the bell: Sell Interest rate vol and buy MBS

The MOVE Index tripled when the FED started hiking as the peak was unknown; and stay elevated because we did not know when they would start cutting.

Now we know...

The MOVE (implied volatility) is @ 101; but bonds have

10

18

122

New Commentary....

All eyes are on the FED, will it be 25bp or 50bp...I don't care !!

The more important question is the path and speed of rate policy over the next twelve months.

What is clearly the “wrong price” is the 249bp of rate cuts anticipated

10

10

119

New Commentary...

While never totally transparent, the medium-term path forward for interest rates is well lit.

Via a combination of Politics, the Data, the Calendar, and Hubris (human ego) the FED is boxed in, and the most likely scenario is “one and done” until the election.

8

14

117

The 2022 Model Portfolio

Come this time every year, I publish a list of “Investments” that I think will do well over the intermediate horizon - two to five years.

Remember: Sizing is more important the entry level.

Be safe

hb

10

17

110

I am somewhat new to Twitter, so I will admit that mean words from Trolls hurt my feelings...

But to all of you who accused me of being disrespectful for pushing back on Lacy and

@jeffSnider_AIP

for their sanguine view of rates and inflation...

Nanny nanny boo boo to you !!

21

6

113

The greatest risk to a financial asset portfolio is a flip in the Correlation between Stocks and Bonds; and it may already be happening.

SPX and Rates peaked/ troughed Dec '21 and Jun '22; and now in tandem - so much for 60/40.

Armageddon with rates above 3.5% to 5.0% (chart)

5

24

113

Thank you, Bloomberg....

Stay tuned for my much teased MBS encore due November 6th/7th

Commentary preview on Nov 1st; here and my website...

5

4

109

For Option-geeks only...

Wall Street derivative desks are in a tizzy

The one-year forward 2s vs 30s was +4bp on March 1; it is now NEGATIVE 96bp

They are short billions of Curve options struck at zero; From my archive is similar to EUR in 2008

6

19

111

Stocks worried - Nope

Bonds in panic - Yup

The VIX is clipping at 27.5 vs and "actual" volatility of 25.5%; an 8% premium.

The MOVE will close near 137 vs it component "actual" volatility of 94; a 46% premium !!

MOVE @ 137 is roughly 8bp rate change per day for September.

7

17

108

Important comment to

@boazweinstein

buying MBS

He is NOT buying MBS Index products, rather he is long NEW ISSUE MBS which civilians can only buy via my new MBS ETF "strategy"

Corp IG = 5.11%

New issue MBS (FN 6%)= 6.05%

Consult

@profplum99

or

@EMcArdleInvest

for ticker

16

12

110

New Commentary...

We all know the FED is going to ease at some point; and they have told us via the DOTs that their terminal rate will be near 2.50%. As such, the next big money trade will be discerning when and how the FED will start to cut their

6

15

111

"MBS Strategy" update:

72% of all 30yr MBS have coupons from 2% to 3.5%; so the value is in the newly issued MBS, not the Index:

"MBS strategy" distribution of 5.93% is:

+228bp vs MBS Index

+132bp vs UST 10yr

+84 IG Corps (5yr)

cc:

@profplum99

@boazweinstein

@EMcArdleInvest

7

9

109

My new "MBS Strategy" starts trading today.

This Strategy offers civilians direct access to new issue MBS bonds (~FN 6% MBS) with higher coupons and lower durations than MBS Index products (~FN 3% MBS).

Yields +100bp to IG Corp with NO credit risk

>>>

8

7

105

2024 Stocking Stuffers

Come this time every year, I publish a list of “Investments” that I think will do well over the intermediate horizon.

This year I offer "buy and hold" investments to add to a core Equity portfolio

@profplum99

@EMcArdleInvest

4

14

106

The only chart that matters...

Inflation above 2.5% has coincided with the correlation between stocks and rates (bonds) flipping negative; so they would trade up and down together.

A levered (risk parity) portfolio would be toast.

Not calling a "top", just saying watch it...

4

18

99

Not as exciting as Tiktok "cats playing with yarn", but this is the most important chart for investing in Financial Assets.

The correlation between stocks/bonds seems to break down with Inflation over 2.5%, and 10yr rates above 4.25% (see past Commentaries).

60/40 will be toast

7

27

99

A definitive reply: $MOVE vs $VIX is fine

One-month Implied Volatility for liquid assets usually prices near 21 day Actual Volatility

Act Vol for Rates over the past month is 165 (vs $MOVE = 156) and for Stocks is 29.9 (vs $VIX = 27.9)

QED

cc:

@profplum99

@DiMartinoBooth

5

21

99

What's the "wrong price"....

This is the Yield Spread between the 30yr rate and the 40yr rate, presently NEGATIVE 23bp.

In English, the 30yr rate is 3.37% and the 40yr rate is 3.14% (anticipating a 30yr in 2033 of 2.79%)

2s vs 10s at negative 60ish is fine, this is nuts.

9

13

95

MBS vs T10yr peaked on Oct 17 at +190bp, they are now +150bp...why ?

T2yr was 5.21%; now 4.67%

MOVE was 130; now 110

New MBS duration is 24% 2yr rates

Index MBS duration is 4% 2yr rates

Still a lot more to go

@boazweinstein

@dampedspring

@profplum99

@biancoresearch

@Hedgeye

5

13

98

(almost) 'Convexity for Dummies'

Short Convexity can always be found lurking near the scene of the crime.

Today's Commentary - "Lurking at the Scene", offers a practical discussion of Convexity, and uses the GameStop mania as a working model.

7

19

96

Attention Volatility/Options/Convexity experts; I know something you don't...

The Yield Curve inversion has had a greater impact on MBS (and thus retail mortgage rates) than the increase in Implied Volatility...check it out.

6

13

94

You have all seen this chart of the "alligator mouth" of SPX vs Rates; and I am NOT going to make any predictions about the near future.

But I am a UChicago monetarist, and I will just say that at some point rates matter.

The "D" in DCF means "discount rate"

@profplum99

??

11

8

92

Time for a reminder: When financial markets implode, short Convexity can be found lurking near the scene of the crime

SVB bought $80bn of MBS with fickle bank deposits

So they were effectively short $80bn unhedged puts

QED

5

8

89

@DiMartinoBooth

is correct, a rising $MOVE with declining rates is correlated to increasing Credit risk

But if you want to see blood in the streets, check out the Euro MOVE Index at 157; a 3.5 Standard Deviation outlier

The FED: Everyone has a plan until punched in the face.

3

21

88

Boom.....Powell said it: "It's unlikely the next move will be higher"

Buy my NYSE Listed newly-issued MBS strategy

(ticker available)

Yield ~ 6.01%; Dur ~ 4.4

@profplum99

@EconguyRosie

@biancoresearch

@dampedspring

@ErikSTownsend

@LynAldenContact

6

6

86

New Commentary:

Mortgage Bonds (MBS) are priced at crisis levels; but we are not in a crisis, just an ordinary FED tightening.

They are the cheapest bond asset class; period

In only a few pages I take "A Deep Dive into MBS" and the valuation process.

7

17

87

New Commentary:

For bond investors there are three 'risk knobs' that can be turned to add extra return:

1) Duration

2) Credit

3) Convexity

With the $MOVE Index near 125, selling Convexity via near-Par MBS offers the best avenue to add "alpha".

5

8

86

The Yield Curve, as measured as the spread between the 2yr rate and the 10yr rate, has exploded to 128bps. This is the largest gap since mid-2015; yet Implied Volatility has yet to follow.

One of these risk vectors must adjust.

(Hint: It will be Volatility)

4

19

82

Blood in the (Wall) Street ?

NOT INVESTMENT ADVICE: But I sold the VIAC May 21 (53 day) expiry put, Strike = 45, at $5.50

Implied Vol of 90% (vs VIX of 21ish)

Breakeven of $39.50 (near the Dec 2019 close)

Unless there is another shoe to drop, this option will decay quickly

6

2

80

My ETF nearing its October 2022 high as rates rise and the Yield Curve steepens

Rate exposure is ~$0.27 per basis point, rates higher ETF higher

Pays a $1.20/yr dividend

You don't buy because you are bearish on rates, you buy it buy because you are bullish and may be wrong

7

5

81

New Commentary:

The FED has purchased a berth on the Titanic after it hit the iceberg. Mr. Powell is conducting the band while the market is sending up rescue flares and we all wonder who will find a lifeboat

email to: harley

@bassman

.net to subscribe

6

16

78

Weekend reading - Convexity for "investment civilians"...

Options 101:

Options 102:

While together they are not quite "Convexity for Dummies", they are in that same zip code.

GameStop mania used as a working model

2

16

79

Replay Available:

The Lacy Hunt's guest appearance on our Keeping It Simple webinar is here:

I challenge Dr. Hunt and

@profplum99

to explain why inflation will recede and the economy will soon turn South

Who do you believe, me or your lying eyes ?

6

10

74

The MOVE Index (the VIX for bonds) close at 69.31, a local high since the March rate peak.

But it is being depressed by the FED's near zero short-term rate policy.

If the MOVE was calculate using only +10yr rates, it would be over 81.5.

2

11

75

The difference between a "Correction" and a "Panic": Liquidity !

As long as daily borrowing can be rolled over, we are fine; when loans are called in...Yikes

2008 and 2020 were both institutional "margin calls"; the risk now is "civilian" (barstool) margin calls force selling

3

10

74

Team Transitory takes a victory lap as Inflation minus everything is zero....

@profplum99

@EconguyRosie

please note sarcasm....

2

4

75

New Commentary - "The Water is Warm in the MBS Pool"; a primer on MBS bonds for civilians.

MBS are 75bp wider to USTs since the FED hinted at QT last year, they are presently 2-standard deviations cheap to the average.

I like MBS here, a lot !!

5

10

76

Homework for bond allocators (not advice), but if you are curious how to use my new "MBS Strategy":

1) Replacement with similar Curve exposure

2) Replacement with big Curve steepener

3) Hedge Fund style zero duration steepener

cc:

@profplum99

@VrntPerception

@EMcArdleInvest

2

3

77

New Commentary

The market has bet the ranch that the U.S. economy is going to ‘hard land’ soon; thus the FED will cut rates as soon as September; this is simply NOT going to happen

The Yield Curve is way too inverted

@profplum99

and I agree, finally

12

8

75

Infamous two and one-half day rule...?

A trading "old wive's tale" I created years ago was the 2 1/2 day rule. Here, a shock to the market would take 60 hours to resolve.

Day 1: Ignore

Day 2: Panic and prayer

Day 3: Stop out at mid-day

The curve flattener will flame out soon.

5

13

76

Using ETFs to play the Yield Curve with the Pro's...

Below is the Spot 7yr rate vs the Forward 20yr rate, notice the inversion (red)

Buy 6 units of a 3x levered 10yr futures strategy and;

Buy 1 unit of a Payer Swaption Hedge strategy

Locally flat duration + long convexity

hb

9

4

73

Bonds Have Had a Wild Ride. The Roller Coaster Is Coming to a Stop. via

@BarronsOnline

Click below for my NYSE-listed newly-issued MBS Strategy

4

10

73

Be careful of Mortgage REITs that are trading near Tangible Book Value (TBV).

The dividend is solid, but the market price is not as FED purchases of Agency MBS have driven relative value to a forever low.

I'm not saying "sell", but prices will drop ~10% if the FED reduces QE

2

14

74

$MOVE Index back below 100, before the FED !

Mostly confirms the rate peak has been set, but the elephant in the room is the length of the "pause" before the "pivot" to actually cutting rates.

Realized MOVE for past month is 109: Options market likes a longer pause

5

8

71

Weekend reading....

Click below for a good introduction to my macro-economic worldview...

Immodestly, one of my better Commentaries that also highlighted the November 2018 Yield Curve inversion as a precursor for a recession in early 2020.

Be safe

2

8

68

Beware of TIPs...

The FED has overweighted their purchase of TIPs relative to Coupon bonds since QE5. 5yr TIPs now sport a near forever low yield of -1.65%.

Forget their yield sensitivity, I can't even guess whether TIPs have a positive or negative duration !

h/t IJ

3

11

67

Time for the infamous 2 1/2 day rule....

I abhor market timing, but it is my experience that when $H1T happens, the market peaks and reverses 2.5 days after ignition.

Day one is shock

Day two is panic, prayer and a call from Risk

Mid-Day 3, the position is closed out

2

5

66

Indeed the FED increased its holdings of both coupon bonds and TIPs since March 2020, but on a relative basis they increased their TIPs ownership by over twice as much.

There is minimal "free market" information offered in a controlled asset.

2

5

63

Not investment advice; but....

Both

@profplum99

and I love Simplify's Short-term Futures Strategy; the yield of the UST two-year with the duration (price sensitivity) of the UST ten-year.

Ping

@SimplifyAsstMgt

for more

Remember: Sizing is more important than entry level

4

2

65

New Commentary:

A primer on Leverage (which is different than Convexity)

Plus, ideas for civilians to profit like the professionals.

Ping my partner

@profplum99

for ideas, or call my associates for further details

6

9

64

MBS is effectively an interest rate "buy-write" with an embedded Curve Steepener

T10yr @ 4.46%

IG Corp @ 5.11%

FN 3% @ 5.17%

MBS Index @ 5.25%

FN 6% @ 6.05%

New Issue "MBS Strategy" ~5.90%

$MOVE @ 124 (vs Avg = ~95)

$VIX @ 14.5 (vs Avg = ~20)

6

4

62

Let's mark this addition to my Holiday Stocking Stuffers...(call me in June 2023)..

Buy 6 units of a 3x levered 10yr futures strategy and;

Buy 1 unit of a Payer Swaption Hedge strategy

Prices ~~ $15.75 and $65.00

Have a safe and happy Holiday Season

2

8

61

The infamous two and one-half day rule arrives on schedule.

Tsy30yr peaked Sunday night at 1.93%, about 60 trading hours after the post-FED gap from 2.19%.

Presently trading at 2.11%, retracing almost 70% of the move.

Sometimes the "old wives" ain't that old...

2

4

60

Stop the "recession" chatter...Nominal GDP rose by 6.3%, the economy is still expanding.

What you should worry about is the historian relationship between Nominal GDP and 10yr Rates. If the FED cannot chill Nominal GDP, rates are going north.

3

4

60

New Commentary:

The near record Yield Curve inversion combined with an elevated level of Implied Volatility finally offers some rather dreamy investment opportunities.

An investment dream for Team Transitory (

@profplum99

)

5

10

60

Mortgage Rates normalize: B

eware

MBS bonds tend to trade ~75bp higher in rate than other bonds. The FED compressed this to barely 25bp during Covid, but now it's reverting

1) Levered REITs will take a hit

2) Housing will slow

3) Market anticipates balance sheet run off

3

16

56

What's the wrong price ?

MBS (Mortgage-backed Securities)

The long-term average spread is usually about 75bp, presently it is near 35bp.

mREITs are trading at a discount to NAV in anticipation of a reversion to the mean.

ReFinance your home mortgage soon !

3

6

58

All's clear, mortgage REITs looking good

I will pen a longer Commentary on my site soon, but until then, MBS spreads are at 118bps, a level only exceeded during the GFC (chart)

The largest generic mREITs tangible book declined by only 16.7% to $13.12, despite a 70bp widening

7

10

54

As noted below, there is a long-term relationship between Nominal GDP and the 10yr Treasury rate.

This is not spurious, there is fundamental support for this correlation; thus it is possible to have rising rates in a "technical" recession in Real GDP.

10

3

54

Call the referee, someone is off sides

SPX is now in a "bull market", yet Bonds anticipate a 141bp cut in the one-year rate by June 2024

Core CPI @ 5.3%; Core PCE @ 4.7%, and U-Rate at 3.7%.....I just don't see it

I love FN 5s @ 98.65 to yield ~5.22%

1

5

53

There is a fundamental reason for the Yield Curve to correlate with Implied Volatility:

The MOVE Index (the VIX for interest rates) closed at 61.73 yesterday, it should be closer to 75ish.

Flashing red light for High Yield (junk bonds) and MBS.

2

10

51

"Short Convexity can always be always be found lurking near the scene of the crime"

I offered this on March 16, 2021

For a primer on Convexity from my Maven's classroom:

and....

Near zero rates encourages risky behavior

1

9

50

Thank you

@ErikSTownsend

and

@PatrickCeresna

for hosting me on MacroVoices

or

Hubris (ego) will motivate Powell to hike rates aggressively to avoid the WSJ obituary: "Powell - an Arthur F. Burns redux"

4

6

53

New Commentary:

The FED’s too specific Forward Guidance via the DOTs offered investors unsupported confidence in the economic future. As such, too many investors and financial managers exhibited classic Moral Hazard by taking on imprudent levels of risk

2

4

53

(Should be) Head line news....

The European 2yr interest rate leaps above zero for the first time since October 2015.

I suppose this could be a blip, but if not, watch out below. Money flowing out of the Euro to USD to escape negative rates will slow down.

7

9

50

I penned "A Deep Dive into Mortgage Bonds" last November 3, 2022

Pure mREITs have rallied over 25%; If short-term rates decline, mREITs have more to go...will they ?

Find out today on KIS with

@profplum99

and

@EPBResearch

4

8

50

Reply to

@LoganMohtashami

: It was not shrinking inventories that jumped house prices, rather it was the intersection of income/interest rate relative to price.

Rates dropping from 5% to 2.75% accounts for 85% of price spike

Per

@GrantsPub

below, a current 5.5% rate is a dagger

5

12

51

Re: Credit Suisse...

It's never different this time; short convexity is always "Lurking as the Scene"

See prior tweet for my guess of the math underpinning the loss.

Click above link for deeper dive into the mechanics of Convexity

0

10

51

While many users of this Strategy will be those who are certain interest rates will rise; the better users are those who think rates will decline, but want to protect against the chance they are wrong as a rise above 4.25% may bring on a financial tsunami

2

7

52

Supporting comments on my new "MBS Strategy" from

@VrntPerception

Questions..."Simply" ask

@EMcArdleInvest

(you know I can't post a ticker) or

@profplum99

4

3

49

So you missed the bottom, stop your blubbering

FN 3s - [proxy of MBS Index] price = 84.59

Distribution = 3.55%, YTM = 4.99%

New MBS strategy price = 50.96

Dist and YTM = ~5.85%,

vs Credit IG = 4.85% (+100bp)

vs 10yr = 4.29% (+155bp)

MBS is still the wrong price

@profplum99

3

6

50